You might also like

- Taller Dos Acco 112Document51 pagesTaller Dos Acco 112api-274120622No ratings yet

- Taller Cuatro Acco 112Document35 pagesTaller Cuatro Acco 112api-274120622No ratings yet

- Taller Tres Acco 112Document41 pagesTaller Tres Acco 112api-274120622No ratings yet

- CCC 8Document2 pagesCCC 8api-274120622No ratings yet

- 8 4aDocument2 pages8 4aapi-274120622No ratings yet

- Taller Uno Acco 112Document44 pagesTaller Uno Acco 112api-274120622No ratings yet

- 8 2aDocument2 pages8 2aapi-274120622No ratings yet

- ccc4 2Document1 pageccc4 2api-274120622No ratings yet

- ccc2 4Document1 pageccc2 4api-274120622No ratings yet

- 7 4aDocument2 pages7 4aapi-274120622No ratings yet

- CCC 5Document10 pagesCCC 5api-274120622No ratings yet

- Caleb BorkeDocument1 pageCaleb Borkeapi-274120622No ratings yet

- CCC 6Document2 pagesCCC 6api-274120622No ratings yet

- 7 1aDocument1 page7 1aapi-274120622No ratings yet

- ccc4 3Document1 pageccc4 3api-274120622No ratings yet

- ccc3 5Document1 pageccc3 5api-274120622No ratings yet

- ccc4 1Document1 pageccc4 1api-274120622No ratings yet

- ccc3 2Document1 pageccc3 2api-274120622No ratings yet

- ccc3 4Document1 pageccc3 4api-274120622No ratings yet

- Self 2Document1 pageSelf 2api-274120622No ratings yet

- ccc3 1Document1 pageccc3 1api-274120622No ratings yet

- ccc3 3Document1 pageccc3 3api-274120622No ratings yet

- ccc2 1Document1 pageccc2 1api-274120622No ratings yet

- ch06 CookieDocument4 pagesch06 Cookieapi-2741206220% (1)

- Taller Cinco Caleb BorkeDocument1 pageTaller Cinco Caleb Borkeapi-274120622No ratings yet

- Self Test DaisyDocument1 pageSelf Test Daisyapi-274120622No ratings yet

- CH 08Document8 pagesCH 08api-274120622No ratings yet

- ch08 ProblemDocument9 pagesch08 Problemapi-281193111No ratings yet

- Taller Seis Acco 111Document44 pagesTaller Seis Acco 111api-274120622No ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Tax Invoice: Sold From / Dispatch FromDocument2 pagesTax Invoice: Sold From / Dispatch FromBharat BhushanNo ratings yet

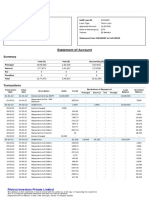

- This Is A System-Generated Statement. Hence, It Does Not Require Any SignatureDocument15 pagesThis Is A System-Generated Statement. Hence, It Does Not Require Any SignaturemohitNo ratings yet

- Canara Bank AssignmentDocument46 pagesCanara Bank AssignmentMukesh Patel50% (2)

- Lacc Wire Transfer Acc.Document1 pageLacc Wire Transfer Acc.Maxim BudanNo ratings yet

- (Foreign Exchange Market-Part1) PDFDocument22 pages(Foreign Exchange Market-Part1) PDFEdward Joseph A. RamosNo ratings yet

- Stress Testing of Jamuna Bank LTDDocument15 pagesStress Testing of Jamuna Bank LTDRahat Ul AminNo ratings yet

- Assignment No 1 Name: Zarish Akram Registration ID: 10731 Course: Islamic Banking and Applied Finance Examples of Riba and GhararDocument3 pagesAssignment No 1 Name: Zarish Akram Registration ID: 10731 Course: Islamic Banking and Applied Finance Examples of Riba and GhararZarish AkramNo ratings yet

- Dav University Jalandhar: Merger of Company: Indusland Bank - Bharat Financial LimitedDocument12 pagesDav University Jalandhar: Merger of Company: Indusland Bank - Bharat Financial LimitedSHAGUN BADYALNo ratings yet

- Reserve Bank of India: Trade Receivable E-Discounting System (Treds)Document18 pagesReserve Bank of India: Trade Receivable E-Discounting System (Treds)omprakash padhi100% (1)

- HDFC Bank Literature ReviewDocument8 pagesHDFC Bank Literature Reviewc5e83cmh100% (1)

- Walt Disney Yen Financing I - Group 8Document6 pagesWalt Disney Yen Financing I - Group 8Sonal Choudhary100% (1)

- Format of Inward Remittance For Export AdvanceDocument2 pagesFormat of Inward Remittance For Export AdvanceKamlesh SonareNo ratings yet

- Problem 5-1, 5-2, 5-6, 5-7 AnswerDocument3 pagesProblem 5-1, 5-2, 5-6, 5-7 AnswerNINIO B. MANIALAGNo ratings yet

- Document 806977650 PDFDocument17 pagesDocument 806977650 PDFshortmycdsNo ratings yet

- Monetary Policy and Central Banking: Geriel I. Fajardo 3FM3 Assignment 2Document3 pagesMonetary Policy and Central Banking: Geriel I. Fajardo 3FM3 Assignment 2Geriel FajardoNo ratings yet

- Indian Banking System AND Basic Banking ConceptsDocument19 pagesIndian Banking System AND Basic Banking ConceptsmanuyadavNo ratings yet

- Swift Car SampleDocument3 pagesSwift Car SampleAjish KumarNo ratings yet

- BPI vs. Intermediate Appellate Court GR# L-66826, August 19, 1988Document2 pagesBPI vs. Intermediate Appellate Court GR# L-66826, August 19, 1988Jolet Paulo Dela CruzNo ratings yet

- Information Sheet Documentary Credit and Stand by Letter of CreditDocument4 pagesInformation Sheet Documentary Credit and Stand by Letter of CreditSally AhmedNo ratings yet

- Loan StatementDocument4 pagesLoan StatementkappilNo ratings yet

- What Is A Cheque Truncation System?Document7 pagesWhat Is A Cheque Truncation System?PrramakrishnanRamaKrishnanNo ratings yet

- Do Women Make Better ManagersDocument8 pagesDo Women Make Better ManagersShatarupa BhattacharyaNo ratings yet

- Ch10depository Transfer ChecksDocument21 pagesCh10depository Transfer ChecksEfad HafizullahNo ratings yet

- Micro FinanceDocument28 pagesMicro FinanceBharat Sai Kiran KNo ratings yet

- Banking Fees and Charges: Section A Rekening Giro 2Document9 pagesBanking Fees and Charges: Section A Rekening Giro 2Baram MadiramNo ratings yet

- GA-SA-F12 (Local - Overseas Travel Expenses Claim Form) Rev4 LockedDocument1 pageGA-SA-F12 (Local - Overseas Travel Expenses Claim Form) Rev4 LockedEroseli IsmailNo ratings yet

- Bank Statements Advice GuideDocument2 pagesBank Statements Advice GuideSãbbìŕ RàhmâñNo ratings yet

- HBLDocument42 pagesHBLsamiNo ratings yet

- A Dissertation Report OnDocument58 pagesA Dissertation Report OnSharathNo ratings yet

- Advisers Blame Each Other For Seizure of IPO Market: Special InvestigationDocument32 pagesAdvisers Blame Each Other For Seizure of IPO Market: Special InvestigationCity A.M.No ratings yet