You might also like

- Your Amazing Itty Bitty® Book of QuickBooks® TerminologyFrom EverandYour Amazing Itty Bitty® Book of QuickBooks® TerminologyNo ratings yet

- Taller Seis Acco 111Document44 pagesTaller Seis Acco 111api-274120622No ratings yet

- Accounting for Merchandising OperationsDocument26 pagesAccounting for Merchandising OperationsKayesCjNo ratings yet

- Accounting For InventoriesDocument12 pagesAccounting For InventoriesNoor AlSabbaghNo ratings yet

- Chapter 5 Inventory AccountingDocument57 pagesChapter 5 Inventory Accountinghosie.oqbe100% (1)

- ACCT Midterm 2Document26 pagesACCT Midterm 2Gene'sNo ratings yet

- Accounting For Merchandising OperationsDocument31 pagesAccounting For Merchandising OperationsBülent Kılıç100% (1)

- Review of The Accounting Cycle: Survival Notes - Actbas2 TERM 1 AY 2014-2015Document12 pagesReview of The Accounting Cycle: Survival Notes - Actbas2 TERM 1 AY 2014-2015Gilbert TiongNo ratings yet

- Exercise For Chapter 5 6Document16 pagesExercise For Chapter 5 6Ngọc Ánh VũNo ratings yet

- Chapter 5 PowerpointDocument37 pagesChapter 5 Powerpointapi-248607804No ratings yet

- B ACTG111 4 Practice Problems MerchandisingDocument16 pagesB ACTG111 4 Practice Problems Merchandisinghotdog kaNo ratings yet

- Chapter 4,5,6 QuizzesDocument22 pagesChapter 4,5,6 QuizzesAnonymous aPQWrwo3iiNo ratings yet

- True or False accounting quiz answersDocument5 pagesTrue or False accounting quiz answersMikaella SanchezNo ratings yet

- Valuation of Inventories A Cost-Basis ApproachDocument46 pagesValuation of Inventories A Cost-Basis ApproachIrwan JanuarNo ratings yet

- A201 Ch6 Fall 2013Document44 pagesA201 Ch6 Fall 2013Set LuNo ratings yet

- Harrison Chapter 6 StudentDocument48 pagesHarrison Chapter 6 StudentDakshin SooryaNo ratings yet

- Chapter 6 PowerpointDocument34 pagesChapter 6 Powerpointapi-248607804No ratings yet

- Incomplete RecordsDocument13 pagesIncomplete RecordsSylvan Muzumbwe MakondoNo ratings yet

- 2010-06-23 203304 Financialaccounting 2Document6 pages2010-06-23 203304 Financialaccounting 2pi!No ratings yet

- Chapter 5—Accounting for Merchandising OperationsDocument15 pagesChapter 5—Accounting for Merchandising OperationsSantun Pi TOen100% (2)

- Chapter 3 NotesDocument10 pagesChapter 3 NotesInhoi TchoiNo ratings yet

- Accounting For Merchandising Business PDFDocument38 pagesAccounting For Merchandising Business PDFFariha Lynn Safwan86% (7)

- Accounting for Merchandising BusinessesDocument38 pagesAccounting for Merchandising BusinessesJeffrey JosephNo ratings yet

- Accounting for Merchandising BusinessesDocument72 pagesAccounting for Merchandising Businessesdavesanity23100% (1)

- Accounting for Merchandising Business OverviewDocument57 pagesAccounting for Merchandising Business OverviewAliaJustineIlagan100% (1)

- Intermediate I Chapter 8Document45 pagesIntermediate I Chapter 8Aarti JNo ratings yet

- Welcome Back: Accounting For Business Decisions ADocument65 pagesWelcome Back: Accounting For Business Decisions ALeah StonesNo ratings yet

- ABM 12 - Accounting-Module 2 SCIDocument6 pagesABM 12 - Accounting-Module 2 SCIWella LozadaNo ratings yet

- Chapter - 1 Inventories Definition: - Inventory Is Used To DesignateDocument14 pagesChapter - 1 Inventories Definition: - Inventory Is Used To DesignateMulugeta TsegaNo ratings yet

- intermidet ch4Document90 pagesintermidet ch4kqk07829No ratings yet

- Operating Cycle of A Merchandising BusinessDocument10 pagesOperating Cycle of A Merchandising BusinessJanelle FortesNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument25 pagesAccounting Cycle of A Merchandising BusinessMichelle Vinoray Pascual100% (2)

- Adjusted Trial Balance ProfittDocument4 pagesAdjusted Trial Balance ProfittShesharam ChouhanNo ratings yet

- Acc. QuestionsDocument5 pagesAcc. QuestionsFaryal MughalNo ratings yet

- Accounting ChapterDocument13 pagesAccounting ChapterMamaru SewalemNo ratings yet

