You might also like

- Economic Development in The Philippines: High Potential, Big Challenges, Wide ImpactDocument31 pagesEconomic Development in The Philippines: High Potential, Big Challenges, Wide ImpactArangkada PhilippinesNo ratings yet

- UNDESA E-Gouvernement, Étude Complète 2014Document284 pagesUNDESA E-Gouvernement, Étude Complète 2014usinemarocNo ratings yet

- UNDESA E-Gouvernement, Étude Complète 2014Document284 pagesUNDESA E-Gouvernement, Étude Complète 2014usinemarocNo ratings yet

- REFMAD-V Enterprise Ilocos NorteDocument11 pagesREFMAD-V Enterprise Ilocos NorteArangkada PhilippinesNo ratings yet

- Deloitte Philippines Competitiveness ReportDocument15 pagesDeloitte Philippines Competitiveness ReportArangkada PhilippinesNo ratings yet

- 2014 February NewsletterDocument2 pages2014 February NewsletterArangkada PhilippinesNo ratings yet

- Palafox Masterplan Ilocos NorteDocument33 pagesPalafox Masterplan Ilocos NorteArangkada Philippines100% (3)

- Overseas Filipino Remittance Ilocos NorteDocument7 pagesOverseas Filipino Remittance Ilocos NorteArangkada PhilippinesNo ratings yet

- Medical Tourism Ilocos NorteDocument34 pagesMedical Tourism Ilocos NorteArangkada PhilippinesNo ratings yet

- FCC Presentation FinalDocument27 pagesFCC Presentation FinalArangkada PhilippinesNo ratings yet

- BPO-ICT Potentials Ilocos NorteDocument20 pagesBPO-ICT Potentials Ilocos NorteArangkada PhilippinesNo ratings yet

- 2014 March NewsletterDocument2 pages2014 March NewsletterArangkada PhilippinesNo ratings yet

- April TPP Updates EmailDocument4 pagesApril TPP Updates EmailArangkada PhilippinesNo ratings yet

- Sponsorship SpeechesDocument31 pagesSponsorship SpeechesArangkada PhilippinesNo ratings yet

- Amcham Statement Regarding Obama's VisitDocument1 pageAmcham Statement Regarding Obama's VisitArangkada PhilippinesNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- MAIZEDocument27 pagesMAIZEDr Annie SheronNo ratings yet

- Human Rights Law - Yasin vs. Hon. Judge Sharia CourtDocument7 pagesHuman Rights Law - Yasin vs. Hon. Judge Sharia CourtElixirLanganlanganNo ratings yet

- Erich FrommDocument2 pagesErich FrommTina NavarroNo ratings yet

- Global Warmin G and Green House Effect: Submit Ted To:-Mr - Kaush Ik SirDocument24 pagesGlobal Warmin G and Green House Effect: Submit Ted To:-Mr - Kaush Ik SirinderpreetNo ratings yet

- PD 984Document38 pagesPD 984mav3riick100% (2)

- Kern County Sues Governor Gavin NewsomDocument3 pagesKern County Sues Governor Gavin NewsomAnthony Wright100% (1)

- Rahu Yantra Kal Sarp Yantra: Our RecommendationsDocument2 pagesRahu Yantra Kal Sarp Yantra: Our RecommendationsAbhijeet DeshmukkhNo ratings yet

- 10.0 Ms For Scaffolding WorksDocument7 pages10.0 Ms For Scaffolding WorksilliasuddinNo ratings yet

- Assignment Nutrition and HydrationDocument17 pagesAssignment Nutrition and Hydrationmelencio olivasNo ratings yet

- B65a RRH2x40-4R UHGC SPDocument71 pagesB65a RRH2x40-4R UHGC SPNicolás RuedaNo ratings yet

- Manual Chiller Parafuso DaikinDocument76 pagesManual Chiller Parafuso Daiking3qwsf100% (1)

- Biomolecules ExtractionDocument6 pagesBiomolecules ExtractionBOR KIPLANGAT ISAACNo ratings yet

- Presentation - Factors Affecting ClimateDocument16 pagesPresentation - Factors Affecting ClimateAltoverosDihsarlaNo ratings yet

- Moderated Caucus Speech Samples For MUNDocument2 pagesModerated Caucus Speech Samples For MUNihabNo ratings yet

- Pet 402Document1 pagePet 402quoctuanNo ratings yet

- Generic 5S ChecklistDocument2 pagesGeneric 5S Checklistswamireddy100% (1)

- Toaz - Info Fermentation of Carrot Juice Wheat Flour Gram Flour Etc PRDocument17 pagesToaz - Info Fermentation of Carrot Juice Wheat Flour Gram Flour Etc PRBhumika SahuNo ratings yet

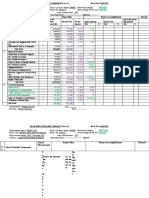

- Fomula Spreadsheet (WACC and NPV)Document7 pagesFomula Spreadsheet (WACC and NPV)vaishusonu90No ratings yet

- Test Questions For Oncologic DisordersDocument6 pagesTest Questions For Oncologic Disorderspatzie100% (1)

- Sindh Rescue 1122 Test Sample PapersDocument12 pagesSindh Rescue 1122 Test Sample PapersMAANJONY100% (1)

- Site Quality ManualDocument376 pagesSite Quality ManualsNo ratings yet

- Wa0016Document3 pagesWa0016Vinay DahiyaNo ratings yet

- Quarterly Progress Report FormatDocument7 pagesQuarterly Progress Report FormatDegnesh AssefaNo ratings yet

- Multilevel Full Mock Test 5: Telegramdagi KanalDocument20 pagesMultilevel Full Mock Test 5: Telegramdagi KanalShaxzod AxmadjonovNo ratings yet

- Aircaft Avionics SystemDocument21 pagesAircaft Avionics SystemPavan KumarNo ratings yet

- Hippocrates OathDocument6 pagesHippocrates OathSundary FlhorenzaNo ratings yet

- Full Bridge Phase Shift ConverterDocument21 pagesFull Bridge Phase Shift ConverterMukul ChoudhuryNo ratings yet

- The Power of PositivityDocument5 pagesThe Power of PositivityYorlenis PintoNo ratings yet

- Rar Vol11 Nro3Document21 pagesRar Vol11 Nro3Valentine WijayaNo ratings yet

- Sports MedicineDocument2 pagesSports MedicineShelby HooklynNo ratings yet