You might also like

- Wind Energy Sarvesh - KumarDocument26 pagesWind Energy Sarvesh - Kumaranon_228506499No ratings yet

- Workshop On Combined Heat & PowerDocument25 pagesWorkshop On Combined Heat & PowerRajat SudNo ratings yet

- Business opportunities in electric motor industryDocument12 pagesBusiness opportunities in electric motor industryOsen GaoNo ratings yet

- Power Scenario IN India: A.S.Bakshi Chief Engineer (Planning Wing) Central Electricity AuthorityDocument69 pagesPower Scenario IN India: A.S.Bakshi Chief Engineer (Planning Wing) Central Electricity AuthorityRitesh KelkarNo ratings yet

- Electricity Generation Cost 2023Document35 pagesElectricity Generation Cost 2023taigerasNo ratings yet

- WND Enegry in IndiaDocument20 pagesWND Enegry in IndiaManohara Reddy PittuNo ratings yet

- MEPS three phase electric motorsDocument2 pagesMEPS three phase electric motorsAnonymous DJrec2No ratings yet

- Green Telecom TowersDocument4 pagesGreen Telecom TowersvishalbalechaNo ratings yet

- Modelling and Policy Analysis: Long-Term Power Options For IndiaDocument51 pagesModelling and Policy Analysis: Long-Term Power Options For IndiaAnkush GargNo ratings yet

- Overview of Power SectorDocument26 pagesOverview of Power SectorRameswar DashNo ratings yet

- National Electricity Policy: Objectives of The PolicyDocument5 pagesNational Electricity Policy: Objectives of The PolicySandeep YerraNo ratings yet

- 1.4 Power Sector MainDocument24 pages1.4 Power Sector MainAbhaSinghNo ratings yet

- TET 407 - Energy Planning, Regulation & Investment PlanningDocument69 pagesTET 407 - Energy Planning, Regulation & Investment PlanningMonterez SalvanoNo ratings yet

- EC Act 2001Document3 pagesEC Act 2001Yogesh ChaudhariNo ratings yet

- Implementation of Energy Conservation Act and BEE Action PlanDocument33 pagesImplementation of Energy Conservation Act and BEE Action PlanRohan PrakashNo ratings yet

- IRENA RE Latin America Policies 2015 Country ChileDocument9 pagesIRENA RE Latin America Policies 2015 Country ChileBarbara Hansen-DuncanNo ratings yet

- Power: Public SectorDocument4 pagesPower: Public SectorHitesh ShahNo ratings yet

- Korea New and Renewable Energy PolicyDocument23 pagesKorea New and Renewable Energy PolicyĐỗ Anh TuấnNo ratings yet

- Energy efficiency opportunities through ESCOsDocument16 pagesEnergy efficiency opportunities through ESCOscuvi17No ratings yet

- CCC CCC C C C CDocument20 pagesCCC CCC C C C CSwapnil RautNo ratings yet

- Kyung-Jin Boo - New & Renewable Energy Policy FIT Vs RPSDocument23 pagesKyung-Jin Boo - New & Renewable Energy Policy FIT Vs RPSAsia Clean Energy ForumNo ratings yet

- PTI Energy PolicyDocument52 pagesPTI Energy PolicyPTI Official100% (9)

- Report With The Scope of Measure 5.15 of The Second Regular Review of The Memorandum of Understanding On Specific Economic Policy ConditionalityDocument20 pagesReport With The Scope of Measure 5.15 of The Second Regular Review of The Memorandum of Understanding On Specific Economic Policy ConditionalityFilipe CaetanoNo ratings yet

- Group 6 Project ReportDocument10 pagesGroup 6 Project ReportGolam ZakariaNo ratings yet

- Electricity Generation Cost Report 2020Document72 pagesElectricity Generation Cost Report 2020Sanuwar RahmanNo ratings yet

- Answer Paper SustainabilityDocument18 pagesAnswer Paper Sustainabilityhiran meneripitiyaNo ratings yet

- Renewable Energy: Policy Analysis of Major ConsumersDocument8 pagesRenewable Energy: Policy Analysis of Major ConsumersAwaneesh ShuklaNo ratings yet

- The Eveolving Worldof PowerDocument16 pagesThe Eveolving Worldof Powergosalhs9395No ratings yet