- Methods of Estimating InventoryDocument46 pagesMethods of Estimating Inventoryone formanyNo ratings yet

- Chap 004Document45 pagesChap 004Yuti XianNo ratings yet

- Module 12Document35 pagesModule 12Alyssa Nikki VersozaNo ratings yet

- DocxDocument11 pagesDocx?????No ratings yet

- Exam Revision - 5 & 6 SolDocument7 pagesExam Revision - 5 & 6 SolNguyễn Minh ĐứcNo ratings yet

- Chapter 5. Accounting For Merchandising OperationsDocument5 pagesChapter 5. Accounting For Merchandising OperationsÁlvaro Vacas González de EchávarriNo ratings yet

- Accounting For Merchandising OperationsDocument13 pagesAccounting For Merchandising OperationsAB Cloyd100% (1)

- Acctg 11-1 Gbs For Week 11Document5 pagesAcctg 11-1 Gbs For Week 11Ynna Gesite0% (1)

- Slater11e Ch15 StudDocument50 pagesSlater11e Ch15 StudIvana May BedaniaNo ratings yet

- CH 08Document38 pagesCH 08مريمالرئيسي50% (4)

- Handouts Acctg 1 - MerchandisingDocument13 pagesHandouts Acctg 1 - MerchandisingJoannah Marie OliverosNo ratings yet

- ch05 Part 1 2023Document47 pagesch05 Part 1 2023hstptr8wdwNo ratings yet

- Practice Test Chap 56Document8 pagesPractice Test Chap 56Jayr OcoyNo ratings yet

- q2 ProbDocument11 pagesq2 ProbGamers HubNo ratings yet

- MerchandisingDocument14 pagesMerchandisingalok_misNo ratings yet

- The Gross Profit Method For Estimated Ending InventoryDocument4 pagesThe Gross Profit Method For Estimated Ending InventoryKeith Joanne Santiago100% (2)

- Tutorial (Merchandising Without Answers)Document18 pagesTutorial (Merchandising Without Answers)Luize Nathaniele SantosNo ratings yet

- CashflowDocument6 pagesCashflowAizia Sarceda Guzman71% (7)

- Lecture 6 Accounting For Inventory (I)Document33 pagesLecture 6 Accounting For Inventory (I)chestervale1No ratings yet

- Import Business: A Guide on Starting Up Your Own Import BusinessFrom EverandImport Business: A Guide on Starting Up Your Own Import BusinessRating: 4 out of 5 stars4/5 (1)

- Accounting All-in-One For Dummies, with Online PracticeFrom EverandAccounting All-in-One For Dummies, with Online PracticeRating: 3 out of 5 stars3/5 (1)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Taller Cuatro Acco 112Document35 pagesTaller Cuatro Acco 112api-274120622No ratings yet

- Taller Tres Acco 112Document41 pagesTaller Tres Acco 112api-274120622No ratings yet

- 8 2aDocument2 pages8 2aapi-274120622No ratings yet

- CCC 6Document2 pagesCCC 6api-274120622No ratings yet

- Taller Ocho Acco 111Document29 pagesTaller Ocho Acco 111api-274120622No ratings yet

- Caleb BorkeDocument1 pageCaleb Borkeapi-274120622No ratings yet

- CCC 8Document2 pagesCCC 8api-274120622No ratings yet

- Taller Dos Acco 112Document51 pagesTaller Dos Acco 112api-274120622No ratings yet

- Taller Uno Acco 112Document44 pagesTaller Uno Acco 112api-274120622No ratings yet

- 8 4aDocument2 pages8 4aapi-274120622No ratings yet

- 7 1aDocument1 page7 1aapi-274120622No ratings yet

- 7 4aDocument2 pages7 4aapi-274120622No ratings yet

- ccc4 3Document1 pageccc4 3api-274120622No ratings yet

- CCC 5Document10 pagesCCC 5api-274120622No ratings yet

- ccc3 5Document1 pageccc3 5api-274120622No ratings yet

- ccc4 1Document1 pageccc4 1api-274120622No ratings yet

- ccc3 4Document1 pageccc3 4api-274120622No ratings yet

- ccc4 2Document1 pageccc4 2api-274120622No ratings yet

- ccc3 3Document1 pageccc3 3api-274120622No ratings yet

- ccc3 2Document1 pageccc3 2api-274120622No ratings yet

- Self 2Document1 pageSelf 2api-274120622No ratings yet

- ccc3 1Document1 pageccc3 1api-274120622No ratings yet

- ch08 ProblemDocument9 pagesch08 Problemapi-281193111No ratings yet

- ccc2 4Document1 pageccc2 4api-274120622No ratings yet

- Self Test DaisyDocument1 pageSelf Test Daisyapi-274120622No ratings yet

- Taller Cinco Caleb BorkeDocument1 pageTaller Cinco Caleb Borkeapi-274120622No ratings yet

