You might also like

- Book-Keeping and Accounts Level 2/series 2-2009Document13 pagesBook-Keeping and Accounts Level 2/series 2-2009Hein Linn Kyaw60% (10)

- Book-Keeping & Accounts Level 2/series 2 2008 (Code 2007)Document12 pagesBook-Keeping & Accounts Level 2/series 2 2008 (Code 2007)Hein Linn KyawNo ratings yet

- +-LCCI Level 1 - How To Pass Book-Keeping (Recommeded Book) - +Document334 pages+-LCCI Level 1 - How To Pass Book-Keeping (Recommeded Book) - +rock300785% (26)

- LCCI First Level Revision NotesDocument20 pagesLCCI First Level Revision NotesLinda Martin100% (2)

- 2008 LCCI Level1 Book-Keeping (1517-4)Document13 pages2008 LCCI Level1 Book-Keeping (1517-4)JessieChuk100% (2)

- Book-Keeping, Book-Keeping & AccountDocument119 pagesBook-Keeping, Book-Keeping & AccountSiThu60% (5)

- LCCI Accounting First Level 笔记 - 百度文库Document23 pagesLCCI Accounting First Level 笔记 - 百度文库Asok Kumar50% (2)

- L1 Book-Keeping S2 2000Document21 pagesL1 Book-Keeping S2 2000Fung Hui YingNo ratings yet

- Book-Keeping and Accounts/Series-2-2004 (Code2006)Document16 pagesBook-Keeping and Accounts/Series-2-2004 (Code2006)Hein Linn Kyaw100% (4)

- Chapter (1) The Accounting EquationDocument46 pagesChapter (1) The Accounting Equationtunlinoo.067433100% (3)

- Pearson LCCI: Certificate in Bookkeeping and Accounting (VRQ)Document20 pagesPearson LCCI: Certificate in Bookkeeping and Accounting (VRQ)Aung Zaw Htwe100% (2)

- Lcci Level I Que and Ans (1606) MALDocument13 pagesLcci Level I Que and Ans (1606) MALThuzar Lwin100% (2)

- Code 2007 Accounting Level 2 2010 Series 4Document15 pagesCode 2007 Accounting Level 2 2010 Series 4apple_syih100% (1)

- 2010 LCCI Bookkeeping and Accounts Series 3Document8 pages2010 LCCI Bookkeeping and Accounts Series 3Fung Hui Ying75% (4)

- Book-Keeping & Accounts/Series-2-2005 (Code2006)Document14 pagesBook-Keeping & Accounts/Series-2-2005 (Code2006)Hein Linn Kyaw100% (2)

- Lcci Level 1Document32 pagesLcci Level 1Gloria100% (7)

- Book-Keeping and Accounts Level 2Document16 pagesBook-Keeping and Accounts Level 2Hein Linn Kyaw87% (15)

- Level 1 Certificate in Book-Keeping: SyllabusDocument20 pagesLevel 1 Certificate in Book-Keeping: Syllabusvincentho2k100% (1)

- LCCI L2 Bookkeeping and Accounting ASE20093 Jan 2017Document16 pagesLCCI L2 Bookkeeping and Accounting ASE20093 Jan 2017chee pin wongNo ratings yet

- Control AccountsDocument22 pagesControl AccountsLorato Tunah Mokibito100% (1)

- LCCI Chp02Document11 pagesLCCI Chp02richardchan001100% (1)

- LCCI LEVEL 1&2 TextbookDocument100 pagesLCCI LEVEL 1&2 TextbookJohn Sue Han100% (1)

- Book Keeping & Accounts/Series-4-2007 (Code2006)Document13 pagesBook Keeping & Accounts/Series-4-2007 (Code2006)Hein Linn Kyaw100% (2)

- 03 Intro To AccountingDocument407 pages03 Intro To AccountingAllzoommood100% (3)

- FINANCIALREPORTINGand Analysis ExamDocument7 pagesFINANCIALREPORTINGand Analysis ExamKizito KizitoNo ratings yet

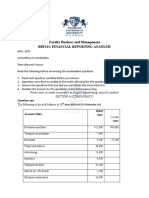

- Faculty Business and Management Bbf211: Financial Reporting AnanlsisDocument7 pagesFaculty Business and Management Bbf211: Financial Reporting AnanlsisMichael AronNo ratings yet

- Financial Accounting: Sample Paper 1Document26 pagesFinancial Accounting: Sample Paper 1HassleBustNo ratings yet

- Bcom 3 Sem Corporate Accounting 1 21100518 Mar 2021Document5 pagesBcom 3 Sem Corporate Accounting 1 21100518 Mar 2021abin.com22No ratings yet

