You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- 2016 - Pilipinas Shell V Commissioner of Customs - 195876Document3 pages2016 - Pilipinas Shell V Commissioner of Customs - 195876Anonymous sgEtt467% (3)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Quiz On Percentage Tax and Documentary Stamps TaxDocument4 pagesQuiz On Percentage Tax and Documentary Stamps Taxncllpdll100% (4)

- Doing Business Guide OmanDocument12 pagesDoing Business Guide OmanhazimNo ratings yet

- International Business - Pulses Export BPLAN PDFDocument30 pagesInternational Business - Pulses Export BPLAN PDFSangram Jagtap100% (1)

- Introduction to SAP Global Trade Services (GTSDocument3 pagesIntroduction to SAP Global Trade Services (GTSGuru PrasadNo ratings yet

- Value Added Tax-Summary LectureDocument18 pagesValue Added Tax-Summary LectureUy SamuelNo ratings yet

- PD 1464 Tariff and Customs Code of The Philippines - Vol 1&2Document120 pagesPD 1464 Tariff and Customs Code of The Philippines - Vol 1&2Renz Ruiz100% (2)

- Farolan Vs CTADocument1 pageFarolan Vs CTAKat Jolejole100% (2)

- Joint Admin OrderDocument53 pagesJoint Admin OrderBelle MadrigalNo ratings yet

- Thematic Activities On TradeDocument24 pagesThematic Activities On TradeMaleehaNo ratings yet

- Meaning: Customs DutyDocument2 pagesMeaning: Customs DutySOBICA KNo ratings yet

- Bureau of Customs Draft Order On Compulsory Acquisition For Undervalued GoodsDocument6 pagesBureau of Customs Draft Order On Compulsory Acquisition For Undervalued GoodsPortCallsNo ratings yet

- Services & Surcharges GUIDE 2019 DHL Express IndiaDocument2 pagesServices & Surcharges GUIDE 2019 DHL Express IndiasanjeevNo ratings yet

- Oyu Tolgoi Purchase Order General Conditions For The Supply of Goods (October 2022)Document25 pagesOyu Tolgoi Purchase Order General Conditions For The Supply of Goods (October 2022)Undral NatsagNo ratings yet

- LEU 3 Customs Union & Fiscal Barriers To Trade Final PPT 20Document47 pagesLEU 3 Customs Union & Fiscal Barriers To Trade Final PPT 20izzamarisaNo ratings yet

- Deferred Inspection Sites 111915Document12 pagesDeferred Inspection Sites 111915AJNo ratings yet

- 2 - CBNC vs. CIRDocument13 pages2 - CBNC vs. CIRJeanne CalalinNo ratings yet

- Ghana Revenue Authority Customs GuideDocument8 pagesGhana Revenue Authority Customs Guidejose300No ratings yet

- Customs Duty or VAT dispute formDocument1 pageCustoms Duty or VAT dispute formEva Fitch KnottNo ratings yet

- Guide to Preshipment Inspection AppealsDocument8 pagesGuide to Preshipment Inspection Appealsابوالحروف العربي ابوالحروفNo ratings yet

- Economics - Commerce - Capsule - Part - II PDFDocument12 pagesEconomics - Commerce - Capsule - Part - II PDFSumera SoomroNo ratings yet

- Ijcepa Basic AgreementDocument1,083 pagesIjcepa Basic AgreementgeorgevoommenNo ratings yet

- SudanDocument2 pagesSudanKelz YouknowmynameNo ratings yet

- Royal Mail Our Prices 25 March 2019 46305575 PDFDocument9 pagesRoyal Mail Our Prices 25 March 2019 46305575 PDFZakiur Rahman KhanNo ratings yet

- Systems, Processes and Challenges of Public Revenue Collection in ZimbabweDocument12 pagesSystems, Processes and Challenges of Public Revenue Collection in ZimbabwePrince Wayne SibandaNo ratings yet

- Kapatiran Vs TanDocument3 pagesKapatiran Vs TanWinnie Ann Daquil LomosadNo ratings yet

- Tamil Nadu Tnvat ActDocument63 pagesTamil Nadu Tnvat ActsamaadhuNo ratings yet

- Ibc 2 Pager PDFDocument2 pagesIbc 2 Pager PDFsam yadavNo ratings yet

- Bir Ruling (Da-031-07)Document2 pagesBir Ruling (Da-031-07)Stacy Liong BloggerAccountNo ratings yet

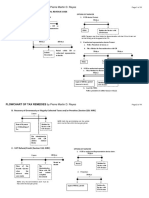

- Flowchart of Tax Remedies 2017 Update PRDocument11 pagesFlowchart of Tax Remedies 2017 Update PRMarjorie Kate CresciniNo ratings yet