You might also like

- Financial Services Firms: Governance, Regulations, Valuations, Mergers, and AcquisitionsFrom EverandFinancial Services Firms: Governance, Regulations, Valuations, Mergers, and AcquisitionsNo ratings yet

- Embedded Value Calculation For A Life Insurance CompanyDocument27 pagesEmbedded Value Calculation For A Life Insurance CompanyJoin RiotNo ratings yet

- B Pension Risk TransferDocument7 pagesB Pension Risk TransferMikhail FrancisNo ratings yet

- Goldman Sachs Presentation To Credit Suisse Financial Services ConferenceDocument20 pagesGoldman Sachs Presentation To Credit Suisse Financial Services ConferenceEveline WangNo ratings yet

- Life InsuranceDocument17 pagesLife Insurancerchawdhry123No ratings yet

- The Financial Advisor M&A Guidebook: Best Practices, Tools, and Resources for Technology Integration and BeyondFrom EverandThe Financial Advisor M&A Guidebook: Best Practices, Tools, and Resources for Technology Integration and BeyondNo ratings yet

- Insurance AccountingDocument16 pagesInsurance Accountingssp2000No ratings yet

- Bushee-2004-Journal of Applied Corporate FinanceDocument10 pagesBushee-2004-Journal of Applied Corporate Financeaa2007No ratings yet

- Audit Committee Quality of EarningsDocument3 pagesAudit Committee Quality of EarningsJilesh PabariNo ratings yet

- 1.4corporate Business Law PDFDocument180 pages1.4corporate Business Law PDFMohamed LaminNo ratings yet

- EV and VNB MethodologyDocument2 pagesEV and VNB MethodologySaravanan BalakrishnanNo ratings yet

- Lbo Model Long FormDocument5 pagesLbo Model Long FormGabriella RicardoNo ratings yet

- The Pension Risk Transfer Market at $260 BillionDocument16 pagesThe Pension Risk Transfer Market at $260 BillionImranullah KhanNo ratings yet

- European Re InsuranceDocument95 pagesEuropean Re InsuranceKapil MehtaNo ratings yet

- McKinsey Life Insurance 2.0Document52 pagesMcKinsey Life Insurance 2.0Moushumi DharNo ratings yet

- USS Global Equity Fund FactsheetDocument1 pageUSS Global Equity Fund Factsheetsteven burnsNo ratings yet

- Private Equity Unchained: Strategy Insights for the Institutional InvestorFrom EverandPrivate Equity Unchained: Strategy Insights for the Institutional InvestorNo ratings yet

- Basel II Risk Weight FunctionsDocument31 pagesBasel II Risk Weight FunctionsmargusroseNo ratings yet

- Critical Financial Review: Understanding Corporate Financial InformationFrom EverandCritical Financial Review: Understanding Corporate Financial InformationNo ratings yet

- What Is The Difference Between Book Value and Market ValueDocument12 pagesWhat Is The Difference Between Book Value and Market ValueAinie Intwines100% (1)

- How to structure investments to protect downsideDocument6 pagesHow to structure investments to protect downsidehelloNo ratings yet

- 157 28235 EA419 2012 1 2 1 CH 08Document38 pages157 28235 EA419 2012 1 2 1 CH 08devidoyNo ratings yet

- Sector Specific Ratios and ValuationDocument10 pagesSector Specific Ratios and ValuationAbhishek SinghNo ratings yet

- Debt Service Coverage Ratio DSCR Net Income/ DebtDocument10 pagesDebt Service Coverage Ratio DSCR Net Income/ DebtAlvaroDeCampsNo ratings yet

- Enterprise Risk Management A Complete Guide - 2019 EditionFrom EverandEnterprise Risk Management A Complete Guide - 2019 EditionNo ratings yet

- Wealth & Asset ManagementDocument17 pagesWealth & Asset ManagementVishnuSimmhaAgnisagarNo ratings yet

- Leadership Risk: A Guide for Private Equity and Strategic InvestorsFrom EverandLeadership Risk: A Guide for Private Equity and Strategic InvestorsNo ratings yet

- Capital Structure of An LBO PDFDocument3 pagesCapital Structure of An LBO PDFTim OttoNo ratings yet

- ContentServer 9 PDFDocument17 pagesContentServer 9 PDFDanudear DanielNo ratings yet

- Process and Asset Valuation A Complete Guide - 2019 EditionFrom EverandProcess and Asset Valuation A Complete Guide - 2019 EditionNo ratings yet

- Applied Corporate Finance: Journal ofDocument15 pagesApplied Corporate Finance: Journal ofFilouNo ratings yet

