You might also like

- Post Implementation Review of Project CompletionDocument19 pagesPost Implementation Review of Project CompletionAmul Shrestha50% (2)

- Module 3 BudgetDocument22 pagesModule 3 BudgetLeizeljoy B. BALDERASNo ratings yet

- PP-20-Governance GuideDocument17 pagesPP-20-Governance GuideSALAH HELLARANo ratings yet

- ScbaDocument15 pagesScbaAmit SinghNo ratings yet

- Introduction To Public Sector Finance IIDocument28 pagesIntroduction To Public Sector Finance IIPEDRONo ratings yet

- Planning Programming Budgeting System (PPBS)Document16 pagesPlanning Programming Budgeting System (PPBS)Central University100% (1)

- Bpa122 Module5Document9 pagesBpa122 Module5Asnairah DICUNUGUNNo ratings yet

- 1.) Assessing The Soundness of The BudgetDocument22 pages1.) Assessing The Soundness of The BudgetTesh SiNo ratings yet

- Public Financial Management in GhanaDocument6 pagesPublic Financial Management in GhanaKwaku- Tei100% (2)

- Lessons Learned: Improving Resumes with the STAR TechniqueDocument26 pagesLessons Learned: Improving Resumes with the STAR TechniqueSmriti KambojNo ratings yet

- Chapter Three:: Project Resource ManagementDocument26 pagesChapter Three:: Project Resource ManagementKhalid Abdiaziz AbdulleNo ratings yet

- C 25 11 Cost EffectivenessDocument11 pagesC 25 11 Cost EffectivenessaptureincNo ratings yet

- Template For Terms of Reference For Project and Programme EvaluationsDocument8 pagesTemplate For Terms of Reference For Project and Programme EvaluationsAmr FangaryNo ratings yet

- Government BudgetingDocument23 pagesGovernment BudgetingChristopher John MwakipesileNo ratings yet

- PublicInvestmentEfficiency KOREADocument24 pagesPublicInvestmentEfficiency KOREAJuKannNo ratings yet

- Earned Value ManagementDocument17 pagesEarned Value ManagementwaterNo ratings yet

- Project Cost Management GuideDocument17 pagesProject Cost Management GuideBirhanu AtnafuNo ratings yet

- VFM Systems Matrix PrefinDocument28 pagesVFM Systems Matrix Prefinkaramat12No ratings yet

- Project Budgeting FundamentalsDocument8 pagesProject Budgeting Fundamentalsمعتز محمدNo ratings yet

- Strategic Planning Process and AnalysisDocument28 pagesStrategic Planning Process and AnalysisSachin MishraNo ratings yet

- Nursing Budget: According To TN Chhabra A Budget Is An Estimation of Future Needs Arranged According To Orderly BasisDocument7 pagesNursing Budget: According To TN Chhabra A Budget Is An Estimation of Future Needs Arranged According To Orderly BasisPooja VishwakarmaNo ratings yet

- Administrative Skills: Budgets in A Business Environment: ITLA 023Document22 pagesAdministrative Skills: Budgets in A Business Environment: ITLA 023TAN XIEW LINGNo ratings yet

- Project Cost ManagementDocument14 pagesProject Cost ManagementRishabhGuptaNo ratings yet

- MonitoringDocument7 pagesMonitoringKylie Mae Ladignon CorpuzNo ratings yet

- Hole OF Roject Valuation: Rogram YcleDocument8 pagesHole OF Roject Valuation: Rogram Yclemerlyk2360No ratings yet

- Project Budgeting GuideDocument31 pagesProject Budgeting GuideAbdisamed AllaaleNo ratings yet

- Week 2 OpmanDocument4 pagesWeek 2 OpmanChristine GarciaNo ratings yet

- Eplc Project Management Plan Practices GuideDocument3 pagesEplc Project Management Plan Practices GuiderezareaNo ratings yet

- How To Initiate A Performance Framework in BudgetingDocument24 pagesHow To Initiate A Performance Framework in BudgetingInternational Consortium on Governmental Financial ManagementNo ratings yet

- Motivation, Budgets and Responsibility AccountingDocument5 pagesMotivation, Budgets and Responsibility AccountingDesak Putu Kenanga PutriNo ratings yet

- Budget Preparation NotesDocument4 pagesBudget Preparation NotesInnocent MapaNo ratings yet

- Operations Management: Session 11, 12 & 13 23/02/24, 26/02/24, 28/02/24 DR Monika TanwarDocument76 pagesOperations Management: Session 11, 12 & 13 23/02/24, 26/02/24, 28/02/24 DR Monika Tanwarm23msa109No ratings yet

- PAN African E-Network Project: Project Planning: Appraisal and ControlDocument76 pagesPAN African E-Network Project: Project Planning: Appraisal and ControlEng Abdulkadir MahamedNo ratings yet

