You might also like

- Short Notes On Public FinanceDocument3 pagesShort Notes On Public FinanceJakir_bnkNo ratings yet

- Is Fiscal Policy the Answer?: A Developing Country PerspectiveFrom EverandIs Fiscal Policy the Answer?: A Developing Country PerspectiveNo ratings yet

- INTRODUCTION TO PUBLIC FINANCE THEORYDocument36 pagesINTRODUCTION TO PUBLIC FINANCE THEORYelizabeth nyasakaNo ratings yet

- Public Sector AccountingDocument33 pagesPublic Sector AccountingYEe Ding100% (15)

- CTT - Public Finance (Prelim Exam)Document4 pagesCTT - Public Finance (Prelim Exam)geofrey gepitulanNo ratings yet

- Fiscal Policy Tools and ImpactsDocument49 pagesFiscal Policy Tools and ImpactsAnum ImranNo ratings yet

- Economic Modelling: Deficit Financing, National Debt and Ricardian EquivalenceDocument15 pagesEconomic Modelling: Deficit Financing, National Debt and Ricardian EquivalencecbagriNo ratings yet

- Advanced Public Sector AccountingDocument408 pagesAdvanced Public Sector AccountingFatin Ferdinand100% (1)

- Public FinanceDocument48 pagesPublic FinanceJorge Labante100% (1)

- MMPA633 - Transformative Governance - Jerson F. PuaDocument8 pagesMMPA633 - Transformative Governance - Jerson F. PuaJohn Michael TalanNo ratings yet

- Chapter III: Managerial Approach To Government BudgetingDocument58 pagesChapter III: Managerial Approach To Government BudgetingkNo ratings yet

- What Is Fiscal Administration?: Nonprofit Budgeting Fiscal ResponsibilityDocument11 pagesWhat Is Fiscal Administration?: Nonprofit Budgeting Fiscal ResponsibilityApril MaeNo ratings yet

- Fiscal FunctionsDocument3 pagesFiscal FunctionsAshashwatmeNo ratings yet

- Principles of Public Finance-PresentationDocument17 pagesPrinciples of Public Finance-Presentationnikkie100% (1)

- The Budget ProcessDocument31 pagesThe Budget ProcessrizzaNo ratings yet

- 1390-Annual Fiscal ReportDocument48 pages1390-Annual Fiscal ReportMacro Fiscal PerformanceNo ratings yet

- What Is A Projectvs ProgramDocument2 pagesWhat Is A Projectvs ProgramRCC NPCC100% (1)

- Public Fiscal AdministrationDocument119 pagesPublic Fiscal AdministrationWilson King B. SALARDANo ratings yet

- Guide to Public Debt TheoriesDocument2 pagesGuide to Public Debt TheoriesRonnie TambalNo ratings yet

- Public Sector AccountingDocument17 pagesPublic Sector AccountingAnthony ChaiNo ratings yet

- Public Financial System and Public Enterprises ExperiencesDocument5 pagesPublic Financial System and Public Enterprises ExperiencesMeane BalbontinNo ratings yet

- Public DebtDocument4 pagesPublic DebtMohit MandaniNo ratings yet

- Public Finance and Taxation - 1 Nbaa Cpa-1Document265 pagesPublic Finance and Taxation - 1 Nbaa Cpa-1Osmund100% (1)

- Public Finance Course Outline 2Document2 pagesPublic Finance Course Outline 2Wonde Biru0% (1)

- Responsibility of Fiscal Policy UPDATEDDocument24 pagesResponsibility of Fiscal Policy UPDATEDFiona RamiNo ratings yet

- Management Accounting EssayDocument5 pagesManagement Accounting EssayvardaNo ratings yet

- Public Finance and Economic Management Reforms in MalawiDocument15 pagesPublic Finance and Economic Management Reforms in MalawiInternational Consortium on Governmental Financial ManagementNo ratings yet

- Public Financial ManagementDocument41 pagesPublic Financial ManagementDenalynn100% (1)

- Bovens Public Accountability - Connex2Document35 pagesBovens Public Accountability - Connex2NazLubna100% (1)

- CHAPTER ONE Public Finanace (2) - 1Document10 pagesCHAPTER ONE Public Finanace (2) - 1mani per100% (1)

- Public DebtDocument9 pagesPublic DebtSamiksha SinghNo ratings yet

- The Intergovernmental Fiscal Transfers On Local Government Autonomy and Service Delivery in TanzaniaDocument26 pagesThe Intergovernmental Fiscal Transfers On Local Government Autonomy and Service Delivery in TanzaniaGlobal Research and Development ServicesNo ratings yet