- IveyMBA Permanent Employment Report PDFDocument10 pagesIveyMBA Permanent Employment Report PDFUmesh T NNo ratings yet

- Alternative Investment Strategies A Complete Guide - 2020 EditionFrom EverandAlternative Investment Strategies A Complete Guide - 2020 EditionNo ratings yet

- Financial Fine Print: Uncovering a Company's True ValueFrom EverandFinancial Fine Print: Uncovering a Company's True ValueRating: 3 out of 5 stars3/5 (3)

- FCFE Vs DCFF Module 8 (Class 28)Document9 pagesFCFE Vs DCFF Module 8 (Class 28)Vineet AgarwalNo ratings yet

- Chapter 11 Leveraged Buyout Structures and ValuationDocument27 pagesChapter 11 Leveraged Buyout Structures and ValuationanubhavhinduNo ratings yet

- Mid MonthDocument4 pagesMid Monthcipollini50% (2)

- Assignment 3 - Financial Case StudyDocument1 pageAssignment 3 - Financial Case StudySenura SeneviratneNo ratings yet

- Investment Ideas - Capital Market Assumptions (CMA) Methodology - 5 July 2012 - (Credit Suisse) PDFDocument24 pagesInvestment Ideas - Capital Market Assumptions (CMA) Methodology - 5 July 2012 - (Credit Suisse) PDFQuantDev-MNo ratings yet

- Business Valuation ManagementDocument42 pagesBusiness Valuation ManagementRakesh SinghNo ratings yet

- ASEAN Corporate Governance Scorecard Country Reports and Assessments 2019From EverandASEAN Corporate Governance Scorecard Country Reports and Assessments 2019No ratings yet

- Private Companies (Very Small Businesses) Key Financial DifferencesDocument50 pagesPrivate Companies (Very Small Businesses) Key Financial DifferencesFarhan ShafiqueNo ratings yet

- Ohlson 2007Document10 pagesOhlson 2007mzurzdcoNo ratings yet

- Chapter One: Mcgraw-Hill/IrwinDocument17 pagesChapter One: Mcgraw-Hill/Irwinteraz2810No ratings yet

- Tax Issues in Purchase and Sale AgreementsDocument20 pagesTax Issues in Purchase and Sale AgreementsTaichi ChenNo ratings yet

- Guideline D-9: Source of Earnings Disclosure for Life Insurance CompaniesDocument7 pagesGuideline D-9: Source of Earnings Disclosure for Life Insurance CompaniesFredericYudhistiraDharmawataNo ratings yet

- Reformulation - Analysis of SCFDocument17 pagesReformulation - Analysis of SCFAkib Mahbub KhanNo ratings yet

- Starboard Value LP LetterDocument4 pagesStarboard Value LP Lettersumit.bitsNo ratings yet

- The Role of The Insurance Industry Association: Brad Smith and Diana KeeganDocument30 pagesThe Role of The Insurance Industry Association: Brad Smith and Diana Keeganrajesh_natarajan_4No ratings yet

- Financial Modeling ExamplesDocument8 pagesFinancial Modeling ExamplesRohit BajpaiNo ratings yet

- Financial Modeling Fundamentals QuizDocument10 pagesFinancial Modeling Fundamentals QuizdafxNo ratings yet

- Investment Risk and Return AnalysisDocument20 pagesInvestment Risk and Return AnalysisravaladityaNo ratings yet

- REIT (Real Estate Investment Trust) Valuation 101: Would You Like A Dividend With Your Funds From Operations?Document16 pagesREIT (Real Estate Investment Trust) Valuation 101: Would You Like A Dividend With Your Funds From Operations?ziuziNo ratings yet

- Credit Models and the Crisis: A Journey into CDOs, Copulas, Correlations and Dynamic ModelsFrom EverandCredit Models and the Crisis: A Journey into CDOs, Copulas, Correlations and Dynamic ModelsNo ratings yet

- Article - Mercer Capital Guide Option Pricing ModelDocument18 pagesArticle - Mercer Capital Guide Option Pricing ModelKshitij SharmaNo ratings yet

- Capital Structure: Capital Structure Refers To The Amount of Debt And/or Equity Employed by ADocument12 pagesCapital Structure: Capital Structure Refers To The Amount of Debt And/or Equity Employed by AKath LeynesNo ratings yet

- 9M 2013 Unaudited ResultsDocument2 pages9M 2013 Unaudited ResultsOladipupo Mayowa PaulNo ratings yet

- Amcon Bonds FaqDocument4 pagesAmcon Bonds FaqOladipupo Mayowa PaulNo ratings yet

