You might also like

- Replacement Theory MABDocument16 pagesReplacement Theory MABBabasab Patil (Karrisatte)No ratings yet

- Cost Analysis: Presented By: Anindita Samajpati Sonam Aggarwal Sonal Taneja Pankaj MahajanDocument18 pagesCost Analysis: Presented By: Anindita Samajpati Sonam Aggarwal Sonal Taneja Pankaj Mahajansonal_tanejaNo ratings yet

- Auto Logisitcs ReportDocument218 pagesAuto Logisitcs ReportistyloankurNo ratings yet

- Using Cost-Time Profile For Value Stream OptimizationDocument9 pagesUsing Cost-Time Profile For Value Stream OptimizationBagas KaraNo ratings yet

- Shruti Assignment 2Document25 pagesShruti Assignment 2Shruti SuryawanshiNo ratings yet

- COMSATS HRM LECTURE NOTES CHAPTER 17-24Document37 pagesCOMSATS HRM LECTURE NOTES CHAPTER 17-24Moh RoshiNo ratings yet

- Module 1 - Introduction and Management Decision Making - Homework SolutionsDocument4 pagesModule 1 - Introduction and Management Decision Making - Homework SolutionsAbelNo ratings yet

- Introduction To SCMDocument38 pagesIntroduction To SCMArif Shan50% (2)

- Transportation ModelsDocument106 pagesTransportation ModelsNguyễn Sơn LâmNo ratings yet

- Procter & Gamble: Using Agent Based Modeling and RFID: Supply Chain ManagementDocument18 pagesProcter & Gamble: Using Agent Based Modeling and RFID: Supply Chain ManagementJames KudrowNo ratings yet

- SCM 16 Transportation Management - Part-2Document11 pagesSCM 16 Transportation Management - Part-2swagat mohapatra100% (1)

- Online Mid-Term POM May-Aug 2020 G-6Document5 pagesOnline Mid-Term POM May-Aug 2020 G-6Hossain TanjilaNo ratings yet

- InventoryDocument34 pagesInventorymbapritiNo ratings yet

- Marginal Costing & Absorption Costing Profit ReconciliationDocument7 pagesMarginal Costing & Absorption Costing Profit ReconciliationCourage KanyonganiseNo ratings yet

- 2011 LSCM Lesson1 Logistics PDFDocument83 pages2011 LSCM Lesson1 Logistics PDFAnkita Agarwal67% (3)

- Statistics 2 Marks and Notes 2019Document37 pagesStatistics 2 Marks and Notes 2019ANITHA ANo ratings yet

- Martin Christopher 4 PDFDocument11 pagesMartin Christopher 4 PDFVangelis Rodopoulos100% (1)

- Case Summary TaxDocument8 pagesCase Summary TaxSaurav MahtoNo ratings yet

- Basic Concepts of Supply Chain ManagementDocument42 pagesBasic Concepts of Supply Chain ManagementMarcela BerrocalNo ratings yet

- 2008 Reverse Logistics Strategies For End-Of-life ProductsDocument22 pages2008 Reverse Logistics Strategies For End-Of-life ProductsValen Ramirez HNo ratings yet

- Cost Accounting AssignmentDocument3 pagesCost Accounting AssignmentMkaeDizonNo ratings yet

- Inventory Models Chapter Explains Economic Order Quantity and Reorder Point DecisionsDocument17 pagesInventory Models Chapter Explains Economic Order Quantity and Reorder Point DecisionshidayatsadikinNo ratings yet

- Engineering Economics and Financial AccountingDocument5 pagesEngineering Economics and Financial AccountingAkvijayNo ratings yet

- Standard Costing Concept and DeterminationDocument33 pagesStandard Costing Concept and DeterminationRASHIDABOLTWALANo ratings yet

- Logistics Problems and SolutionsDocument11 pagesLogistics Problems and SolutionsSailpoint CourseNo ratings yet

- Direct Product ProfitDocument5 pagesDirect Product Profitahmed_23zulfiqarNo ratings yet

- BU330 Accounting For ManagerDocument88 pagesBU330 Accounting For ManagerG Jha100% (1)

- 1898 Ford Operations ManagementDocument8 pages1898 Ford Operations ManagementSanthoshAnvekarNo ratings yet

- Mission Flow DiagramDocument1 pageMission Flow DiagramAnees Ethiyil KunjumuhammedNo ratings yet

- A Project On The Economic Order QuantityDocument26 pagesA Project On The Economic Order QuantityFortune Fmx MushongaNo ratings yet

