You might also like

- MB0025 Financial Management AccountingDocument10 pagesMB0025 Financial Management AccountingTaran Deep SinghNo ratings yet

- Rancho Foods Deposits All Cash Receipts Each Wednesday and FridayDocument1 pageRancho Foods Deposits All Cash Receipts Each Wednesday and FridayAmit PandeyNo ratings yet

- How to reconcile a bank statementDocument1 pageHow to reconcile a bank statementAnkita T. Moore100% (1)

- 5f388b962f84e - BANK RECONCILIATION STATEMENT PDFDocument4 pages5f388b962f84e - BANK RECONCILIATION STATEMENT PDFYogesh ChaulagaiNo ratings yet

- EngineeringMathematics II (SP) PDFDocument1 pageEngineeringMathematics II (SP) PDFrahul m nairNo ratings yet

- The Accounting Process (The Accounting Cycle) : 2. Prepare The Transaction'sDocument3 pagesThe Accounting Process (The Accounting Cycle) : 2. Prepare The Transaction'sGanesh ZopeNo ratings yet

- Accounting For Business (15 Credits)Document3 pagesAccounting For Business (15 Credits)cuongaccNo ratings yet

- Accounts - Bank Reconciliation StatementDocument18 pagesAccounts - Bank Reconciliation StatementAnuj KutalNo ratings yet

- ACC 211 - Review 2 (Chapters 5, 6, & 7) SolutionDocument5 pagesACC 211 - Review 2 (Chapters 5, 6, & 7) SolutionBrennan Patrick WynnNo ratings yet

- Bank Reconciliation AprilDocument3 pagesBank Reconciliation AprilAnonymous FAlrXF100% (1)

- SLURRY FLOW IN MILLS: GRATE DISCHARGE MECHANISMDocument24 pagesSLURRY FLOW IN MILLS: GRATE DISCHARGE MECHANISMJavier OyarceNo ratings yet

- Business English SamplesDocument13 pagesBusiness English SamplesMarina PeshovskaNo ratings yet

- Introduction to Data Interpretation (DIDocument3 pagesIntroduction to Data Interpretation (DINavdeep AhlawatNo ratings yet

- Principle of EngineeringDocument206 pagesPrinciple of EngineeringbmhshNo ratings yet

- Bank Reconciliation StatementDocument3 pagesBank Reconciliation StatementzB13No ratings yet

- Nov07 Mathematics IIIDocument8 pagesNov07 Mathematics IIIandhracollegesNo ratings yet

- Midterm Bi ADocument13 pagesMidterm Bi AFabiana BarbeiroNo ratings yet

- Mathematics III MAY2003 or 220556Document2 pagesMathematics III MAY2003 or 220556Nizam Institute of Engineering and Technology LibraryNo ratings yet

- ACTBAS 2 - Lecture 7 Internal Control and Cash, Bank ReconciliationDocument5 pagesACTBAS 2 - Lecture 7 Internal Control and Cash, Bank ReconciliationJason Robert MendozaNo ratings yet

- Peak Performance Instruction SheetDocument2 pagesPeak Performance Instruction SheetnamnblobNo ratings yet

- 293 Financial Accounting - COURSE OUTLINEDocument7 pages293 Financial Accounting - COURSE OUTLINEsilenteyesNo ratings yet

- Engineering Mathematics Topic 5Document2 pagesEngineering Mathematics Topic 5cyclopsoctopusNo ratings yet

- Cyber CrimeDocument2 pagesCyber CrimeDondi de MesaNo ratings yet

- Catholic Bible: Midterm Performance Task "Catholic and Protestant Bible: Advantages and Disadvantages"Document3 pagesCatholic Bible: Midterm Performance Task "Catholic and Protestant Bible: Advantages and Disadvantages"kaitNo ratings yet

- ACCT 2001 Exam 2 Review ProblemsDocument11 pagesACCT 2001 Exam 2 Review Problemsdpa7020No ratings yet

- The Bigger Wave of Hallyu in Indonesia - GlocalizationDocument12 pagesThe Bigger Wave of Hallyu in Indonesia - GlocalizationGlobal Research and Development ServicesNo ratings yet

- Accounting vs. Auditing: The Origins of AuditingDocument2 pagesAccounting vs. Auditing: The Origins of AuditingAbdu Mohammed100% (2)