- 9854 Goldlink Insurance Audited 2013 Financial Statements May 2015Document3 pages9854 Goldlink Insurance Audited 2013 Financial Statements May 2015Oladipupo Mayowa PaulNo ratings yet

- Filling Station GuidelinesDocument8 pagesFilling Station GuidelinesOladipupo Mayowa PaulNo ratings yet

- Best Practice Guidelines Governing Analyst-Corporate Issuer Relations - CFADocument16 pagesBest Practice Guidelines Governing Analyst-Corporate Issuer Relations - CFAOladipupo Mayowa PaulNo ratings yet

- First City Monument Bank PLC.: Investor/Analyst Presentation Review of H1 2008/9 ResultsDocument31 pagesFirst City Monument Bank PLC.: Investor/Analyst Presentation Review of H1 2008/9 ResultsOladipupo Mayowa PaulNo ratings yet

- IBT199 IBTC Q1 2014 Holdings Press Release PRINTDocument1 pageIBT199 IBTC Q1 2014 Holdings Press Release PRINTOladipupo Mayowa PaulNo ratings yet

- Abridged Financial Statement September 2012Document2 pagesAbridged Financial Statement September 2012Oladipupo Mayowa PaulNo ratings yet

- IBT199 IBTC Q1 2014 Holdings Press Release PRINTDocument1 pageIBT199 IBTC Q1 2014 Holdings Press Release PRINTOladipupo Mayowa PaulNo ratings yet

- Diamond Bank Half Year Results 2011 SummaryDocument5 pagesDiamond Bank Half Year Results 2011 SummaryOladipupo Mayowa PaulNo ratings yet

- FCMB Group PLC 3Q13 (IFRS) Group Results Investors & Analysts PresentationDocument32 pagesFCMB Group PLC 3Q13 (IFRS) Group Results Investors & Analysts PresentationOladipupo Mayowa PaulNo ratings yet

- FCMB Group PLC Announces HY13 (Unaudited) IFRS-Compliant Group Results - AmendedDocument4 pagesFCMB Group PLC Announces HY13 (Unaudited) IFRS-Compliant Group Results - AmendedOladipupo Mayowa PaulNo ratings yet

- q1 2008 09 ResultsDocument1 pageq1 2008 09 ResultsOladipupo Mayowa PaulNo ratings yet

- q1 2008 09 ResultsDocument1 pageq1 2008 09 ResultsOladipupo Mayowa PaulNo ratings yet

- FirstCity Group profit up 88% in 3 monthsDocument1 pageFirstCity Group profit up 88% in 3 monthsOladipupo Mayowa PaulNo ratings yet

- 2007 Q2resultsDocument1 page2007 Q2resultsOladipupo Mayowa PaulNo ratings yet

- 2006 Q1resultsDocument1 page2006 Q1resultsOladipupo Mayowa PaulNo ratings yet

- 2011 Year End Results Press Release - FinalDocument2 pages2011 Year End Results Press Release - FinalOladipupo Mayowa PaulNo ratings yet

- 5 Year Financial Report 2010Document3 pages5 Year Financial Report 2010Oladipupo Mayowa PaulNo ratings yet

- 9-Months 2012 IFRS Unaudited Financial Statements FINAL - With Unaudited December 2011Document5 pages9-Months 2012 IFRS Unaudited Financial Statements FINAL - With Unaudited December 2011Oladipupo Mayowa PaulNo ratings yet

- 5 Year Financial Report 2010Document3 pages5 Year Financial Report 2010Oladipupo Mayowa PaulNo ratings yet

- GTBank H1 2011 Results PresentationDocument17 pagesGTBank H1 2011 Results PresentationOladipupo Mayowa PaulNo ratings yet

- June 2009 Half Year Financial Statement GaapDocument78 pagesJune 2009 Half Year Financial Statement GaapOladipupo Mayowa PaulNo ratings yet

- GTBank FY 2011 Results PresentationDocument16 pagesGTBank FY 2011 Results PresentationOladipupo Mayowa PaulNo ratings yet

- 2011 Half Year Result StatementDocument3 pages2011 Half Year Result StatementOladipupo Mayowa PaulNo ratings yet

- Dec09 Inv Presentation GAAPDocument23 pagesDec09 Inv Presentation GAAPOladipupo Mayowa PaulNo ratings yet

- GTBank H1 2012 Results AnalysisDocument17 pagesGTBank H1 2012 Results AnalysisOladipupo Mayowa PaulNo ratings yet

- Final Fs 2012 Gtbank BV 2012Document16 pagesFinal Fs 2012 Gtbank BV 2012Oladipupo Mayowa PaulNo ratings yet

- Fs 2011 GtbankDocument17 pagesFs 2011 GtbankOladipupo Mayowa PaulNo ratings yet

- MINNA PADI INVESTAMA SEKURITAS 2017 ANNUAL REPORTDocument158 pagesMINNA PADI INVESTAMA SEKURITAS 2017 ANNUAL REPORTRina KusumaNo ratings yet

- E-banking services explainedDocument12 pagesE-banking services explainedSaniya MhateNo ratings yet

- G.R. No. 174269 - Pantaleon Vs AmEx (2009)Document3 pagesG.R. No. 174269 - Pantaleon Vs AmEx (2009)Sarah Jade LayugNo ratings yet

- Isa 805Document13 pagesIsa 805baabasaamNo ratings yet

- Bangladesh Development Bank loan application formDocument27 pagesBangladesh Development Bank loan application formJadid HoqueNo ratings yet

- Life Cycle of A LoanDocument12 pagesLife Cycle of A LoanSyed Noman AhmedNo ratings yet

- AudprobDocument3 pagesAudprobJonalyn MoralesNo ratings yet

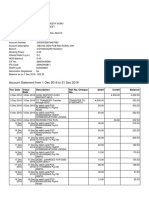

- Account Statement From 1 Dec 2016 To 31 Dec 2016: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Dec 2016 To 31 Dec 2016: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceENDLURI DEEPAK KUMARNo ratings yet

- Afar 106 - Home Office and Branch Accounting PDFDocument3 pagesAfar 106 - Home Office and Branch Accounting PDFReyn Saplad PeralesNo ratings yet

- Request PaymentDocument37 pagesRequest Paymentsaodahshidah100% (1)

- Sip Report - Bajaj MBADocument49 pagesSip Report - Bajaj MBAGaurav MantalaNo ratings yet

- Agent Name, License No & IRDA URN ListDocument20 pagesAgent Name, License No & IRDA URN ListHarshad BhirudNo ratings yet

- Bank Statement 2Document1 pageBank Statement 2bc180204979 ALI FAROOQNo ratings yet

- The Reasons of This Question: 2. Levels of Career GoalsDocument17 pagesThe Reasons of This Question: 2. Levels of Career GoalsRaviraj ZalaNo ratings yet

- Shippers Letter of InstructionDocument2 pagesShippers Letter of InstructionWilliam LooNo ratings yet

- SAP Question BankDocument33 pagesSAP Question Bankpunithan81No ratings yet

- Session 14 Digest CHARLES LEE V CADocument3 pagesSession 14 Digest CHARLES LEE V CAAnna Marie DayanghirangNo ratings yet

- Constitutions Heeb Farmers AssociationDocument20 pagesConstitutions Heeb Farmers AssociationSamoon Khan Ahmadzai100% (2)

- Lala Shanti Swarup Vs Munshi Singh & Ors On 3 January, 1967Document5 pagesLala Shanti Swarup Vs Munshi Singh & Ors On 3 January, 1967Knowledge GuruNo ratings yet

- Application Forms, Financial Results, EMI Calculator and MoreDocument21 pagesApplication Forms, Financial Results, EMI Calculator and MoreRohanTheGreatNo ratings yet

- 2 LetterDocument9 pages2 LetterSaif AzmanNo ratings yet

- Acme Shoe, Rubber and Plastic Corporation v. CA - Scire LicetDocument2 pagesAcme Shoe, Rubber and Plastic Corporation v. CA - Scire LicetRonn PagcoNo ratings yet

- Bills of ExchangeDocument16 pagesBills of ExchangeswayamNo ratings yet

- Impact of Cashback Offers On Consumer BehaviorDocument10 pagesImpact of Cashback Offers On Consumer BehaviorsonikaNo ratings yet

- Streamline Unlimited Account: Closing Balance $3,265.34 CR Enquiries 13 2221Document4 pagesStreamline Unlimited Account: Closing Balance $3,265.34 CR Enquiries 13 2221jo220171No ratings yet

- Pengetahuan Cargo 2016Document121 pagesPengetahuan Cargo 2016danu yp100% (3)

- Marine and Energy CoversDocument13 pagesMarine and Energy CoversmanojvarrierNo ratings yet

- Barbados Credit Unions Funeral InsuranceDocument12 pagesBarbados Credit Unions Funeral InsuranceKammieNo ratings yet

- Prepare The Cash BookDocument4 pagesPrepare The Cash BookShaloom TV100% (1)

- B3 PDFDocument465 pagesB3 PDFabdulramani mbwana100% (7)