You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Shed PlansDocument1 pageShed PlansFrancis Wolfgang UrbanNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Figure E Small Roof: 2x4 Nailers 2x4 Rafter 2x4 Subfascia 1x2 Fascia Trim 24" 32" 29-3/4"Document1 pageFigure E Small Roof: 2x4 Nailers 2x4 Rafter 2x4 Subfascia 1x2 Fascia Trim 24" 32" 29-3/4"Francis Wolfgang UrbanNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Shed Material List Part (1 of 9)Document2 pagesShed Material List Part (1 of 9)nwright_besterNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shed PlansDocument1 pageShed PlansFrancis Wolfgang Urban50% (2)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shed PlansDocument1 pageShed PlansFrancis Wolfgang UrbanNo ratings yet

- Figure A Trusses: Inner (Common) Truss (9 Req'd)Document1 pageFigure A Trusses: Inner (Common) Truss (9 Req'd)Francis Wolfgang UrbanNo ratings yet

- Shed PlansDocument1 pageShed PlansFrancis Wolfgang UrbanNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- 25 Foot CabinDocument28 pages25 Foot Cabinapi-3708365100% (1)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shed PlansDocument16 pagesShed PlansFrancis Wolfgang Urban100% (7)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Shed PlansDocument1 pageShed PlansFrancis Wolfgang UrbanNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- 10 Dollar Telescope PlansDocument9 pages10 Dollar Telescope Planssandhi88No ratings yet

- 15 Foot SailDocument4 pages15 Foot SailjdogheadNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- IRS Publication Form Instructions 1099 MiscDocument10 pagesIRS Publication Form Instructions 1099 MiscFrancis Wolfgang UrbanNo ratings yet

- IRS Publication Form Instructions 8853Document8 pagesIRS Publication Form Instructions 8853Francis Wolfgang UrbanNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- 6 Inch Reflector PlansDocument12 pages6 Inch Reflector PlansSektordrNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- 3 Wheel 2Document5 pages3 Wheel 2jii_907001No ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- 3inchrefractorDocument6 pages3inchrefractorGianluca SalvatoNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- IRS Publication Form Instructions 2106Document8 pagesIRS Publication Form Instructions 2106Francis Wolfgang UrbanNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- IRS Publication Form 8919Document2 pagesIRS Publication Form 8919Francis Wolfgang UrbanNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Human Resources HR Consultant AgreementDocument7 pagesHuman Resources HR Consultant Agreementwaqastariq77_7812164100% (1)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Chapter 6Document29 pagesChapter 6Reese Parker20% (5)

- App IDocument13 pagesApp I김민성No ratings yet

- HR MR2 Requirements Document: Draft Copy For Initial ReviewDocument22 pagesHR MR2 Requirements Document: Draft Copy For Initial ReviewĶåřìimó ÅbďīNo ratings yet

- Waiver of Interest FormsDocument9 pagesWaiver of Interest FormsJordan MillerNo ratings yet

- Current Liabilities, Provisions, and Contingencies: Chapter Learning ObjectivesDocument43 pagesCurrent Liabilities, Provisions, and Contingencies: Chapter Learning Objectivesannedanyle acabadoNo ratings yet

- Chapter 1 Individual Income TaxDocument21 pagesChapter 1 Individual Income TaxtravellingNo ratings yet

- Cpar-Chapter 13: Current Liabilities and ContingenciesDocument37 pagesCpar-Chapter 13: Current Liabilities and Contingenciesspur ious100% (1)

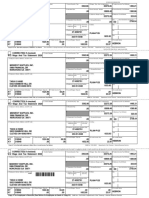

- Second PaystubDocument1 pageSecond Paystubjohnathan greyNo ratings yet

- W2 & Earnings: Emma MimsDocument1 pageW2 & Earnings: Emma MimsIsaiah MimsNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Uber SettlementDocument153 pagesUber Settlementjeff_roberts881No ratings yet

- Exercises Chapter 11Document3 pagesExercises Chapter 11Fatima BeenaNo ratings yet

- Copy B-To Be Filed With Employee's FEDERAL Tax ReturnDocument5 pagesCopy B-To Be Filed With Employee's FEDERAL Tax ReturnKyle im taken by cailey hand Hand100% (1)

- CH 8Document36 pagesCH 8anjo hosmerNo ratings yet

- The Following Payroll Liability Accounts Are Included in The Ledger 118383Document1 pageThe Following Payroll Liability Accounts Are Included in The Ledger 118383M Bilal SaleemNo ratings yet

- Wage and Tax Statement: Copy B - To Be Filed With Employee's FEDERAL Tax ReturnDocument7 pagesWage and Tax Statement: Copy B - To Be Filed With Employee's FEDERAL Tax ReturnLovely HeartNo ratings yet

- What Is A Corporation SoleDocument30 pagesWhat Is A Corporation Solelihu74100% (2)

- StatementDocument1 pageStatementWaifubot 2.1No ratings yet

- PWC Tax GuideDocument30 pagesPWC Tax Guideshikhagupta3288No ratings yet

- Military Members: 2LT Entitlements Packet 2011Document38 pagesMilitary Members: 2LT Entitlements Packet 2011saltonc7No ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Paying Taxes With Coupon 112903Document4 pagesPaying Taxes With Coupon 112903Ya Boy React100% (5)

- 2018 Instructions For Schedule 8812: Additional Child Tax CreditDocument3 pages2018 Instructions For Schedule 8812: Additional Child Tax CredittinpenaNo ratings yet

- Wage and Tax Statement: OMB No. 1545-0008Document7 pagesWage and Tax Statement: OMB No. 1545-0008LUZILLE MEDINANo ratings yet

- Instructions:: Apollo Preliminary Analytical Procedures Audit Mini-CaseDocument14 pagesInstructions:: Apollo Preliminary Analytical Procedures Audit Mini-CaseShefali GoyalNo ratings yet

- Income Tax Return 2019Document9 pagesIncome Tax Return 2019Sh'Nanigns X3No ratings yet

- July PAY STUB 03Document1 pageJuly PAY STUB 03enudo SolomonNo ratings yet

- Chapter 9 - Solution Manual PDFDocument37 pagesChapter 9 - Solution Manual PDFNatalie ChoiNo ratings yet

- 5 Audit Procedures ChecklistsDocument43 pages5 Audit Procedures ChecklistsCahya PerdanaNo ratings yet

- Kelompok 10 - Kelas o - Week 9Document10 pagesKelompok 10 - Kelas o - Week 9willyNo ratings yet

- Nanny Work Agreement For Criselle M MarquezDocument6 pagesNanny Work Agreement For Criselle M MarquezZhel MarquezNo ratings yet