- Global Power Sector TrendsDocument9 pagesGlobal Power Sector TrendsMuneer AhmedNo ratings yet

- FiT in Sri Lanka: Achieving Carbon Neutral Growth by 2020Document22 pagesFiT in Sri Lanka: Achieving Carbon Neutral Growth by 2020Murali HaripalanNo ratings yet

- On Africa 2010Document19 pagesOn Africa 2010MrHynaNo ratings yet

- PAT Scheme Drives Energy Efficiency in Cement SectorDocument44 pagesPAT Scheme Drives Energy Efficiency in Cement SectorrvnesariNo ratings yet

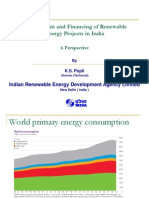

- Development and Financing of Renewable Energy Projects in IndiaDocument43 pagesDevelopment and Financing of Renewable Energy Projects in IndiaKishore KrishnaNo ratings yet

- Australia Lret WhitepaperDocument12 pagesAustralia Lret Whitepaperapi-248801082No ratings yet

- National Energy Policy 2013-18: A Critical ReviewDocument10 pagesNational Energy Policy 2013-18: A Critical ReviewShine BrightNo ratings yet

- Story: CoverDocument3 pagesStory: Covershanki359No ratings yet

- Unece-E8-Ebrd-Wec: Fostering Investment in Electricity Generation in Central and Eastern Europe and Central AsiaDocument32 pagesUnece-E8-Ebrd-Wec: Fostering Investment in Electricity Generation in Central and Eastern Europe and Central AsiaAhmet GülverenNo ratings yet

- Bangladesh Energy Efficiency ContextDocument7 pagesBangladesh Energy Efficiency ContextASHUTOSH RANJANNo ratings yet

- Grid Integrated Electrolysis Oct 31 2016Document66 pagesGrid Integrated Electrolysis Oct 31 2016amsukdNo ratings yet

- BEE PAT Booklet FinalDocument140 pagesBEE PAT Booklet Finaldinu_eshuNo ratings yet

- Unece-E8-Ebrd-Wec: Fostering Investment in Electricity Generation in Central and Eastern Europe and Central AsiaDocument32 pagesUnece-E8-Ebrd-Wec: Fostering Investment in Electricity Generation in Central and Eastern Europe and Central Asiaapi-295462696No ratings yet

- 1power ScenarioDocument46 pages1power Scenariosexyakshay2623No ratings yet

- Philippine Cobp Phi 2014 2016 Ssa 02Document6 pagesPhilippine Cobp Phi 2014 2016 Ssa 02LuthfieSangKaptenNo ratings yet

- Energy Storage: Legal and Regulatory Challenges and OpportunitiesFrom EverandEnergy Storage: Legal and Regulatory Challenges and OpportunitiesNo ratings yet

- Energy LawDocument8 pagesEnergy LawJaiy ChandharNo ratings yet

- Indian Electricity Act 2020 & Amendments: Key HighlightsDocument19 pagesIndian Electricity Act 2020 & Amendments: Key HighlightsRohit kumarNo ratings yet

- Saudi Arabia Energy Efficiency ReportDocument6 pagesSaudi Arabia Energy Efficiency Reportmohamad5357No ratings yet

- P Lutchman Embedded GX AMEU 19Document13 pagesP Lutchman Embedded GX AMEU 19Poonam HutheramNo ratings yet

- An Overview of Energy Scenarios, Storage Systems and The Infrastructure For Vehicle-To-Grid TechnologyDocument18 pagesAn Overview of Energy Scenarios, Storage Systems and The Infrastructure For Vehicle-To-Grid TechnologyKaiba Seto100% (1)

- Solar Parameter SummaryDocument5 pagesSolar Parameter Summarysrivastava_yugankNo ratings yet

- Renovation, Modernization and Life Extension of Power PlantsDocument24 pagesRenovation, Modernization and Life Extension of Power PlantskrcdewanewNo ratings yet

- AGHAM Fit System Briefer PDFDocument9 pagesAGHAM Fit System Briefer PDFRichardNo ratings yet

- Climatic Change 2. Advances in Renewable Energy 3. Rapid Urbanization 4. Battery Chemistry 5. Energy SecurityDocument46 pagesClimatic Change 2. Advances in Renewable Energy 3. Rapid Urbanization 4. Battery Chemistry 5. Energy Securitymail meNo ratings yet