- Chapter One Mening and Scope of Public FinanceDocument12 pagesChapter One Mening and Scope of Public FinanceHabibuna Mohammed100% (1)

- CH1 Fundamental Principles of Public FinanceDocument29 pagesCH1 Fundamental Principles of Public Financefadwa100% (1)

- Performance Based Budgeting: Some ViewsDocument4 pagesPerformance Based Budgeting: Some ViewsadityatnnlsNo ratings yet

- Government Budget Objectives and ImpactDocument21 pagesGovernment Budget Objectives and ImpactSireen IqbalNo ratings yet

- 09 - The New Budget System For The Phil. GovernmentDocument11 pages09 - The New Budget System For The Phil. GovernmentJuharto UsopNo ratings yet

- Zambia IFMIS Presentation To World Bank Meeting3Document24 pagesZambia IFMIS Presentation To World Bank Meeting3Ahmednoor Hassan67% (3)

- Nature of Development Economics: Is Concerned Primarily With The Efficient, Least-CostDocument2 pagesNature of Development Economics: Is Concerned Primarily With The Efficient, Least-CostRio AlbaricoNo ratings yet

- Public Debt PDFDocument18 pagesPublic Debt PDFRyan DueÑas GuevarraNo ratings yet

- Sources of RevenuesDocument6 pagesSources of RevenuesTabangz ArNo ratings yet

- Introduction To Fiscal AdministrationDocument10 pagesIntroduction To Fiscal Administrationcharydel.oretaNo ratings yet

- Governmental and Not Profit AccountingDocument4 pagesGovernmental and Not Profit AccountingPahladsingh100% (1)

- Public Fin CH-1Document49 pagesPublic Fin CH-1Wonde Biru100% (1)

- Understanding the Meaning and Scope of Public FinanceDocument47 pagesUnderstanding the Meaning and Scope of Public FinanceMaria Elena Sitoy BarroNo ratings yet

- Public Finance Week 2Document30 pagesPublic Finance Week 2Letsah BrightNo ratings yet

- Public ExpenditureDocument7 pagesPublic ExpenditureHarsh ShahNo ratings yet

- Public Sector AccountingDocument5 pagesPublic Sector AccountingKhushboo JainNo ratings yet

- Taxation Law ExplainedDocument33 pagesTaxation Law ExplainedDavid100% (2)

- Public Debt and Fiscal Consolidation: A Closer Look at Public DebtsDocument7 pagesPublic Debt and Fiscal Consolidation: A Closer Look at Public DebtsVinn EcoNo ratings yet

- Effect of Public Expenditure On Economic Growth in Nigeria, 1970 2009Document16 pagesEffect of Public Expenditure On Economic Growth in Nigeria, 1970 2009Andy OkwuNo ratings yet

- Government Budgeting PPBS To Performance-Based BudgetingDocument3 pagesGovernment Budgeting PPBS To Performance-Based BudgetingChong BianzNo ratings yet

- Public FinanceDocument2 pagesPublic Financemohamed sheikh yuusufNo ratings yet

- Public Sector Compliance with Audit Act 1957Document6 pagesPublic Sector Compliance with Audit Act 1957Afiq NaimNo ratings yet

- Urban and Regional Planning Report (Local Government Code)Document19 pagesUrban and Regional Planning Report (Local Government Code)Sherlock HoImes100% (1)

- Budget and Budgetary SystemDocument6 pagesBudget and Budgetary SystemunicornNo ratings yet

- Approaches and Techniques in BudgetingDocument13 pagesApproaches and Techniques in BudgetingMary Grace Ocampo PaciaNo ratings yet

- Final Exam: Part I (30 Points) - Multiple Choice QuestionsDocument11 pagesFinal Exam: Part I (30 Points) - Multiple Choice QuestionsStefaniaGiansiracusaNo ratings yet

- Public ExpenditureDocument6 pagesPublic ExpenditureNaruChoudhary0% (1)

- Imbong v. Ochoa 4. The Question of Constitutionality Must Be Raised at The Earliest OpportunityDocument3 pagesImbong v. Ochoa 4. The Question of Constitutionality Must Be Raised at The Earliest OpportunitychristineNo ratings yet

- WR CSP 21 NameList Engl 021121Document325 pagesWR CSP 21 NameList Engl 021121Mohd BilalNo ratings yet