- MQP - MBA - Sem1 - Financial and Management Accounting (DMBA104)Document5 pagesMQP - MBA - Sem1 - Financial and Management Accounting (DMBA104)Rohit SoodNo ratings yet

- Financial Reporting, Statement & Analysis - Assignment1Document5 pagesFinancial Reporting, Statement & Analysis - Assignment1sumanNo ratings yet

- Unit IDocument10 pagesUnit IkuselvNo ratings yet

- IB124 Introduction To Financial Accounting Autumn Term 2020 Seminar QuestionsDocument7 pagesIB124 Introduction To Financial Accounting Autumn Term 2020 Seminar QuestionsS3F1No ratings yet

- F&A Level II (Paper B)Document6 pagesF&A Level II (Paper B)almmohamed294No ratings yet

- 11th AccountsDocument8 pages11th AccountsShubham sumbriaNo ratings yet

- Chapter 8 - Notes Payable and Debt Restructuring: Problem 8-7Document3 pagesChapter 8 - Notes Payable and Debt Restructuring: Problem 8-7Pau LaguertaNo ratings yet

- Sample QuestionsDocument3 pagesSample QuestionstulikaNo ratings yet

- AC191 Autumn 2011 FINALDocument9 pagesAC191 Autumn 2011 FINALgerlaniamelgacoNo ratings yet

- Acc Nov2012 P2Document13 pagesAcc Nov2012 P2gibbamanjexNo ratings yet

- Frq-Acc-Grade 11-Set 05Document3 pagesFrq-Acc-Grade 11-Set 05itzmellowteaNo ratings yet

- 3 G'S Joint Evaluation Exam.: NAME ..INDEX NO DATEDocument3 pages3 G'S Joint Evaluation Exam.: NAME ..INDEX NO DATEWriter BettyNo ratings yet

- DR CR Le LeDocument7 pagesDR CR Le LeKANGOMA FODIE MansarayNo ratings yet

- Income Statement TutorialDocument5 pagesIncome Statement TutorialKhiren MenonNo ratings yet

- S1 BookKeep 2nd Sem Final ExamDocument3 pagesS1 BookKeep 2nd Sem Final ExamTan Shu YuinNo ratings yet

- L1-June 2013-FINANCIAL REPORTINGDocument25 pagesL1-June 2013-FINANCIAL REPORTINGMetick MicaiahNo ratings yet

- NKT/KS/17/4468: NXO-21328 1 (Contd.)Document3 pagesNKT/KS/17/4468: NXO-21328 1 (Contd.)Namrata RamgadeNo ratings yet

- MN-M001 Online 24 Hour Exam - January 2024 FINAL - 240115 - 093952Document5 pagesMN-M001 Online 24 Hour Exam - January 2024 FINAL - 240115 - 093952szj00247No ratings yet

- Instructions To Candidates:: Question 1 Continues OverleafDocument3 pagesInstructions To Candidates:: Question 1 Continues OverleafAung Kyaw HtayNo ratings yet

- Grade 10 Provincial Case Study QP 2023Document5 pagesGrade 10 Provincial Case Study QP 2023kwazy dlaminiNo ratings yet

- Entrepreneurship22 PDFDocument3 pagesEntrepreneurship22 PDFSean DineverrNo ratings yet

- London Examinations GCE: Accounting (Modular Syllabus) Advanced Subsidiary/Advanced LevelDocument16 pagesLondon Examinations GCE: Accounting (Modular Syllabus) Advanced Subsidiary/Advanced Levelrahat879No ratings yet

- Final Account WorksheetDocument4 pagesFinal Account Worksheetravikumarbadass0No ratings yet

- Accounting - Higherlevel: Leaving Certificate Examination, 2000Document10 pagesAccounting - Higherlevel: Leaving Certificate Examination, 2000meelas123No ratings yet

- Paper 3Document2 pagesPaper 3Raja Mohan RaviNo ratings yet

- RE Exam FA Sem I MFM MMM MHRDMDocument4 pagesRE Exam FA Sem I MFM MMM MHRDMPARAM CLOTHINGNo ratings yet

- Tutorial 9: Statement of Cash FlowsDocument1 pageTutorial 9: Statement of Cash FlowsCheng Win-YarnNo ratings yet

- 2009 S3 Ase2007Document15 pages2009 S3 Ase2007May CcmNo ratings yet

- Accounts Assignment Class 11 CandE 20220111131012374Document5 pagesAccounts Assignment Class 11 CandE 20220111131012374Jithu EmmanuelNo ratings yet