- ccc2 1Document1 pageccc2 1api-274120622No ratings yet

- CH 08Document8 pagesCH 08api-274120622No ratings yet

- ch06 CookieDocument4 pagesch06 Cookieapi-2741206220% (1)

- Oracle ERP 11i - R12 Functional - Technical Materials - MOACDocument12 pagesOracle ERP 11i - R12 Functional - Technical Materials - MOACRNo ratings yet

- ACC 201 Accounting Cycle WorkbookDocument70 pagesACC 201 Accounting Cycle Workbookarnuako25% (20)

- MX - Cost Accounting PDFDocument5 pagesMX - Cost Accounting PDFZamantha TiangcoNo ratings yet

- WHBM08 - Inventory & Cost of Goods SoldDocument64 pagesWHBM08 - Inventory & Cost of Goods SoldMuhammad Salman RasheedNo ratings yet

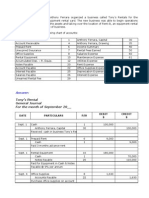

- Tony's Rentals General Journal For September 20Document17 pagesTony's Rentals General Journal For September 20Rehan Mehmood63% (8)

- Akuntansi BiayaDocument8 pagesAkuntansi BiayaDevi NababanNo ratings yet

- CHAPTER 14 Business Combination PFRS 3Document3 pagesCHAPTER 14 Business Combination PFRS 3Richard DuranNo ratings yet

- Overhead Variances and Productivity Measures for Manufacturing CompaniesDocument6 pagesOverhead Variances and Productivity Measures for Manufacturing Companiesmonne100% (2)

- Unicredit Banka OracleDocument34 pagesUnicredit Banka OracleSlobodan BuljugićNo ratings yet

- The Impact of ERP On Supply Chain Management - Exploratory Findings From A European Delphi Study PDFDocument18 pagesThe Impact of ERP On Supply Chain Management - Exploratory Findings From A European Delphi Study PDFshipra177No ratings yet

- Practice MidtermDocument14 pagesPractice MidtermMaria Li100% (1)

- 2Document14 pages2romeoremo13No ratings yet

- Bank Recon Solutions Exercise 2 3Document7 pagesBank Recon Solutions Exercise 2 3Kevin James Sedurifa OledanNo ratings yet

- Week 2 Leap FabmDocument7 pagesWeek 2 Leap FabmDanna Marie EscalaNo ratings yet

- Accounting Cycle Self Test QuestionsDocument6 pagesAccounting Cycle Self Test QuestionsFahad MushtaqNo ratings yet

- Chapter 18 Answer KeyDocument9 pagesChapter 18 Answer KeyNCT100% (1)

- Bondoc Johnpaulo Act2b Accounting Module6Document8 pagesBondoc Johnpaulo Act2b Accounting Module6Joeces Ian DizonNo ratings yet

- Part 2 Basic Accounting Journalizing LectureDocument11 pagesPart 2 Basic Accounting Journalizing LectureKong Aodian100% (2)

- Iscool Merchandise Owner Janine AquinoDocument19 pagesIscool Merchandise Owner Janine AquinoJulian Adam PagalNo ratings yet

- Practice Set - Basic AccountingDocument26 pagesPractice Set - Basic AccountingThessaloe B. Fernandez0% (1)

- Retail Sales ManualDocument5 pagesRetail Sales ManualJose VertizNo ratings yet

- Basic Accounting Multiple ChoiceDocument4 pagesBasic Accounting Multiple Choicenda04030% (1)

- Rekening Koran Permata IDRDocument2 pagesRekening Koran Permata IDRericksanjaya80% (5)

- Perpetual Transactions: Journal EntriesDocument71 pagesPerpetual Transactions: Journal EntriesRona Mae AnteroNo ratings yet

- XXXXXXXXXX4003 20240128150640302188 2 Unlocked 3 Protected 1Document6 pagesXXXXXXXXXX4003 20240128150640302188 2 Unlocked 3 Protected 1r6540073No ratings yet

- Tallyerp 9 For ApmcDocument24 pagesTallyerp 9 For ApmcJawed Ibn KhudbuddinNo ratings yet

- Rosalinda's Boutique Chart of AccountsDocument8 pagesRosalinda's Boutique Chart of AccountsRechelleRuthM.DeiparineNo ratings yet

- Mgt101 PApers With SolutionDocument13 pagesMgt101 PApers With Solutioncs619finalproject.com100% (7)

- Accounting Sample QuestionsDocument6 pagesAccounting Sample QuestionsScholarsjunction.comNo ratings yet

- Quiz On Job Order CostingDocument5 pagesQuiz On Job Order CostingnaomiNo ratings yet