- Resource AllocationDocument8 pagesResource AllocationjbahalkehNo ratings yet

- The Strategic Planning Process: A. Questions and ActivitiesDocument4 pagesThe Strategic Planning Process: A. Questions and ActivitiesDennis ValdezNo ratings yet

- BudgetingDocument45 pagesBudgetingAbdul KadharNo ratings yet

- Linking Project Design, Annual Planning and M&E: SectionDocument32 pagesLinking Project Design, Annual Planning and M&E: SectionbqdianzNo ratings yet

- Business Studies AS Unit 2 Section 3 Topic 1: BudgetsDocument13 pagesBusiness Studies AS Unit 2 Section 3 Topic 1: BudgetsAzoraNo ratings yet

- Chapter 3 Financial FplanningDocument22 pagesChapter 3 Financial Fplanningwax barasho2021No ratings yet

- Government Budgeting Principles, Approaches and Philippine ProcessDocument10 pagesGovernment Budgeting Principles, Approaches and Philippine ProcessAngel BNo ratings yet

- BudgetingDocument46 pagesBudgetingenas.aborayaNo ratings yet

- FM8PBBDocument95 pagesFM8PBBsamuel hailuNo ratings yet

- ASSIGNMENT On Cost EstimationDocument15 pagesASSIGNMENT On Cost EstimationAbhisek Sarkar67% (3)

- PROJECT REPORTS - Closure ReportsDocument5 pagesPROJECT REPORTS - Closure ReportsAnkapali MukherjeeNo ratings yet

- Tools and Techniques of Capital Expenditure ControlDocument11 pagesTools and Techniques of Capital Expenditure ControlHari PurwadiNo ratings yet

- Bsbpmg514 TestDocument5 pagesBsbpmg514 Testsita maharjanNo ratings yet

- Fundamentals of Education ProjectsDocument9 pagesFundamentals of Education ProjectsTabeeta NoreenNo ratings yet

- Chapter Two IPSAS Slide 1 ok-1Document93 pagesChapter Two IPSAS Slide 1 ok-1haymanot gizachewNo ratings yet

- Cost ManagementDocument27 pagesCost ManagementSalman EjazNo ratings yet

- ZZB in PlanningDocument15 pagesZZB in PlanningkarstacyNo ratings yet

- Management ConceptDocument11 pagesManagement ConceptRishabh PathakNo ratings yet

- Presentation 1Document46 pagesPresentation 1ramptechNo ratings yet

- (Project Management Institute) Project Management (B-Ok - Xyz)Document19 pages(Project Management Institute) Project Management (B-Ok - Xyz)Hayelom Tadesse GebreNo ratings yet

- A452 Chester Road Improvements Post Implementation Review ProposalDocument10 pagesA452 Chester Road Improvements Post Implementation Review Proposalkasiopeia30No ratings yet

- Project Cost ManagementDocument30 pagesProject Cost ManagementBUKENYA BEEE-2026No ratings yet

- Budgeting in A Public Sector Power PointDocument40 pagesBudgeting in A Public Sector Power PointSamuel DwumfourNo ratings yet

- Unit 4 4.3 Investment Decisions Profile of The ProjectDocument19 pagesUnit 4 4.3 Investment Decisions Profile of The ProjectAntony antonyNo ratings yet

- Zero Base Budgeting A and Performance Budgeting 090823145427 Phpapp01Document9 pagesZero Base Budgeting A and Performance Budgeting 090823145427 Phpapp01natrix029No ratings yet

- TOGAF® 10 Level 2 Enterprise Arch Part 2 Exam Wonder Guide Volume 2: TOGAF 10 Level 2 Scenario Strategies, #2From EverandTOGAF® 10 Level 2 Enterprise Arch Part 2 Exam Wonder Guide Volume 2: TOGAF 10 Level 2 Scenario Strategies, #2Rating: 5 out of 5 stars5/5 (1)

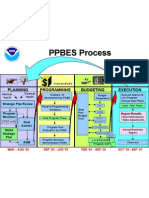

- Ppbes OverviewDocument1 pagePpbes OverviewOctavian VaduvaNo ratings yet

- Improving The Execution of StrategyDocument12 pagesImproving The Execution of StrategyOctavian VaduvaNo ratings yet

- Do DArmy PPBEPrimer 17 Sept 2010Document24 pagesDo DArmy PPBEPrimer 17 Sept 2010Octavian VaduvaNo ratings yet

- PLANNING, PROGRAMMING, BUDGETING, AND EXECUTION (PPBE) PROCESS OVERVIEWDocument21 pagesPLANNING, PROGRAMMING, BUDGETING, AND EXECUTION (PPBE) PROCESS OVERVIEWOctavian VaduvaNo ratings yet

- PPBE PresentationDocument11 pagesPPBE PresentationOctavian VaduvaNo ratings yet