- Financial AccountingDocument4 pagesFinancial AccountingnileshkambleNo ratings yet

- Benefits and Challenges of IFRS Convergence and ApplicationDocument4 pagesBenefits and Challenges of IFRS Convergence and ApplicationCristina Andreea MNo ratings yet

- Quizzer (Cash To Inventory Valuation) KeyDocument10 pagesQuizzer (Cash To Inventory Valuation) KeyLouie Miguel DulguimeNo ratings yet

- Accounting Business Law FinanceDocument8 pagesAccounting Business Law FinanceromeeNo ratings yet

- Background Information2Document6 pagesBackground Information2Karen Laccay50% (2)

- Optimize Cash ControlsDocument18 pagesOptimize Cash ControlsAhmed RawyNo ratings yet

- Foreign Currency Translation - Modified.aDocument71 pagesForeign Currency Translation - Modified.asamuel debebeNo ratings yet

- Computerized AccountingDocument14 pagesComputerized Accountinglayyah2013No ratings yet

- Limitations of Financial AccountingDocument2 pagesLimitations of Financial Accountingegorlinus100% (2)

- CH 4Document73 pagesCH 4Ella ApeloNo ratings yet

- Chapter 6 MC Employee Fraud and The Audit of CashDocument7 pagesChapter 6 MC Employee Fraud and The Audit of CashJames HNo ratings yet

- Financial Accounting: A: How To Study AccountingDocument29 pagesFinancial Accounting: A: How To Study Accountingrishi_positive1195No ratings yet

- Study Habits and Academic Performance of 2nd Year Psychology Students of Cavite State University - Imus CampusDocument3 pagesStudy Habits and Academic Performance of 2nd Year Psychology Students of Cavite State University - Imus CampusDeonne TumaganNo ratings yet

- V Semster Mechanical Engineering RTMNU NagpurDocument15 pagesV Semster Mechanical Engineering RTMNU NagpurAnand NilewarNo ratings yet

- Foreign Currency TranslationDocument38 pagesForeign Currency TranslationAnmol Gulati100% (1)

- Financial Accounting A Managerial Perspective PDFDocument3 pagesFinancial Accounting A Managerial Perspective PDFSabyasachi KarNo ratings yet

- 13D91101 Higher Engineering MathematicsDocument1 page13D91101 Higher Engineering MathematicsAjay KumarNo ratings yet

- MAS Upgrade 4.50 Information PackageDocument98 pagesMAS Upgrade 4.50 Information PackageWayne SchulzNo ratings yet

- Not For Profit EntitiesDocument57 pagesNot For Profit EntitiesGreg DomingoNo ratings yet

- XE Engineering Maths SectionsDocument1 pageXE Engineering Maths SectionsTommyVercettiNo ratings yet

- Engineering Mathematics Statistics Finance ProposalDocument8 pagesEngineering Mathematics Statistics Finance ProposalXiaokang WangNo ratings yet

- Financial Accounting Part 3Document24 pagesFinancial Accounting Part 3dannydolyNo ratings yet

- Accounting For Business CombinationsDocument116 pagesAccounting For Business CombinationsarakeelNo ratings yet

- Business Combination: Consolidated Financial StatementsDocument9 pagesBusiness Combination: Consolidated Financial StatementsJuuzuu GearNo ratings yet

- Final Chapter 6Document14 pagesFinal Chapter 6zynab123No ratings yet

- Analysis For Cash FlowDocument31 pagesAnalysis For Cash FlowRaja Tejas YerramalliNo ratings yet

- Chapter07 - AnswerDocument18 pagesChapter07 - AnswerkdsfeslNo ratings yet

- Heat Transfer May2004 NR 310803Document8 pagesHeat Transfer May2004 NR 310803Nizam Institute of Engineering and Technology LibraryNo ratings yet

- ch05 SolDocument18 pagesch05 SolJohn Nigz Payee100% (1)

- Chap05-Completing The Accounting CycleDocument23 pagesChap05-Completing The Accounting CycleParesh PrasadNo ratings yet

- Solutions Chapter 7Document39 pagesSolutions Chapter 7Brenda Wijaya100% (2)

- Chapter 06 PDFDocument24 pagesChapter 06 PDFadarshNo ratings yet

- Practice Questions Inventories # 2 With AnswersDocument9 pagesPractice Questions Inventories # 2 With AnswersIzzahIkramIllahiNo ratings yet