- TAXATION With ActivityDocument14 pagesTAXATION With ActivityAriel Rashid Castardo BalioNo ratings yet

- Income Tax On Individuals Part 2Document22 pagesIncome Tax On Individuals Part 2mmhNo ratings yet

- Petitioners Respondent Atty. Noe Q. Laguindam Atty. Elpidio I. DigaumDocument11 pagesPetitioners Respondent Atty. Noe Q. Laguindam Atty. Elpidio I. DigaumRomy IanNo ratings yet

- Murder Conviction UpheldDocument9 pagesMurder Conviction UpheldBobNo ratings yet

- Atilano II vs. AsaaliDocument7 pagesAtilano II vs. AsaaliRamil GarciaNo ratings yet

- Javellana V Lutero and RCA JaroDocument4 pagesJavellana V Lutero and RCA JaroYet Barreda BasbasNo ratings yet

- Fact Sheet Huntsville Property Tax RenewalDocument2 pagesFact Sheet Huntsville Property Tax RenewalChamber of Commerce of Huntsville/Madison CountyNo ratings yet

- Legal Ethics Midterm NotesDocument31 pagesLegal Ethics Midterm NotesChristia Sandee Suan100% (2)

- Comelec Nanawagan Sa Payapang Halalan 2022: Comelec Gives In: Voter Registration To Be Extended Until October 31Document1 pageComelec Nanawagan Sa Payapang Halalan 2022: Comelec Gives In: Voter Registration To Be Extended Until October 31John Paul ObleaNo ratings yet

- Code of Conduct For Court PersonnelDocument6 pagesCode of Conduct For Court PersonnelJenelyn Bacay LegaspiNo ratings yet

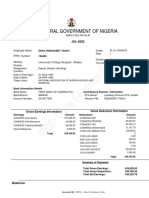

- Federal Pay Slip for Margaret Taiwo GiwaDocument1 pageFederal Pay Slip for Margaret Taiwo GiwaHalleluyah HalleluyahNo ratings yet

- AutoText Technologies, Inc. v. Apple, Inc. Et Al - Document No. 3Document2 pagesAutoText Technologies, Inc. v. Apple, Inc. Et Al - Document No. 3Justia.comNo ratings yet

- Screenshot 2021-12-10 at 5.33.04 PMDocument1 pageScreenshot 2021-12-10 at 5.33.04 PMtriloke pandeyNo ratings yet

- AutoPay Output Documents PDFDocument2 pagesAutoPay Output Documents PDFAnonymous QZuBG2IzsNo ratings yet

- Fact Sheet - The United States Information AgencyDocument9 pagesFact Sheet - The United States Information AgencyThe American Security ProjectNo ratings yet

- Oracle Database 11g: Administration Workshop IDocument2 pagesOracle Database 11g: Administration Workshop IFilipe Santos100% (1)

- Geriatric Nursing: Saint Louis UniversityDocument5 pagesGeriatric Nursing: Saint Louis UniversityDannielle Kathrine JoyceNo ratings yet

- Introduction To Philippine Criminal Justice SystemDocument68 pagesIntroduction To Philippine Criminal Justice SystemLouvieBuhayNo ratings yet

- NoticeOfLiability To USA Agents Mrs. Alvarado PDFDocument16 pagesNoticeOfLiability To USA Agents Mrs. Alvarado PDFMARSHA MAINESNo ratings yet

- To Whomsoever It May ConcernDocument1 pageTo Whomsoever It May ConcernPiyush MishraNo ratings yet

- An Essay On The Foreign Policy of IndiaDocument2 pagesAn Essay On The Foreign Policy of IndiatintucrajuNo ratings yet

- Case Study On Cinderella Flora Farms PVT LTDDocument1 pageCase Study On Cinderella Flora Farms PVT LTDTosniwal and AssociatesNo ratings yet

- Vakalatnama Supreme CourtDocument2 pagesVakalatnama Supreme CourtSiddharth Chitturi80% (5)

- Rules of Origin Are Used To Determine TheDocument4 pagesRules of Origin Are Used To Determine TheLeema AlasaadNo ratings yet

- Francisco Vs TRBDocument3 pagesFrancisco Vs TRBFranz KafkaNo ratings yet

- Commart To San Miguel Case DigestDocument4 pagesCommart To San Miguel Case DigestYolanda Janice Sayan FalingaoNo ratings yet