- MEDA Initiative On Energy Conservation Act in Maharashtra: Hemantkumar H. PatilDocument59 pagesMEDA Initiative On Energy Conservation Act in Maharashtra: Hemantkumar H. PatilNilesh KhadeNo ratings yet

- Energy Scenario in IndiaDocument13 pagesEnergy Scenario in IndiaTado LehnsherrNo ratings yet

- Electric Vehicles and Their Impact To The Electric Grid in Isolated SystemsDocument6 pagesElectric Vehicles and Their Impact To The Electric Grid in Isolated SystemsaaakshaybhargavaNo ratings yet

- Electricity Demand and Generation ScenariosDocument40 pagesElectricity Demand and Generation ScenariosEsperance KAMPIRENo ratings yet

- World energy markets and the future of oilDocument10 pagesWorld energy markets and the future of oilRisang PrasajiNo ratings yet

- Electricity Storage and Renewables Cost and Markets 2030From EverandElectricity Storage and Renewables Cost and Markets 2030No ratings yet

- EU China Energy Magazine 2023 September Issue: 2023, #8From EverandEU China Energy Magazine 2023 September Issue: 2023, #8No ratings yet

- conl.12684Document14 pagesconl.12684AWARARAHINo ratings yet

- ANL. Report of Water Sample During Ganesh Festival - AnnexDocument11 pagesANL. Report of Water Sample During Ganesh Festival - AnnexAWARARAHINo ratings yet

- Standard For Nursery ManagementDocument27 pagesStandard For Nursery ManagementAWARARAHINo ratings yet

- 09 - Chapter 2Document39 pages09 - Chapter 2AWARARAHINo ratings yet

- Energy Scenario and Vision 2020 in IndiaDocument11 pagesEnergy Scenario and Vision 2020 in IndiaKhalid AnwarNo ratings yet

- NH StatewiseDocument13 pagesNH StatewiseAbha MalikNo ratings yet

- Energy in India's Future: InsightsDocument194 pagesEnergy in India's Future: InsightsIfri EnergieNo ratings yet

- Zoo Education Master Plan PDFDocument330 pagesZoo Education Master Plan PDFAWARARAHINo ratings yet

- ChhattisgarhDocument28 pagesChhattisgarhAWARARAHI100% (1)

- Energy Subsidy Reform-Lessons and ImplicationsDocument68 pagesEnergy Subsidy Reform-Lessons and ImplicationsOladipupo Mayowa PaulNo ratings yet

- B A (Hons) German Paper II Language in WritingDocument2 pagesB A (Hons) German Paper II Language in WritingAWARARAHINo ratings yet

- Ba Hons II German Paper IVDocument2 pagesBa Hons II German Paper IVAWARARAHINo ratings yet

- Solar Power in India Opportunities & Challenges: Anand Gupta Co Founder & EditorDocument16 pagesSolar Power in India Opportunities & Challenges: Anand Gupta Co Founder & EditorAWARARAHINo ratings yet

- Energy Resources of IndiaDocument19 pagesEnergy Resources of IndiaAWARARAHINo ratings yet

- B.A. Prog II German Paper II Study of The LanguageDocument3 pagesB.A. Prog II German Paper II Study of The LanguageAWARARAHINo ratings yet

- German Regular Verbs - Pres. TenseDocument3 pagesGerman Regular Verbs - Pres. TenseAWARARAHI100% (1)

- EarthquakeDocument42 pagesEarthquakeAWARARAHINo ratings yet

- Vegetation Types PDFDocument7 pagesVegetation Types PDFAWARARAHINo ratings yet

- Phylogenetic Evaluation of Species Nomenclature Of: Pestalotiopsis in Relation To Host AssociationDocument17 pagesPhylogenetic Evaluation of Species Nomenclature Of: Pestalotiopsis in Relation To Host AssociationAWARARAHINo ratings yet

- Index 2Document2 pagesIndex 2AWARARAHINo ratings yet

- PUMP SELECTION GUIDEDocument13 pagesPUMP SELECTION GUIDEHeymonth ChandraNo ratings yet

- EPL Lab ManualDocument74 pagesEPL Lab ManualPrince Vineeth67% (3)