- CAC1101201008 Financial Accounting 1ADocument6 pagesCAC1101201008 Financial Accounting 1AGift MoyoNo ratings yet

- Ayeesha - Principles of Management AccountingDocument5 pagesAyeesha - Principles of Management AccountingMahesh KumarNo ratings yet

- 9706 w03 QP 4Document8 pages9706 w03 QP 4roukaiya_peerkhanNo ratings yet

- Ministry of Planning, Finance and Industry - Notification 86-2019 0Document2 pagesMinistry of Planning, Finance and Industry - Notification 86-2019 0Hein Linn KyawNo ratings yet

- Introduction To Statistics PGDBDocument42 pagesIntroduction To Statistics PGDBHein Linn KyawNo ratings yet

- GMAT Reading ComprehensionDocument5 pagesGMAT Reading ComprehensionHein Linn KyawNo ratings yet

- Organization DataDocument23 pagesOrganization DataHein Linn KyawNo ratings yet

- Book Keeping & Accounts/Series-2-2007 (Code2006)Document12 pagesBook Keeping & Accounts/Series-2-2007 (Code2006)Hein Linn Kyaw100% (2)

- Book Keeping & Accounts/Series-3-2007 (Code2006)Document11 pagesBook Keeping & Accounts/Series-3-2007 (Code2006)Hein Linn Kyaw100% (3)

- Cost Accounting/Series-3-2007 (Code3016)Document18 pagesCost Accounting/Series-3-2007 (Code3016)Hein Linn Kyaw50% (6)

- Management Accounting/Series-3-2007 (Code3023)Document15 pagesManagement Accounting/Series-3-2007 (Code3023)Hein Linn Kyaw100% (1)

- Accounting (IAS) /series 4 2007 (Code3901)Document17 pagesAccounting (IAS) /series 4 2007 (Code3901)Hein Linn Kyaw0% (1)

- Accounting/Series 2 2007 (Code3001)Document16 pagesAccounting/Series 2 2007 (Code3001)Hein Linn Kyaw100% (3)

- Accounting/Series 3 2007 (Code3001)Document18 pagesAccounting/Series 3 2007 (Code3001)Hein Linn KyawNo ratings yet

- Business Statstics/Series-3-2007 (Code3009)Document20 pagesBusiness Statstics/Series-3-2007 (Code3009)Hein Linn Kyaw100% (1)

- Management Accounting: Level 3Document18 pagesManagement Accounting: Level 3Hein Linn Kyaw100% (3)

- Accounting/Series 4 2007 (Code3001)Document17 pagesAccounting/Series 4 2007 (Code3001)Hein Linn Kyaw100% (2)

- Business Statstics/Series-4-2007 (Code-3009)Document22 pagesBusiness Statstics/Series-4-2007 (Code-3009)Hein Linn KyawNo ratings yet

- Advanced Business Calculation/Series-4-2007 (Code3003)Document13 pagesAdvanced Business Calculation/Series-4-2007 (Code3003)Hein Linn Kyaw100% (6)

- Management Accounting Level 3: LCCI International QualificationsDocument15 pagesManagement Accounting Level 3: LCCI International QualificationsHein Linn Kyaw100% (1)

- Cost Accounting: Level 3Document19 pagesCost Accounting: Level 3Hein Linn Kyaw100% (1)

- Cost Accounting/Series-4-2011 (Code3017)Document17 pagesCost Accounting/Series-4-2011 (Code3017)Hein Linn Kyaw100% (2)

- Accounting (IAS) /series 4 2011 (Code3902)Document16 pagesAccounting (IAS) /series 4 2011 (Code3902)Hein Linn Kyaw75% (4)

- Book Keeping & Accounts/Series-4-2007 (Code2006)Document13 pagesBook Keeping & Accounts/Series-4-2007 (Code2006)Hein Linn Kyaw100% (2)

- Book-Keeping and Accounts/Series-4-2011 (Code2007)Document16 pagesBook-Keeping and Accounts/Series-4-2011 (Code2007)Hein Linn Kyaw100% (1)

- Cost Accounting Level 3: LCCI International QualificationsDocument20 pagesCost Accounting Level 3: LCCI International QualificationsHein Linn Kyaw33% (3)

- Management Accounting/Series-4-2011 (Code3024)Document18 pagesManagement Accounting/Series-4-2011 (Code3024)Hein Linn Kyaw100% (2)

- Accounting/Series 4 2011 (Code30124)Document16 pagesAccounting/Series 4 2011 (Code30124)Hein Linn Kyaw100% (1)

