You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- AprilDocument6 pagesAprilcindy pecañaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Qantas Airways: Name: Institution Affiliation: DateDocument8 pagesQantas Airways: Name: Institution Affiliation: DatePhuong NhungNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Doing Business in The UkDocument20 pagesDoing Business in The UkMalena BerardiNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Item Description RCVD Unit Price Gross Amt Disc % Ta Amount DeptDocument1 pageItem Description RCVD Unit Price Gross Amt Disc % Ta Amount DeptGustu LiranNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Chapter 5 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Document33 pagesChapter 5 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Falah Ud Din SheryarNo ratings yet

- April 2023 The Bill ElectricityDocument1 pageApril 2023 The Bill ElectricityAbdul Raheem OfficialNo ratings yet

- Account Activity: Mar 18-Apr 19, 2011Document3 pagesAccount Activity: Mar 18-Apr 19, 2011Yusuf OmarNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Service Charges and FeesDocument11 pagesService Charges and FeesajmalNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- HDFC Bank Deposit Online Receipt FormatDocument1 pageHDFC Bank Deposit Online Receipt FormatAjay Ajay67% (6)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Prelim Exam-Business Tax - Set BDocument3 pagesPrelim Exam-Business Tax - Set BRenalyn Paras0% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Tax Invoice: Description of Goods Amount Per Rate Quantity Hsn/SacDocument2 pagesTax Invoice: Description of Goods Amount Per Rate Quantity Hsn/SacBhavnaben PanchalNo ratings yet

- Inv-0058 Ayyappa AgenciesDocument1 pageInv-0058 Ayyappa AgenciesSRIKAR DHANOORINo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- ACC 111 Chapter 7 Lecture NotesDocument5 pagesACC 111 Chapter 7 Lecture NotesLoriNo ratings yet

- Quiz Chapter 2 Statement of Comprehensive IncomeDocument13 pagesQuiz Chapter 2 Statement of Comprehensive Incomefinn mertensNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Dinner For Kirsten GillibrandDocument2 pagesDinner For Kirsten GillibrandSunlight FoundationNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

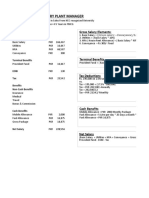

- Shoe Factory Plant Manager: Gross Salary ElementsDocument2 pagesShoe Factory Plant Manager: Gross Salary ElementsSukaina SalmanNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Online Shoppers 30 Lack DataDocument18 pagesOnline Shoppers 30 Lack DataSuvojit MondalNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Electricity Tax Interest Payment Electricity Tax Interest Payment Electricity Tax Interest PaymentDocument1 pageElectricity Tax Interest Payment Electricity Tax Interest Payment Electricity Tax Interest PaymentaaanathanNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- 02 PDF MergedDocument36 pages02 PDF MergedarpanNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- PR 7 Diagnostic ExamDocument8 pagesPR 7 Diagnostic ExamMendoza Ron NixonNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Printable Receipt Pizza DeliveryDocument1 pagePrintable Receipt Pizza DeliveryNestor FloresNo ratings yet

- Series 7 Watch BillDocument1 pageSeries 7 Watch BillVedans FinancesNo ratings yet

- GrubhubDocument3 pagesGrubhubBig TeenzNo ratings yet

- Welcome To HDFC Bank NetBankingDocument2 pagesWelcome To HDFC Bank NetBankingGAURAV MISHRANo ratings yet

- Surya YasaDocument2 pagesSurya YasaAh MuhayNo ratings yet

- The Trial Balance of Steve Mentz Cpa Is Dated March PDFDocument1 pageThe Trial Balance of Steve Mentz Cpa Is Dated March PDFAhsan KhanNo ratings yet

- Hotel Confirmation TemplateDocument2 pagesHotel Confirmation TemplateantonytechnoNo ratings yet

- CIR v. PAL (Ortega)Document5 pagesCIR v. PAL (Ortega)Peter Joshua OrtegaNo ratings yet

- Retained EarningsDocument7 pagesRetained EarningsSelena SevvinNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Income and Business TaxationDocument24 pagesIncome and Business TaxationFerdinand Carlos B. DadoNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)