- Journal of Molecular Liquids: Mohammad Hatami Maryam Hasanpour, Dengwei JingDocument22 pagesJournal of Molecular Liquids: Mohammad Hatami Maryam Hasanpour, Dengwei JingSugam KarkiNo ratings yet

- Komatsu D85 A-21 Crawler Tractor PDFDocument2 pagesKomatsu D85 A-21 Crawler Tractor PDFrandy patah asbiNo ratings yet

- Daqing Petroleum Iraq Branch Job Safety Analysis 工作安全分析: Pressure Testing Bop'SDocument2 pagesDaqing Petroleum Iraq Branch Job Safety Analysis 工作安全分析: Pressure Testing Bop'SkhurramNo ratings yet

- TSX ULT Freezers - NorthAmerica - 0719 v2 PDFDocument9 pagesTSX ULT Freezers - NorthAmerica - 0719 v2 PDFambitiousamit1No ratings yet

- Maq. Helados Taylor sC707 PDFDocument2 pagesMaq. Helados Taylor sC707 PDFxray123zzzNo ratings yet

- Asphalts Catalog Tcm14-55227Document54 pagesAsphalts Catalog Tcm14-55227Savaşer YetişNo ratings yet

- MDS1525Document5 pagesMDS1525mirandowebsNo ratings yet

- Boq Gabung Gi Teluk Naga Ii - Full Digital.r3-SentDocument237 pagesBoq Gabung Gi Teluk Naga Ii - Full Digital.r3-SentTika LorenzaNo ratings yet

- MC34063 DWSDocument9 pagesMC34063 DWSTayyeb AliNo ratings yet

- Epoch Oper Eff vs. Drilling EffDocument41 pagesEpoch Oper Eff vs. Drilling EffBobby Worrawongwanna David WhuwanNo ratings yet

- Everything You Ever Wanted To Know About Crankcase ExplosionDocument2 pagesEverything You Ever Wanted To Know About Crankcase ExplosionGiorgi KandelakiNo ratings yet

- TSB1380YGSDocument2 pagesTSB1380YGSlelopNo ratings yet

- LCCF Book Version 2 2017Document116 pagesLCCF Book Version 2 2017IkhwanNo ratings yet

- Sac - WacDocument4 pagesSac - WacAdyasa ChoudhuryNo ratings yet

- Electronic Fuel Injection: Basic System PartsDocument4 pagesElectronic Fuel Injection: Basic System PartsSantosh TrimbakeNo ratings yet

- Energy Conservation and ManagementDocument2 pagesEnergy Conservation and ManagementkannanchammyNo ratings yet

- v1903 2203tvengineDocument46 pagesv1903 2203tvenginehuo sun100% (1)

- Dr. Angus McKay's CV for Drilling Supervisor RoleDocument5 pagesDr. Angus McKay's CV for Drilling Supervisor Roleahmalisha2No ratings yet

- Basic USIT Interpretation - SLB Presentation, 2009Document18 pagesBasic USIT Interpretation - SLB Presentation, 2009alizareiforoushNo ratings yet

- Laser TherapyDocument8 pagesLaser Therapyinrmpt77No ratings yet

- Free Surface Flow Simulation With ACUSIM in The Water IndustryDocument8 pagesFree Surface Flow Simulation With ACUSIM in The Water IndustryKhiladi PujariNo ratings yet

- Random VariablesDocument11 pagesRandom VariablesJoaquin MelgarejoNo ratings yet

- Basic Hydraulic Systems Components GuideDocument67 pagesBasic Hydraulic Systems Components Guidesba98No ratings yet

- Trouble Shooting: Causes RemedyDocument3 pagesTrouble Shooting: Causes RemedyredouaneNo ratings yet

- BSM SM CVDocument36 pagesBSM SM CValexsmn100% (1)

- Roof Insulation: Southern California Gas Company New Buildings Institute Advanced Design Guideline SeriesDocument31 pagesRoof Insulation: Southern California Gas Company New Buildings Institute Advanced Design Guideline Seriesapi-19789368100% (1)

- HVAC Air Filters Catalogue Provides Clean Air SolutionsDocument6 pagesHVAC Air Filters Catalogue Provides Clean Air SolutionssemoyapaNo ratings yet

- Golden rules of work permitsDocument18 pagesGolden rules of work permitsRusihan HSENo ratings yet