- International Purchasing Environment Doc2Document5 pagesInternational Purchasing Environment Doc2Eric Kipkemoi33% (3)

- Executive SummaryDocument11 pagesExecutive SummaryNitish Kumar SinghNo ratings yet

- IEE 534 Supply Chain Modeling and AnalysisDocument2 pagesIEE 534 Supply Chain Modeling and AnalysisindiolandNo ratings yet

- Lean ManufacturingDocument11 pagesLean ManufacturingraisehellNo ratings yet

- Infrastructure Issues and New Developments in The Warehousing IndustryDocument49 pagesInfrastructure Issues and New Developments in The Warehousing Industrypyla jyothiNo ratings yet

- Sai Aswathy. SCM 2 03Document8 pagesSai Aswathy. SCM 2 03sudeepptrNo ratings yet

- SCM Module 3Document31 pagesSCM Module 3suhu.15No ratings yet

- Logistical Interfaces With ProcurementDocument7 pagesLogistical Interfaces With ProcurementJaymark CasingcaNo ratings yet

- Opportunity Cost, Marginal Analysis, RationalismDocument33 pagesOpportunity Cost, Marginal Analysis, Rationalismbalram nayakNo ratings yet

- I.R. Chapter-2 Dr. K.panditDocument10 pagesI.R. Chapter-2 Dr. K.panditDeepak KumarNo ratings yet

- McVeggie Burger: How McDonald's Developed Its First Beef-less Menu ItemDocument19 pagesMcVeggie Burger: How McDonald's Developed Its First Beef-less Menu ItemAashi LuniaNo ratings yet

- Chapter OverviewDocument57 pagesChapter OverviewWajiha SharifNo ratings yet

- Pom Inventory ProblemsDocument8 pagesPom Inventory ProblemsSharath Kannan0% (2)

- PGDM OM 3.3 Material ManagementDocument1 pagePGDM OM 3.3 Material ManagementAlok SinghNo ratings yet

- BBM & Bcom SyllabusDocument79 pagesBBM & Bcom Syllabusyathsih24885100% (2)

- Course Outline - ToM - Dr. Rameez KhalidDocument1 pageCourse Outline - ToM - Dr. Rameez KhalidAbid ButtNo ratings yet

- Maximizing profit for newspaper salesDocument12 pagesMaximizing profit for newspaper salesBhargav D.S.No ratings yet

- Supply Chain DriversDocument27 pagesSupply Chain DriversLakshmi VennelaNo ratings yet

- Objectives of Supply Chain ManagementDocument2 pagesObjectives of Supply Chain ManagementRavi KumarNo ratings yet

- Working of Domestic RefrigiratorDocument15 pagesWorking of Domestic Refrigiratorspursh67% (3)

- Cost & Management Practices in India AssignmentDocument25 pagesCost & Management Practices in India AssignmentAkhil ManglaNo ratings yet

- PDSA Cycle Explained Tools for ChangeDocument21 pagesPDSA Cycle Explained Tools for Changejose luisNo ratings yet

- Ch08 - InventoryDocument112 pagesCh08 - InventoryAdam Yans JrNo ratings yet

- AssDocument2 pagesAssAndree ChicaizaNo ratings yet

- Chapter 5 MRP ErpDocument22 pagesChapter 5 MRP ErpKelly ObrienNo ratings yet

- Handwritten assignment on cost and management accountingDocument6 pagesHandwritten assignment on cost and management accountingJayaKhemaniNo ratings yet

- Cost Estimation Meaning of CostDocument9 pagesCost Estimation Meaning of CostMatinChris KisomboNo ratings yet

- Costing Objectives Semester VDocument7 pagesCosting Objectives Semester VytsNo ratings yet

- Management AccountingDocument112 pagesManagement AccountingSugandha Sethia100% (1)

- MBA 7214 - Practice Exam With The AnswersDocument9 pagesMBA 7214 - Practice Exam With The AnswersAnkit ChoudharyNo ratings yet

- Characteristics and Economic Outlook of Indonesia in the Globalization EraDocument63 pagesCharacteristics and Economic Outlook of Indonesia in the Globalization EraALIFAHNo ratings yet

- CRM ProcessDocument9 pagesCRM ProcesssamridhdhawanNo ratings yet

- Social ResponsibilityDocument2 pagesSocial ResponsibilityAneeq Raheem100% (1)

- Josh Magazine NMAT 2007 Quest 4Document43 pagesJosh Magazine NMAT 2007 Quest 4Pristine Charles100% (1)

- Alifian Faiz NovendiDocument5 pagesAlifian Faiz Novendialifianovendi 11No ratings yet