- Understanding Culture, Society and PoliticsDocument14 pagesUnderstanding Culture, Society and PoliticsBalino, Harold Vincent A.No ratings yet

- Information Technology Certified ProfessionalDocument14 pagesInformation Technology Certified ProfessionalkhaledabdulahNo ratings yet

- Organizational Culture, Socialization, and Mentoring: Mcgraw-Hill/IrwinDocument48 pagesOrganizational Culture, Socialization, and Mentoring: Mcgraw-Hill/IrwinAmanda MeisaNo ratings yet

- Management ToolsDocument120 pagesManagement ToolsBalakumar VNo ratings yet

- Selling The WheelDocument3 pagesSelling The WheelYeasir MalikNo ratings yet

- Relationship Between Corporate Identity and Corporate Reputation: A Case of A Malaysian Higher Education SectorDocument9 pagesRelationship Between Corporate Identity and Corporate Reputation: A Case of A Malaysian Higher Education SectorGandar KusumaNo ratings yet

- A Comparative Study On The Socio Cultura PDFDocument25 pagesA Comparative Study On The Socio Cultura PDFvanessa viojanNo ratings yet

- PWC M&A Integration Survey Report 2017Document30 pagesPWC M&A Integration Survey Report 2017ShuNo ratings yet

- A S WatsonDocument13 pagesA S WatsonDENNIS KIHUNGINo ratings yet

- Introduction of Management LeadershipDocument130 pagesIntroduction of Management LeadershipprashantNo ratings yet

- MGTO 324 Recruitment and Selections: Staffing Model, Strategy, & PlanningDocument39 pagesMGTO 324 Recruitment and Selections: Staffing Model, Strategy, & PlanningKRITIKA NIGAMNo ratings yet

- Operation Management - Case Study 7-2Document2 pagesOperation Management - Case Study 7-2chifai33150% (2)

- School Effectiveness & School-Based ManagementDocument71 pagesSchool Effectiveness & School-Based Managementhartinihusain100% (3)

- NYCDCC Report 07 ECFNo.1755 FourthInterimReportoftheIndependentMon...Document24 pagesNYCDCC Report 07 ECFNo.1755 FourthInterimReportoftheIndependentMon...Latisha Walker0% (1)

- WASSCE WAEC Social Studies Syllabus PDFDocument10 pagesWASSCE WAEC Social Studies Syllabus PDFdaasebre ababiomNo ratings yet

- The Intelligent Internationall NegotiatorDocument174 pagesThe Intelligent Internationall NegotiatorKulbir SinghNo ratings yet

- Digital Tech Leadership Program (DTLP) Summer 2020Document2 pagesDigital Tech Leadership Program (DTLP) Summer 2020Lizzy McquireNo ratings yet

- Contingency ModelsDocument60 pagesContingency Modelskay enNo ratings yet

- Individual Assignment MA RevisedDocument11 pagesIndividual Assignment MA RevisedKamaruzzaman Kamaludeen50% (2)

- The Indian Institute of Business Management & Studies: CASE NO - 1 - Health or WorkDocument3 pagesThe Indian Institute of Business Management & Studies: CASE NO - 1 - Health or Workchu39548No ratings yet

- Topic 4 Culture and LeadershipDocument24 pagesTopic 4 Culture and LeadershipCARLVETT ELLENNE JUNNENo ratings yet

- Doctrine Update For AFDD 1-1Document2 pagesDoctrine Update For AFDD 1-1Joel BurtonNo ratings yet

- Organizational Behaviour Syllabus PDFDocument6 pagesOrganizational Behaviour Syllabus PDFAmorsolo EspirituNo ratings yet

- Diversity Wins: How Inclusion MattersDocument56 pagesDiversity Wins: How Inclusion MattersdgNo ratings yet

- Guidance For AY17 Command and General Staff Officer Course (CGSOC)Document19 pagesGuidance For AY17 Command and General Staff Officer Course (CGSOC)Foreign PolicyNo ratings yet

- 5 Lb. Book of GRE Practice Problems (2nd Edition - Latest)Document191 pages5 Lb. Book of GRE Practice Problems (2nd Edition - Latest)MRAAKNo ratings yet

- Coo Perform AppraisalDocument7 pagesCoo Perform AppraisalAninditya Hasna KurniatiNo ratings yet

- Essential Qualities of A LeaderDocument4 pagesEssential Qualities of A LeaderShafiq MirdhaNo ratings yet

- AME Lean AssessmentDocument33 pagesAME Lean AssessmentYenaro CortesNo ratings yet

- SMRP GUIDELINE 3.0 Determining Leading and Lagging IndicatorsDocument6 pagesSMRP GUIDELINE 3.0 Determining Leading and Lagging IndicatorsJair TNo ratings yet