- Digest - RPA v. ReyesDocument2 pagesDigest - RPA v. ReyesJoseph Bernard Areño MarzanNo ratings yet

- Plaintiff,: in The United States District Court For The District of MarylandDocument3 pagesPlaintiff,: in The United States District Court For The District of MarylanddhoNo ratings yet

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassFrom EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNo ratings yet

- Sacred Success: A Course in Financial MiraclesFrom EverandSacred Success: A Course in Financial MiraclesRating: 5 out of 5 stars5/5 (15)

- Personal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationFrom EverandPersonal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationRating: 4.5 out of 5 stars4.5/5 (18)

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsFrom EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsNo ratings yet

- Bookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesFrom EverandBookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesRating: 4.5 out of 5 stars4.5/5 (30)

- You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantFrom EverandYou Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantRating: 4 out of 5 stars4/5 (104)

- Improve Money Management by Learning the Steps to a Minimalist Budget: Learn How To Save Money, Control Your Personal Finances, Avoid Consumerism, Invest Wisely And Spend On What Matters To YouFrom EverandImprove Money Management by Learning the Steps to a Minimalist Budget: Learn How To Save Money, Control Your Personal Finances, Avoid Consumerism, Invest Wisely And Spend On What Matters To YouRating: 5 out of 5 stars5/5 (5)

- How To Budget And Manage Your Money In 7 Simple StepsFrom EverandHow To Budget And Manage Your Money In 7 Simple StepsRating: 5 out of 5 stars5/5 (4)

- Basic Python in Finance: How to Implement Financial Trading Strategies and Analysis using PythonFrom EverandBasic Python in Finance: How to Implement Financial Trading Strategies and Analysis using PythonRating: 5 out of 5 stars5/5 (9)

- Rich Nurse Poor Nurses The Critical Stuff Nursing School Forgot To Teach YouFrom EverandRich Nurse Poor Nurses The Critical Stuff Nursing School Forgot To Teach YouNo ratings yet

- Swot analysis in 4 steps: How to use the SWOT matrix to make a difference in career and businessFrom EverandSwot analysis in 4 steps: How to use the SWOT matrix to make a difference in career and businessRating: 4.5 out of 5 stars4.5/5 (4)

- Budget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.From EverandBudget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Rating: 5 out of 5 stars5/5 (75)

- Money Made Easy: How to Budget, Pay Off Debt, and Save MoneyFrom EverandMoney Made Easy: How to Budget, Pay Off Debt, and Save MoneyRating: 5 out of 5 stars5/5 (1)

- How to Save Money: 100 Ways to Live a Frugal LifeFrom EverandHow to Save Money: 100 Ways to Live a Frugal LifeRating: 5 out of 5 stars5/5 (1)

- Lean but Agile: Rethink Workforce Planning and Gain a True Competitive EdgeFrom EverandLean but Agile: Rethink Workforce Planning and Gain a True Competitive EdgeNo ratings yet

- Retirement Reality Check: How to Spend Your Money and Still Leave an Amazing LegacyFrom EverandRetirement Reality Check: How to Spend Your Money and Still Leave an Amazing LegacyNo ratings yet

- The New York Times Pocket MBA Series: Forecasting Budgets: 25 Keys to Successful PlanningFrom EverandThe New York Times Pocket MBA Series: Forecasting Budgets: 25 Keys to Successful PlanningRating: 4.5 out of 5 stars4.5/5 (8)

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsFrom EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo ratings yet

- Money Management: The Ultimate Guide to Budgeting, Frugal Living, Getting out of Debt, Credit Repair, and Managing Your Personal Finances in a Stress-Free WayFrom EverandMoney Management: The Ultimate Guide to Budgeting, Frugal Living, Getting out of Debt, Credit Repair, and Managing Your Personal Finances in a Stress-Free WayRating: 3.5 out of 5 stars3.5/5 (2)

- Budgeting: The Ultimate Guide for Getting Your Finances TogetherFrom EverandBudgeting: The Ultimate Guide for Getting Your Finances TogetherRating: 5 out of 5 stars5/5 (14)

- Mastering Your Money: A Practical Guide to Budgeting and Saving For Christians Take Control of Your Finances and Achieve Your Financial Goals with 10 Simple Steps: Christian BooksFrom EverandMastering Your Money: A Practical Guide to Budgeting and Saving For Christians Take Control of Your Finances and Achieve Your Financial Goals with 10 Simple Steps: Christian BooksNo ratings yet