You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Vertical Analysis of Financial Statements - Pepsi V CokeDocument2 pagesVertical Analysis of Financial Statements - Pepsi V CokeCarneades33% (3)

- America's Healthy Future Act of 2009Document223 pagesAmerica's Healthy Future Act of 2009KFFHealthNewsNo ratings yet

- Components of RNOA - Profit Margin and Asset TurnoverDocument3 pagesComponents of RNOA - Profit Margin and Asset TurnoverCarneadesNo ratings yet

- Monthly CMBS Delinquency August 2009Document1 pageMonthly CMBS Delinquency August 2009CarneadesNo ratings yet

- Earnings Quality Analysis - Operating Cash Flow To Net IncomeDocument3 pagesEarnings Quality Analysis - Operating Cash Flow To Net IncomeCarneadesNo ratings yet

- Introduction To Credit Risk Analysis: Debt To Equity RatioDocument3 pagesIntroduction To Credit Risk Analysis: Debt To Equity RatioCarneadesNo ratings yet

- Basic V Diluted EPSDocument1 pageBasic V Diluted EPSCarneadesNo ratings yet

- Bond Pricing 101Document3 pagesBond Pricing 101CarneadesNo ratings yet

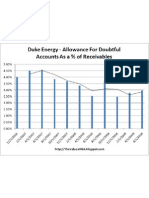

- Duke Energy Allowances To ReceivablesDocument1 pageDuke Energy Allowances To ReceivablesCarneadesNo ratings yet

- OCF To CapexDocument1 pageOCF To CapexCarneadesNo ratings yet

- RealPoint CMBS Delinquency Report July 2009Document15 pagesRealPoint CMBS Delinquency Report July 2009Carneades100% (1)

- Net Operating Profit Margin (NOPM)Document1 pageNet Operating Profit Margin (NOPM)CarneadesNo ratings yet

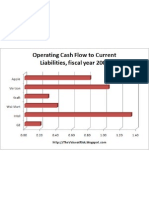

- OCF To Current LiabilitiesDocument1 pageOCF To Current LiabilitiesCarneadesNo ratings yet

- Aetna Q2 09 Financial ResultsDocument14 pagesAetna Q2 09 Financial ResultsCarneadesNo ratings yet

- Housing Starts August 2009Document1 pageHousing Starts August 2009CarneadesNo ratings yet

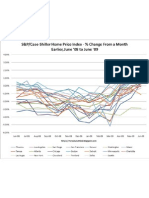

- SP/Case Shiller Index Through June 2009Document1 pageSP/Case Shiller Index Through June 2009CarneadesNo ratings yet

- Semiconductor Data Through July 2009Document2 pagesSemiconductor Data Through July 2009CarneadesNo ratings yet

- Social Security COLA History 1999-2009Document1 pageSocial Security COLA History 1999-2009CarneadesNo ratings yet

- ENSYS Cap and Trade Briefing 8-20-09Document25 pagesENSYS Cap and Trade Briefing 8-20-09CarneadesNo ratings yet

- Democrats and Out of State Campaign ContributionsDocument3 pagesDemocrats and Out of State Campaign ContributionsCarneadesNo ratings yet

- The SEC's Role Regarding and Oversight of Nationally Recognized Statistical Rating OrganizationsDocument124 pagesThe SEC's Role Regarding and Oversight of Nationally Recognized Statistical Rating OrganizationsCarneadesNo ratings yet

- Prison Population As % of US Population 1980-2007Document1 pagePrison Population As % of US Population 1980-2007CarneadesNo ratings yet

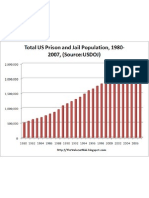

- US Prison Population 1980-2007Document1 pageUS Prison Population 1980-2007CarneadesNo ratings yet

- Medicare Modernization ActDocument416 pagesMedicare Modernization ActCarneadesNo ratings yet

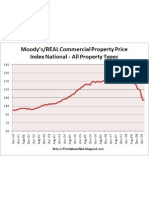

- Moodys CPPI August 2009Document1 pageMoodys CPPI August 2009CarneadesNo ratings yet

- July 2009 Housing Starts 2005-PresentDocument1 pageJuly 2009 Housing Starts 2005-PresentCarneadesNo ratings yet

