You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Praxis Business School: Assignment OnDocument26 pagesPraxis Business School: Assignment OnArihantNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Introduction To PM - Session 1Document9 pagesIntroduction To PM - Session 1Sushma Jeswani TalrejaNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- 5 Porters Model of Coca ColaDocument10 pages5 Porters Model of Coca ColaIshaan TalrejaNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Coca Cola PPT of 5 Porters ModelDocument14 pagesCoca Cola PPT of 5 Porters ModelIshaan TalrejaNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Organization Unit IDocument42 pagesOrganization Unit IIshaan TalrejaNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- CaseDocument3 pagesCaseIshaan TalrejaNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- XXX ReportDocument73 pagesXXX ReportIshaan TalrejaNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Product Pricing Session 4Document24 pagesProduct Pricing Session 4Ishaan TalrejaNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Observation MethodDocument1 pageObservation MethodIshaan TalrejaNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- Porters Five Force ModelDocument6 pagesPorters Five Force ModelIshaan TalrejaNo ratings yet

- Prescriptive Strategy To Rescue BritainDocument1 pagePrescriptive Strategy To Rescue BritainIshaan TalrejaNo ratings yet

- Indian Telecom SectorDocument18 pagesIndian Telecom SectorIshaan TalrejaNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Prescriptive Strategy To Rescue BritainDocument1 pagePrescriptive Strategy To Rescue BritainIshaan TalrejaNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Mcdonald'sDocument3 pagesMcdonald'sIshaan TalrejaNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Telecom CaseStudy Telenor Streamlines HR Management System 07 2011Document4 pagesTelecom CaseStudy Telenor Streamlines HR Management System 07 2011Adil MustafaNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Observation MethodDocument1 pageObservation MethodIshaan TalrejaNo ratings yet

- Boston Consulting GroupDocument3 pagesBoston Consulting GroupPuran SinghNo ratings yet

- Admissions and Discharge: GuidelinesDocument26 pagesAdmissions and Discharge: GuidelinesIshaan TalrejaNo ratings yet

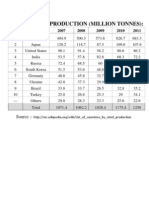

- Top Steel Producing Countries 2007-2011Document1 pageTop Steel Producing Countries 2007-2011Ishaan TalrejaNo ratings yet

- Everything You Need to Know About Bluetooth TechnologyDocument21 pagesEverything You Need to Know About Bluetooth TechnologyNav89No ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Thokth Fo'ofo - Ky ) Xokfy J: at @ Vf/klwpuk at @Document11 pagesThokth Fo'ofo - Ky ) Xokfy J: at @ Vf/klwpuk at @Ishaan TalrejaNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- RRB Sample Qs PaperDocument1 pageRRB Sample Qs PaperIshaan TalrejaNo ratings yet

- Time TableDocument2 pagesTime TableIshaan TalrejaNo ratings yet

- Bba Time TableDocument1 pageBba Time TableIshaan TalrejaNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Paper 5 PDFDocument529 pagesPaper 5 PDFTeddy BearNo ratings yet

- Model LOC Model LOC: CeltronDocument3 pagesModel LOC Model LOC: CeltronmhemaraNo ratings yet

- Appointment and Authority of AgentsDocument18 pagesAppointment and Authority of AgentsRaghav Randar0% (1)

- Kotler & Keller (Pp. 325-349)Document3 pagesKotler & Keller (Pp. 325-349)Lucía ZanabriaNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Parked Tank LayoutDocument1 pageParked Tank LayoutAZreen A. ZAwawiNo ratings yet

- Application of Game TheoryDocument65 pagesApplication of Game Theorymithunsraj@gmail.com100% (2)

- Bharathiar University MPhil/PhD Management SyllabusDocument22 pagesBharathiar University MPhil/PhD Management SyllabusRisker RaviNo ratings yet

- 911 AuditDocument163 pages911 AuditAlyssa RobertsNo ratings yet

- Steelpipe Sales Catalogue 4th Edition May 12Document61 pagesSteelpipe Sales Catalogue 4th Edition May 12jerome42nNo ratings yet

- Chapter 4 - Fire InsuranceDocument8 pagesChapter 4 - Fire InsuranceKhandoker Mahmudul HasanNo ratings yet

- CE462-CE562 Principles of Health and Safety-Birleştirildi PDFDocument663 pagesCE462-CE562 Principles of Health and Safety-Birleştirildi PDFAnonymous MnNFIYB2No ratings yet