- Advanced Business Calculations/Series-4-2011 (Code3003)Document12 pagesAdvanced Business Calculations/Series-4-2011 (Code3003)Hein Linn Kyaw100% (12)

- Business Statstics/Series-4-2011 (Code3009)Document18 pagesBusiness Statstics/Series-4-2011 (Code3009)Hein Linn KyawNo ratings yet

- Business Statistics Level 3: LCCI International QualificationsDocument22 pagesBusiness Statistics Level 3: LCCI International QualificationsHein Linn Kyaw100% (1)

- Accounting (IAS) Level 3: LCCI International QualificationsDocument14 pagesAccounting (IAS) Level 3: LCCI International QualificationsHein Linn Kyaw50% (2)

- Lcci Level3 Solution Past Paper Series 3-10Document14 pagesLcci Level3 Solution Past Paper Series 3-10tracyduckk67% (3)

- Bautista Vs CADocument3 pagesBautista Vs CAKristel Hipolito100% (1)

- StatementOfAccount 50373717340 16072023 154959Document19 pagesStatementOfAccount 50373717340 16072023 154959Ajay GuptaNo ratings yet

- Cash & Cash Equivalents (Viajar Basis)Document38 pagesCash & Cash Equivalents (Viajar Basis)Nicole Daphne FigueroaNo ratings yet

- CONTRACT RATESDocument4 pagesCONTRACT RATESRiski W PratamaNo ratings yet

- Chapter 27 UpdatedDocument18 pagesChapter 27 UpdatedIBn RefatNo ratings yet

- Og 20 9906 1806 00039107up25y1732 PDFDocument5 pagesOg 20 9906 1806 00039107up25y1732 PDFTota Ram MouryaNo ratings yet

- Lazada Return FormDocument1 pageLazada Return FormLeez1778% (9)

- Mercantile Law 2016 Bar Examinations No AnswersDocument4 pagesMercantile Law 2016 Bar Examinations No AnswersDiane Dee YaneeNo ratings yet

- PGSS Member HandbookDocument133 pagesPGSS Member Handbookdgfman63No ratings yet

- PTR UsermanualDocument25 pagesPTR UsermanualDSEU Campus GBPIT OkhlaNo ratings yet

- Provident Fund - SynopsisDocument9 pagesProvident Fund - SynopsisSIDDHANT MOHAPATRANo ratings yet

- Chase Bank Statement SummaryDocument4 pagesChase Bank Statement Summaryyungler0% (2)

- Artifact 7 - PF Withdrawal (Form 19) TESLDocument4 pagesArtifact 7 - PF Withdrawal (Form 19) TESLShiva Ram ReddyNo ratings yet

- My StatementDocument9 pagesMy StatementAjayNo ratings yet

- PDFDocument4 pagesPDFLALIT KUMARNo ratings yet

- Application For Caliming of Unpaid DividendDocument2 pagesApplication For Caliming of Unpaid DividendCA Bharat JainNo ratings yet

- ESS - Claim SystemDocument20 pagesESS - Claim Systemleonheart_chia27No ratings yet

- Terms & Conditions For 811 Account OpeningDocument8 pagesTerms & Conditions For 811 Account OpeningMr. UNKNOWN manNo ratings yet

- Ibasco Vs CADocument6 pagesIbasco Vs CAGlorious El DomineNo ratings yet

- 138 Notice-Manoj ParveDocument3 pages138 Notice-Manoj ParvemanojNo ratings yet

- Internship Report Askari BankDocument107 pagesInternship Report Askari Bankafgan52No ratings yet

- LCCI Level 3 2009 Tests PDFDocument19 pagesLCCI Level 3 2009 Tests PDFzsoieNo ratings yet

- PAD Agreement enDocument2 pagesPAD Agreement enGangsta101No ratings yet

- Negotiable Instruments BasicsDocument171 pagesNegotiable Instruments BasicsJøñë ÊphrèmNo ratings yet

- Agrani Bank Internship ReportDocument71 pagesAgrani Bank Internship ReportRobiRashedNo ratings yet

- Documenting Expenses: ReceiptDocument2 pagesDocumenting Expenses: ReceiptARJUN ANANDNo ratings yet

- Settlement Letter 3359100Document3 pagesSettlement Letter 3359100Mahesh DangodeNo ratings yet

- Job No.: #67123: National Highways Authority of IndiaDocument34 pagesJob No.: #67123: National Highways Authority of IndiaBal RajNo ratings yet

- BillSummary - 2021 10 22Document43 pagesBillSummary - 2021 10 22iyas14No ratings yet

- Financial Accounting 1 Unit 9Document23 pagesFinancial Accounting 1 Unit 9chuchuNo ratings yet