- TIC Data June 2009Document1 pageTIC Data June 2009CarneadesNo ratings yet

- July 2009 Housing Starts 1959-PresentDocument1 pageJuly 2009 Housing Starts 1959-PresentCarneadesNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Cost of Goods Sold Problems PDF 1 3Document3 pagesCost of Goods Sold Problems PDF 1 3Janine padronesNo ratings yet

- Astro TalkDocument24 pagesAstro TalkAteet RaiNo ratings yet

- Konrath 14Document11 pagesKonrath 14MaskurNo ratings yet

- Chart of AccountsDocument4 pagesChart of AccountsmakahiyaNo ratings yet

- Sensitivity AnalysisDocument8 pagesSensitivity AnalysisFarhan Ahmed SiddiquiNo ratings yet

- Student Allowance ParentsDocument12 pagesStudent Allowance ParentsHinewai PeriNo ratings yet

- Finals ReviewerDocument9 pagesFinals ReviewerAira Jaimee GonzalesNo ratings yet

- Job Order CostingDocument39 pagesJob Order CostingCharisse Ahnne Toslolado100% (1)

- Motivating Employees through Performance-Based Incentive SchemesDocument23 pagesMotivating Employees through Performance-Based Incentive SchemesNazia Anjum100% (1)

- TOWS Matrix: A Strategic Planning and Management ToolDocument3 pagesTOWS Matrix: A Strategic Planning and Management ToolkamalezwanNo ratings yet

- House Bill 19-1258Document6 pagesHouse Bill 19-1258Michael_Lee_RobertsNo ratings yet

- Group Assignment - Questions - RevisedDocument6 pagesGroup Assignment - Questions - Revised31231023949No ratings yet

- Power and Process of Distrain-Final Version April 2017Document73 pagesPower and Process of Distrain-Final Version April 2017Samuel Oyenitun100% (1)

- TAX05 - First Preboard ExaminationDocument13 pagesTAX05 - First Preboard ExaminationMIMI LANo ratings yet

- Contract of Architect-ClientDocument14 pagesContract of Architect-ClientShe Timbancaya100% (1)

- Trading Steps - IntradayDocument4 pagesTrading Steps - IntradayManish Khanolkar25% (4)

- A Project Report On Direct TaxDocument52 pagesA Project Report On Direct Taxrani26oct72% (18)

- Pre-Qualification Exam in LawDocument4 pagesPre-Qualification Exam in LawSam MieNo ratings yet

- Siklus Akuntansi Pada PT Adi JayaDocument11 pagesSiklus Akuntansi Pada PT Adi Jayafitrianura04No ratings yet

- ProQuestDocuments 2013 03 08Document147 pagesProQuestDocuments 2013 03 08Oktaria MayasariNo ratings yet

- Managing Earnings Using Classification Shifting: Evidence From Quarterly Special ItemsDocument39 pagesManaging Earnings Using Classification Shifting: Evidence From Quarterly Special ItemsNovaz BestNo ratings yet

- Presentation and Preparation of FS FINALDocument86 pagesPresentation and Preparation of FS FINALJoen SinamagNo ratings yet

- Insights on selecting stocks to find winners and avoid losersDocument35 pagesInsights on selecting stocks to find winners and avoid losersramakrishnaprasad908100% (1)

- Illustrative Financial Statements O 201210Document316 pagesIllustrative Financial Statements O 201210Yogeeshwaran Ponnuchamy100% (1)

- Balance SheetDocument1 pageBalance Sheetolyad tesfayeNo ratings yet

- Assignment-2 (New) PDFDocument12 pagesAssignment-2 (New) PDFminnie908No ratings yet

- Dividend Policy at FPL Group, Inc. (A)Document16 pagesDividend Policy at FPL Group, Inc. (A)Aslan Alp0% (1)

- Final Exammm 3Document10 pagesFinal Exammm 3Marianne Adalid MadrigalNo ratings yet

- Startup India Learning Program Business TrackerDocument13 pagesStartup India Learning Program Business TrackerAvi G. UjawaneNo ratings yet

- Cambridge International AS & A Level: Accounting 9706/12Document12 pagesCambridge International AS & A Level: Accounting 9706/12Aimen AhmedNo ratings yet