- EMPLOYEE PARTICIPATION: A STRATEGIC PROCESS FOR TURNAROUND - K. K. VermaDocument17 pagesEMPLOYEE PARTICIPATION: A STRATEGIC PROCESS FOR TURNAROUND - K. K. VermaRaktim PaulNo ratings yet

- Umjetnost PDFDocument92 pagesUmjetnost PDFJuanRodriguezNo ratings yet

- Ch03 - The Environments of Marketing ChannelsDocument25 pagesCh03 - The Environments of Marketing ChannelsRaja Muaz67% (3)

- The Cochran Firm Fraud Failed in CA Fed. CourtDocument13 pagesThe Cochran Firm Fraud Failed in CA Fed. CourtMary NealNo ratings yet

- Consumer Buying Behaviour - FEVICOLDocument10 pagesConsumer Buying Behaviour - FEVICOLShashank Joshi100% (1)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- LGEIL competitive advantagesDocument3 pagesLGEIL competitive advantagesYash RoxsNo ratings yet

- TCS Connected Universe Platform - 060918Document4 pagesTCS Connected Universe Platform - 060918abhishek tripathyNo ratings yet

- APSS1B17 - Contemporary Chinese Society and Popcult - L2 (Week 3)Document28 pagesAPSS1B17 - Contemporary Chinese Society and Popcult - L2 (Week 3)Arvic LauNo ratings yet

- Sap CloudDocument29 pagesSap CloudjagankilariNo ratings yet

- Dynamic Cables Pvt. LTD.: WORKS ORDER-Conductor DivDocument2 pagesDynamic Cables Pvt. LTD.: WORKS ORDER-Conductor DivMLastTryNo ratings yet

- International Trade Statistics YearbookDocument438 pagesInternational Trade Statistics YearbookJHON ALEXIS VALENCIA MENESESNo ratings yet

- PEA144Document4 pagesPEA144coffeepathNo ratings yet

- Customer Satisfaction Report on Peaks AutomobilesDocument72 pagesCustomer Satisfaction Report on Peaks AutomobilesHarmeet SinghNo ratings yet

- CRMDocument7 pagesCRMDushyant PandaNo ratings yet

- Mem 720 - QBDocument10 pagesMem 720 - QBJSW ENERGYNo ratings yet

- Scd Hw2 Nguyễn Thị Hoài Liên Ielsiu19038Document4 pagesScd Hw2 Nguyễn Thị Hoài Liên Ielsiu19038Liên Nguyễn Thị HoàiNo ratings yet

- Multiple Choice QuestionsDocument9 pagesMultiple Choice QuestionsReymark MutiaNo ratings yet

- Bid Doc ZESCO06614 Mumbwa Sanje Reinforcement July 2014 FinalDocument374 pagesBid Doc ZESCO06614 Mumbwa Sanje Reinforcement July 2014 FinalmatshonaNo ratings yet

- The Role of Business ResearchDocument23 pagesThe Role of Business ResearchWaqas Ali BabarNo ratings yet

- Summary: Atomic Habits by James Clear: An Easy & Proven Way to Build Good Habits & Break Bad OnesFrom EverandSummary: Atomic Habits by James Clear: An Easy & Proven Way to Build Good Habits & Break Bad OnesRating: 5 out of 5 stars5/5 (1631)

- Mindset by Carol S. Dweck - Book Summary: The New Psychology of SuccessFrom EverandMindset by Carol S. Dweck - Book Summary: The New Psychology of SuccessRating: 4.5 out of 5 stars4.5/5 (327)

- The War of Art by Steven Pressfield - Book Summary: Break Through The Blocks And Win Your Inner Creative BattlesFrom EverandThe War of Art by Steven Pressfield - Book Summary: Break Through The Blocks And Win Your Inner Creative BattlesRating: 4.5 out of 5 stars4.5/5 (273)

- The Compound Effect by Darren Hardy - Book Summary: Jumpstart Your Income, Your Life, Your SuccessFrom EverandThe Compound Effect by Darren Hardy - Book Summary: Jumpstart Your Income, Your Life, Your SuccessRating: 5 out of 5 stars5/5 (456)

- SUMMARY: So Good They Can't Ignore You (UNOFFICIAL SUMMARY: Lesson from Cal Newport)From EverandSUMMARY: So Good They Can't Ignore You (UNOFFICIAL SUMMARY: Lesson from Cal Newport)Rating: 4.5 out of 5 stars4.5/5 (14)