You might also like

- National RoboSprint 2015 Educational CampaignDocument21 pagesNational RoboSprint 2015 Educational CampaignSuleman RanaNo ratings yet

- Customer Satisfaction 23Document18 pagesCustomer Satisfaction 23Suleman RanaNo ratings yet

- Nawaz Ahmad HBLDocument3 pagesNawaz Ahmad HBLSuleman RanaNo ratings yet

- IKMC 2012 Answers for Pre-Ecolier to Junior LevelsDocument1 pageIKMC 2012 Answers for Pre-Ecolier to Junior LevelsSuleman RanaNo ratings yet

- Internship Report of HBLDocument63 pagesInternship Report of HBLfuadh_1No ratings yet

- IKMC 2012 Answers for Pre-Ecolier to Junior LevelsDocument1 pageIKMC 2012 Answers for Pre-Ecolier to Junior LevelsSuleman RanaNo ratings yet

- SIEMENS Final Repor JhhiefjetDocument45 pagesSIEMENS Final Repor JhhiefjetSuleman RanaNo ratings yet

- Leadership 12544Document8 pagesLeadership 12544Suleman RanaNo ratings yet

- SIEMENS Final Repor JhhiefjetDocument45 pagesSIEMENS Final Repor JhhiefjetSuleman RanaNo ratings yet

- Leadership 2Document22 pagesLeadership 2Suleman RanaNo ratings yet

- Leadership 12544Document8 pagesLeadership 12544Suleman RanaNo ratings yet

- Physics Measurement QuizDocument1 pagePhysics Measurement QuizSuleman RanaNo ratings yet

- Teacher Job DiscriptionDocument6 pagesTeacher Job DiscriptionSuleman RanaNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- 028 Ptrs Modul Matematik t4 Sel-96-99Document4 pages028 Ptrs Modul Matematik t4 Sel-96-99mardhiah88No ratings yet

- FORM 10-K: United States Securities and Exchange CommissionDocument55 pagesFORM 10-K: United States Securities and Exchange CommissionJerome PadillaNo ratings yet

- Joinpdf PDFDocument1,043 pagesJoinpdf PDFOwen Bawlor ManozNo ratings yet

- Project Report On Analysis of Indian BankDocument74 pagesProject Report On Analysis of Indian Banksanthoshni81% (27)

- Partnership AgreementDocument4 pagesPartnership AgreementJohn Mark Paracad100% (2)

- Sub Order LabelsDocument2 pagesSub Order LabelsZeeshan naseemNo ratings yet

- Mutual Funds ExplainedDocument11 pagesMutual Funds ExplainedjchazneyNo ratings yet

- Steel Industry: Contribution in The Development of India's Economic GrowthDocument28 pagesSteel Industry: Contribution in The Development of India's Economic GrowthAditya YadavNo ratings yet

- 5 Parkin Samantha Chapter 2 - Measuring Your Financial Health and Making A PlanDocument6 pages5 Parkin Samantha Chapter 2 - Measuring Your Financial Health and Making A Planapi-245262597100% (1)

- NFLX Initiating Coverage JSDocument12 pagesNFLX Initiating Coverage JSBrian BolanNo ratings yet

- Asset Liability Management in BanksDocument8 pagesAsset Liability Management in Bankskpved92No ratings yet

- Axis Bank - FINANCIAL OVERVIEW OF AXIS BANK & COMPARATIVE STUDY OF CURRENT ACCOUNT AND SAVING ACCDocument93 pagesAxis Bank - FINANCIAL OVERVIEW OF AXIS BANK & COMPARATIVE STUDY OF CURRENT ACCOUNT AND SAVING ACCAmol Sinha56% (9)

- Lead QuesDocument2 pagesLead QuesKameshwara RaoNo ratings yet

- OP 4.09 Pest ManagementDocument2 pagesOP 4.09 Pest ManagementRina YulianiNo ratings yet

- REVIEW OF LITERATURE - Asset and Liability ManagementDocument3 pagesREVIEW OF LITERATURE - Asset and Liability ManagementSherl AugustNo ratings yet

- By LawsDocument15 pagesBy LawsVholts Villa VitugNo ratings yet

- Comprehensive Project ReportDocument13 pagesComprehensive Project ReportRishi KanjaniNo ratings yet

- Cost Management of Engineering Projects PDFDocument30 pagesCost Management of Engineering Projects PDFPooja Jariwala50% (4)

- Philippine Laws on Credit TransactionsDocument5 pagesPhilippine Laws on Credit TransactionsCamille ArominNo ratings yet

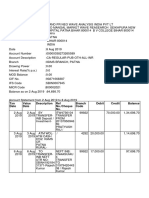

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument3 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceNishi GuptaNo ratings yet

- IIBPS PO DI English - pdf-38 PDFDocument11 pagesIIBPS PO DI English - pdf-38 PDFRahul GaurNo ratings yet

- Oman Issues Executive Regulations for Income Tax LawDocument44 pagesOman Issues Executive Regulations for Income Tax LawavineroNo ratings yet

- Own Mock QualiDocument10 pagesOwn Mock QualiDarwin John SantosNo ratings yet

- Management Accounting: 2 Year ExaminationDocument24 pagesManagement Accounting: 2 Year ExaminationChansa KapambweNo ratings yet

- Bab 2 AklDocument4 pagesBab 2 AklNaomi NovelinNo ratings yet

- Prelio SDocument55 pagesPrelio Sjohnface12No ratings yet

- Acquisition of GC by Tata ChemDocument20 pagesAcquisition of GC by Tata ChemPhalguna ReddyNo ratings yet

- BiographyDocument32 pagesBiographyranarahmanNo ratings yet