- A Study On Green Banking in India - An: Commerce Original Research PaperDocument3 pagesA Study On Green Banking in India - An: Commerce Original Research PaperAnitha RNo ratings yet

- Cliffton Valley Price ListDocument2 pagesCliffton Valley Price Listsishir mandalNo ratings yet

- SAP FI PracticeDocument101 pagesSAP FI Practicenaimdelhi100% (2)

- Deposit Slip CertificateDocument1 pageDeposit Slip CertificateMalou AblazaNo ratings yet

- 01 Handouts Mrunal Economy Batch Code CSP20Document19 pages01 Handouts Mrunal Economy Batch Code CSP20dbiswajitNo ratings yet

- PM Scholarship Scheme Acknowledgement Slip GuideDocument40 pagesPM Scholarship Scheme Acknowledgement Slip GuidehimcstechNo ratings yet

- South AfricaDocument40 pagesSouth AfricaSofy SofyaNo ratings yet

- Credit and Collection Chapter 2Document45 pagesCredit and Collection Chapter 2BEA CARMONANo ratings yet

- Advanced Electronic BankingDocument21 pagesAdvanced Electronic BankingEmmanuel HernandezNo ratings yet

- FICA DocumentsDocument30 pagesFICA DocumentsJayaprakash ReddyNo ratings yet

- Utility Powertech Limited: Notice Inviting E-TenderDocument3 pagesUtility Powertech Limited: Notice Inviting E-Tenderashishntpc1309No ratings yet

- Financial Markets and Institutions AssignmentDocument40 pagesFinancial Markets and Institutions AssignmentAhsan khanNo ratings yet

- Unit 2Document11 pagesUnit 2Tuyên ThanhNo ratings yet

- HS Business Administration Core Sample ExamDocument33 pagesHS Business Administration Core Sample ExamMuhammadIjazAslamNo ratings yet

- Rosa Lim Found Guilty of Issuing Worthless ChecksDocument4 pagesRosa Lim Found Guilty of Issuing Worthless ChecksRam PagongNo ratings yet

- Digest of NI ActDocument185 pagesDigest of NI Actseachu67% (3)

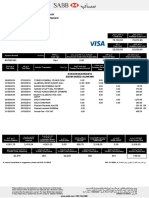

- SABB Platinum Visa Credit Card StatementDocument2 pagesSABB Platinum Visa Credit Card Statementsabah alsannaa100% (1)

- Https LMC - Up.nic - in Internet AuthenticatedUser TaxSubmit - AspxDocument2 pagesHttps LMC - Up.nic - in Internet AuthenticatedUser TaxSubmit - AspxRanju TripathiNo ratings yet

- Bop Internship ReportDocument70 pagesBop Internship Reportiqarah100% (4)

- Tax Invoice: Abhishek GoenkaDocument1 pageTax Invoice: Abhishek GoenkaSaurabh ChaudharyNo ratings yet

- PCBUDocument1 pagePCBUchityalasriaktnh0000No ratings yet

- Downloaded DocumentDocument7 pagesDownloaded DocumentStacie GlanceNo ratings yet

- ABA Principles of Banking Table of ContentsDocument11 pagesABA Principles of Banking Table of ContentsCápMinhQuyền0% (3)

- New Microsoft Word DocumentDocument10 pagesNew Microsoft Word Documentमहेश कुमार मीनाNo ratings yet

- NGO Registration FormDocument4 pagesNGO Registration Formrachit-malviya-421367% (6)

- Gmed General Terms of Sale and Provision of Services December 2020Document1 pageGmed General Terms of Sale and Provision of Services December 2020Chan StephenNo ratings yet

- How To Read Your MT4 Trading StatementDocument7 pagesHow To Read Your MT4 Trading StatementwanfaroukNo ratings yet

- EyeforTravel - The Travel Leadership Forum: Evolution of Online Travel 2008Document6 pagesEyeforTravel - The Travel Leadership Forum: Evolution of Online Travel 2008Nikhil VijayanNo ratings yet

- STOCK AUDIT PROCEDURES AND IRREGULARITIESDocument4 pagesSTOCK AUDIT PROCEDURES AND IRREGULARITIESCma Suman Kumar VermaNo ratings yet

- Ejaz Naseer NBP Reprort 2018Document58 pagesEjaz Naseer NBP Reprort 2018Tayyab ali gardaziNo ratings yet