- FM 422Document8 pagesFM 422Harmaein KuaNo ratings yet

- Bitcoin Dicebot Script WorkingDocument3 pagesBitcoin Dicebot Script WorkingMaruel MeyerNo ratings yet

- October Month Progress ReportDocument12 pagesOctober Month Progress ReportShashi PrakashNo ratings yet

- Sharma Industries (SI) : Structural Dilemma: Group No - 2Document5 pagesSharma Industries (SI) : Structural Dilemma: Group No - 2PRATIK RUNGTANo ratings yet

- CH 31 Open-Economy Macroeconomics Basic ConceptsDocument52 pagesCH 31 Open-Economy Macroeconomics Basic ConceptsveroirenNo ratings yet

- Construction EngineeringDocument45 pagesConstruction EngineeringDr Olayinka Okeola100% (4)

- Comparative Analysis of Broking FirmsDocument12 pagesComparative Analysis of Broking FirmsJames RamirezNo ratings yet

- HR McqsDocument12 pagesHR McqsHammadNo ratings yet

- Thyrocare Technologies Ltd. - IPODocument4 pagesThyrocare Technologies Ltd. - IPOKalpeshNo ratings yet

- Exchange RatesDocument11 pagesExchange RatesElizavetaNo ratings yet

- Seminar Assignments Multiple Choice Questions City Size Growth PDFDocument4 pagesSeminar Assignments Multiple Choice Questions City Size Growth PDFminlwintheinNo ratings yet

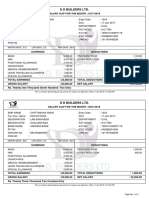

- Blkpay YyyymmddDocument4 pagesBlkpay YyyymmddRamesh PatelNo ratings yet

- AssignmentDocument8 pagesAssignmentnaabbasiNo ratings yet

- Capital Budgeting Project Instruction RubricDocument3 pagesCapital Budgeting Project Instruction RubricSunil Kumar0% (1)

- EH101 Course InformationDocument1 pageEH101 Course InformationCharles Bromley-DavenportNo ratings yet

- Bahco Chile 2021Document160 pagesBahco Chile 2021victor guajardoNo ratings yet

- Crop Insurance - BrazilDocument3 pagesCrop Insurance - Brazilanandekka84No ratings yet

- 6021-P3-Lembar KerjaDocument48 pages6021-P3-Lembar KerjaikhwanNo ratings yet

- G4-Strataxman-Bir Form and DeadlinesDocument4 pagesG4-Strataxman-Bir Form and DeadlinesKristen StewartNo ratings yet

- Fruits & Veg DatabaseDocument23 pagesFruits & Veg Databaseyaseer303No ratings yet

- Find payment channels in Aklan provinceDocument351 pagesFind payment channels in Aklan provincejhoanNo ratings yet

- Pay - Slip Oct. & Nov. 19Document1 pagePay - Slip Oct. & Nov. 19Atul Kumar MishraNo ratings yet

- Risk Assessment For Grinding Work: Classic Builders and DevelopersDocument3 pagesRisk Assessment For Grinding Work: Classic Builders and DevelopersradeepNo ratings yet

- Tour Guiding Introduction to the Tourism IndustryDocument13 pagesTour Guiding Introduction to the Tourism Industryqueenie esguerraNo ratings yet

- As of December 2, 2010: MHA Handbook v3.0 1Document170 pagesAs of December 2, 2010: MHA Handbook v3.0 1jadlao8000dNo ratings yet

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (12)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetFrom EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNo ratings yet

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- Profit First for Therapists: A Simple Framework for Financial FreedomFrom EverandProfit First for Therapists: A Simple Framework for Financial FreedomNo ratings yet

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItFrom EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItRating: 5 out of 5 stars5/5 (13)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Basic Accounting: Service Business Study GuideFrom EverandBasic Accounting: Service Business Study GuideRating: 5 out of 5 stars5/5 (2)

- Bookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesFrom EverandBookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesRating: 4.5 out of 5 stars4.5/5 (30)

- Project Control Methods and Best Practices: Achieving Project SuccessFrom EverandProject Control Methods and Best Practices: Achieving Project SuccessNo ratings yet

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Mysap Fi Fieldbook: Fi Fieldbuch Auf Der Systeme Anwendungen Und Produkte in Der DatenverarbeitungFrom EverandMysap Fi Fieldbook: Fi Fieldbuch Auf Der Systeme Anwendungen Und Produkte in Der DatenverarbeitungRating: 4 out of 5 stars4/5 (1)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyFrom EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyRating: 4 out of 5 stars4/5 (4)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet