You might also like

- Master BudgetDocument5 pagesMaster BudgetSaranyaa KanagarajNo ratings yet

- General AwarenessDocument525 pagesGeneral AwarenessAshitha M R Dilin100% (1)

- Chapter 16 - AnswerDocument8 pagesChapter 16 - Answerwynellamae100% (2)

- Hotel Master Critical PathDocument14 pagesHotel Master Critical Pathtaola80% (25)

- Internal ControlsDocument17 pagesInternal ControlsSitti Najwa100% (1)

- Auditing and Assurance Services TBDocument65 pagesAuditing and Assurance Services TBgilli1tr100% (2)

- Fiba PDFDocument302 pagesFiba PDFSubodh singhNo ratings yet

- Module in BudgetingDocument5 pagesModule in BudgetingJade TanNo ratings yet

- Developing Operating & Capital BudgetingDocument48 pagesDeveloping Operating & Capital Budgetingapi-3742302100% (2)

- Hca16ge Ch06 SMDocument76 pagesHca16ge Ch06 SMAmanda GuanNo ratings yet

- Financial Planning and Control ProcessDocument3 pagesFinancial Planning and Control ProcessPRINCESS HONEYLET SIGESMUNDONo ratings yet

- Management Accounting - HCA16ge - Ch6Document76 pagesManagement Accounting - HCA16ge - Ch6Corliss Ko100% (3)

- Master Budget QuestionsDocument19 pagesMaster Budget QuestionsSwathi Ashok100% (2)

- UNIT-3 Financial Planning and ForecastingDocument33 pagesUNIT-3 Financial Planning and ForecastingAssfaw KebedeNo ratings yet

- Cost II-Ch - 3 Master BudgetDocument14 pagesCost II-Ch - 3 Master BudgetYitera SisayNo ratings yet

- Capital Budgeting IIDocument37 pagesCapital Budgeting IISelahi YılmazNo ratings yet

- Managerial Accounting IBPDocument58 pagesManagerial Accounting IBPSaadat Ali100% (1)

- Profit PlanningDocument5 pagesProfit PlanningChaudhry Umair YounisNo ratings yet

- Solution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 8Document44 pagesSolution Manual, Managerial Accounting Hansen Mowen 8th Editions - CH 8jasperkennedy083% (46)

- 1st Regular Session - ApprovedDocument22 pages1st Regular Session - ApprovedAllen HidalgoNo ratings yet

- Budgeting and Budgetary Control 2019Document10 pagesBudgeting and Budgetary Control 2019Kerrice RobinsonNo ratings yet

- Chapter 07 - BDocument40 pagesChapter 07 - BGedionNo ratings yet

- Chapter 07 - Planning For Profit and Cost ControlDocument60 pagesChapter 07 - Planning For Profit and Cost Controlruqayya muhammedNo ratings yet

- What Are The Basic Benefits and Purposes of DeveloDocument7 pagesWhat Are The Basic Benefits and Purposes of DeveloHenry L BanaagNo ratings yet

- Financial Planning and BudgetingDocument45 pagesFinancial Planning and BudgetingRafael BensigNo ratings yet

- CH 2 Cost IIDocument10 pagesCH 2 Cost IIfirewNo ratings yet

- Budgetary Planning GuideDocument13 pagesBudgetary Planning Guideyana kiutNo ratings yet

- Akmen Bab 8Document3 pagesAkmen Bab 8Hafizh GalihNo ratings yet

- Ch.13 Managing Small Business FinanceDocument5 pagesCh.13 Managing Small Business FinanceBaesick MoviesNo ratings yet

- Bases de CostosDocument13 pagesBases de CostosNohemi LopezNo ratings yet

- Original 1436552353 VICTORIA ProjectDocument12 pagesOriginal 1436552353 VICTORIA ProjectShashank SharanNo ratings yet

- Brewer6ce WYRNTK Ch07Document5 pagesBrewer6ce WYRNTK Ch07Bilal ShahidNo ratings yet

- MANAGING SMALL WPS OfficeDocument6 pagesMANAGING SMALL WPS Officecristine beaNo ratings yet

- Responsibility Accounting: Keval Patel ID - S32883Document14 pagesResponsibility Accounting: Keval Patel ID - S32883raj ramukNo ratings yet

- Bsbfim601 Manage FinancesDocument18 pagesBsbfim601 Manage FinancesJoanne Navarro AlmeriaNo ratings yet

- Managerial Accounting Asiacareer College/Cparcenter Operational and Financial Budgeting DWM - Reyno, Cpa, DbaDocument3 pagesManagerial Accounting Asiacareer College/Cparcenter Operational and Financial Budgeting DWM - Reyno, Cpa, DbaCertified Public AccountantNo ratings yet

- Management AccountingDocument8 pagesManagement AccountingAKSHAY KATARENo ratings yet

- Fiscal Management WF Dr. Emerita R. Alias Edgar Roy M. Curammeng Financial Forecasting, Corporate Planning and BudgetingDocument10 pagesFiscal Management WF Dr. Emerita R. Alias Edgar Roy M. Curammeng Financial Forecasting, Corporate Planning and BudgetingJeannelyn CondeNo ratings yet

- Financial Forecasting, Corporate Planning and BudgetingDocument6 pagesFinancial Forecasting, Corporate Planning and BudgetingAdoree RamosNo ratings yet

- Actual Activities of A Firm.: Answers To Study Questions For Chapter 8Document4 pagesActual Activities of A Firm.: Answers To Study Questions For Chapter 8Louie De La TorreNo ratings yet

- SHS Business Finance Chapter 3Document17 pagesSHS Business Finance Chapter 3Ji BaltazarNo ratings yet

- Chapter 07Document92 pagesChapter 07milkie beigeNo ratings yet

- Business Finance: 1 Quarter Lesson 3: Financial Planning ProcessDocument6 pagesBusiness Finance: 1 Quarter Lesson 3: Financial Planning ProcessReshaNo ratings yet

- Financial Planning and Budgeting GuideDocument29 pagesFinancial Planning and Budgeting GuidejsemlpzNo ratings yet

- Budgeting: Solutions To QuestionsDocument64 pagesBudgeting: Solutions To Questionsمصطفى العادليNo ratings yet

- Lecture 11 BIS ManagerialDocument25 pagesLecture 11 BIS Managerialnada ahmedNo ratings yet

- Budgeting CycleDocument4 pagesBudgeting CycleAhsaan KhanNo ratings yet

- Master Budgeting OutlineDocument14 pagesMaster Budgeting OutlineGina Mantos GocotanoNo ratings yet

- Chapter 6Document8 pagesChapter 6Rohit BadgujarNo ratings yet

- Section - A 201: (I) Discuss About Accounting PrinciplesDocument7 pagesSection - A 201: (I) Discuss About Accounting PrinciplesPrem KumarNo ratings yet

- Master Budget Components and UsesDocument10 pagesMaster Budget Components and UsesNur Athirah Binti MahdirNo ratings yet

- What Is a Budget? GuideDocument7 pagesWhat Is a Budget? GuideMichaelNo ratings yet

- Business Finance For Video Module 2Document16 pagesBusiness Finance For Video Module 2Bai NiloNo ratings yet

- Financial Management 2iu3hudihDocument10 pagesFinancial Management 2iu3hudihNageshwar singhNo ratings yet

- HanduotDocument20 pagesHanduotTegene TesfayeNo ratings yet

- Class Notes CH21Document17 pagesClass Notes CH21KamauWafulaWanyamaNo ratings yet

- Technological University of The Philippines: Ayala Boulevard, Ermita, Manila College of Industrial TechnologyDocument17 pagesTechnological University of The Philippines: Ayala Boulevard, Ermita, Manila College of Industrial Technologylorina p del rosarioNo ratings yet

- Chapter 07Document92 pagesChapter 07nguyenminhduong313No ratings yet

- CH - 2 Master Budget - Ahmed With Illustration and SolutionDocument15 pagesCH - 2 Master Budget - Ahmed With Illustration and SolutionYohannes MeridNo ratings yet

- Report No. 6 Batoy Khey Heart N. Matano Naffy BDocument35 pagesReport No. 6 Batoy Khey Heart N. Matano Naffy BCamille EscoteNo ratings yet

- Chm1 PPT SlidesDocument15 pagesChm1 PPT Slidesgilli1tr100% (1)

- Managerial AccountingDocument17 pagesManagerial Accountinggilli1tr100% (1)

- Financial Accounting 7th EditionDocument9 pagesFinancial Accounting 7th Editiongilli1trNo ratings yet

- Chapter 12 - Check Figures To 24-53Document4 pagesChapter 12 - Check Figures To 24-53gilli1trNo ratings yet

- Chap08 Extra Challenge ExercisesDocument7 pagesChap08 Extra Challenge Exercisesgilli1trNo ratings yet

- Financial Accounting 7th EditionDocument6 pagesFinancial Accounting 7th Editiongilli1trNo ratings yet

- Chap06 Extra Challange ExercisesDocument8 pagesChap06 Extra Challange Exercisesgilli1trNo ratings yet

- Financial Accounting 7th EditionDocument4 pagesFinancial Accounting 7th Editiongilli1trNo ratings yet

- Financial Accounting 7th EditionDocument5 pagesFinancial Accounting 7th Editiongilli1tr100% (1)

- Financial Accounting 7th EditionDocument8 pagesFinancial Accounting 7th Editiongilli1trNo ratings yet

- Financial Accounting 7th EditionDocument7 pagesFinancial Accounting 7th Editiongilli1tr100% (1)

- Financial Accounting 7th EditionDocument9 pagesFinancial Accounting 7th Editiongilli1trNo ratings yet

- Financial Accounting 7th EditionDocument3 pagesFinancial Accounting 7th Editiongilli1trNo ratings yet

- Southwest Airlines Case - Chap. 06Document11 pagesSouthwest Airlines Case - Chap. 06gilli1trNo ratings yet

- Fundamental Financial Analysis and ReportingDocument6 pagesFundamental Financial Analysis and Reportinggilli1trNo ratings yet

- Fundamental Financial Analysis and ReportingDocument4 pagesFundamental Financial Analysis and Reportinggilli1trNo ratings yet

- Auditing Purchasing ProcessDocument57 pagesAuditing Purchasing Processgilli1tr100% (1)

- Global Investments PPT PresentationDocument48 pagesGlobal Investments PPT Presentationgilli1trNo ratings yet

- Auditing and Assurance Services - Ch02Document43 pagesAuditing and Assurance Services - Ch02gilli1tr33% (3)

- Governmental and Nonprofit Accounting Theory and PracticeDocument68 pagesGovernmental and Nonprofit Accounting Theory and Practicegilli1tr100% (2)

- Governmental and Nonprofit Accounting Theory and PracticeDocument68 pagesGovernmental and Nonprofit Accounting Theory and Practicegilli1tr100% (2)

- Auditing Inventory Management ProcessDocument51 pagesAuditing Inventory Management Processgilli1tr67% (3)

- Auditing and Assurance Services Chapter 8 MC QuestionsDocument6 pagesAuditing and Assurance Services Chapter 8 MC Questionsgilli1trNo ratings yet

- Auditing and Assurance ServicesDocument65 pagesAuditing and Assurance Servicesgilli1tr67% (3)

- Auditing and Assurance ServicesDocument69 pagesAuditing and Assurance Servicesgilli1tr100% (1)

- Auditing and Assurance ServicesDocument49 pagesAuditing and Assurance Servicesgilli1tr100% (1)

- Accounting for Investments in SubsidiariesDocument7 pagesAccounting for Investments in Subsidiariesgilli1trNo ratings yet

- Chapter 8 - Debt Service Funds Solutions ManualDocument30 pagesChapter 8 - Debt Service Funds Solutions Manualgilli1trNo ratings yet

- Auditing and Assurance Chapter 14 MC QuestionsDocument9 pagesAuditing and Assurance Chapter 14 MC Questionsgilli1tr0% (1)

- Approaches in Estimating National Income (Group 4)Document6 pagesApproaches in Estimating National Income (Group 4)Yella Mae Pariña RelosNo ratings yet

- Ontario Reader 1998 AKDocument2 pagesOntario Reader 1998 AKDeaf CanuckNo ratings yet

- 06 Budgeting Theory 40Document4 pages06 Budgeting Theory 40Agnes DizonNo ratings yet

- NTU SSS Economics Tutorial ConsumptionDocument4 pagesNTU SSS Economics Tutorial ConsumptionMeena KmNo ratings yet

- Department of Labor: lm3 BlankformDocument5 pagesDepartment of Labor: lm3 BlankformUSA_DepartmentOfLabor100% (6)

- Ch12 Planning For Capital InvestmentsDocument62 pagesCh12 Planning For Capital Investmentsعبدالله ماجد المطارنهNo ratings yet

- Finance Process FlowDocument13 pagesFinance Process FlowHasan NasirNo ratings yet

- Carta Del Conservatorio de Música A La JuntaDocument2 pagesCarta Del Conservatorio de Música A La JuntaEl Nuevo DíaNo ratings yet

- MaaDocument2 pagesMaaSiva SankariNo ratings yet

- Master's Thesis - Factors Affecting Theatrical Success of Films: An Empirical ReviewDocument45 pagesMaster's Thesis - Factors Affecting Theatrical Success of Films: An Empirical Reviewsiddharth_uNo ratings yet

- Delegation of Financial Powers Rules-2022Document78 pagesDelegation of Financial Powers Rules-2022SAYAN BHATTANo ratings yet

- JulyDocument10 pagesJulyJan GarmanNo ratings yet

- Personal Budget Spreadsheet for Annual PlanningDocument5 pagesPersonal Budget Spreadsheet for Annual PlanningAnonymous qRbPsLpuNNo ratings yet

- EVM Gold CardDocument1 pageEVM Gold Cardwalmart007No ratings yet

- 5-Year Strategic PlanDocument53 pages5-Year Strategic PlanGere TassewNo ratings yet

- Jay Kusler-ResumeDocument4 pagesJay Kusler-Resumeapi-403638887No ratings yet

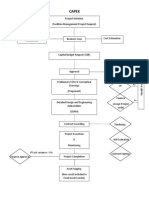

- CAPEXDocument1 pageCAPEXAmal KaNo ratings yet

- CA FINAL AMA Nov 14 Guideline Answers 15.11.2014Document16 pagesCA FINAL AMA Nov 14 Guideline Answers 15.11.2014Prateek MadaanNo ratings yet

- Management AccountingDocument13 pagesManagement AccountingEricka BautistaNo ratings yet

- International Economics 6Th Edition James Gerber Solutions Manual Full Chapter PDFDocument27 pagesInternational Economics 6Th Edition James Gerber Solutions Manual Full Chapter PDFRebeccaBartlettqfam100% (6)

- Kaplan 1988 - One Cost System Isn't EnoughDocument13 pagesKaplan 1988 - One Cost System Isn't EnoughSanjeev RanjanNo ratings yet

- BudgetDocument3 pagesBudgetkawalkaurNo ratings yet

- Financial LiteracyDocument2 pagesFinancial LiteracyLeocila EdangNo ratings yet

- Budget Analysis ReportDocument7 pagesBudget Analysis ReportRahul KumarNo ratings yet

- The City of Calgary 2020 Annual ReportDocument104 pagesThe City of Calgary 2020 Annual ReportAdam ToyNo ratings yet