You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- Case 2 Template For Brookstone OB - Gyn - CompleteDocument9 pagesCase 2 Template For Brookstone OB - Gyn - Completeaklank_218105100% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- 5 7Document2 pages5 7aklank_218105100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- IRS Form SS-4 Guide and InstructionsDocument7 pagesIRS Form SS-4 Guide and InstructionsChristopher WhoKnows100% (3)

- Nedbank Pricing 2020Document55 pagesNedbank Pricing 2020BusinessTech100% (1)

- Running Head: Financial Accounting ManagementDocument7 pagesRunning Head: Financial Accounting Managementaklank_218105No ratings yet

- IE 3265 Production & Operations Planning: Ch. 3 - Aggregate Planning R. Lindeke UMDDocument43 pagesIE 3265 Production & Operations Planning: Ch. 3 - Aggregate Planning R. Lindeke UMDaklank_218105No ratings yet

- Personal investment planning module 11 assignmentDocument1 pagePersonal investment planning module 11 assignmentaklank_218105No ratings yet

- Research Methodology Question BankDocument60 pagesResearch Methodology Question BankMohammed AadilNo ratings yet

- Geometric mean indicates average returns over timeDocument3 pagesGeometric mean indicates average returns over timeaklank_218105No ratings yet

- RequiredDocument1 pageRequiredaklank_218105No ratings yet

- Ratio AnalysisDocument11 pagesRatio Analysisaklank_218105No ratings yet

- Assignment #1 Solution (Chapters 3 and 5)Document5 pagesAssignment #1 Solution (Chapters 3 and 5)aklank_218105No ratings yet

- Raven Manufacturing CompanyDocument4 pagesRaven Manufacturing Companyaklank_218105No ratings yet

- RequiredDocument2 pagesRequiredaklank_218105No ratings yet

- Cash Flows From Operating ActivitiesDocument1 pageCash Flows From Operating Activitiesaklank_218105No ratings yet

- RequiredDocument1 pageRequiredaklank_218105No ratings yet

- Shca20 eDocument6 pagesShca20 eaklank_218105No ratings yet

- Acct 323Document1 pageAcct 323aklank_218105No ratings yet

- Name Surname MSFT RatiosDocument64 pagesName Surname MSFT Ratiosaklank_218105No ratings yet

- Gutierrez CompanyDocument1 pageGutierrez Companyaklank_218105No ratings yet

- BSNL Receipt - 888901413137Document1 pageBSNL Receipt - 888901413137aklank_218105No ratings yet

- BSNL Receipt - 888905452002 - Jun14Document1 pageBSNL Receipt - 888905452002 - Jun14aklank_218105No ratings yet

- Week 4 HomeworkDocument4 pagesWeek 4 Homeworkaklank_218105No ratings yet

- Project 1Document6 pagesProject 1aklank_218105No ratings yet

- Assignment 1Document5 pagesAssignment 1aklank_218105No ratings yet

- CSMN Factsheet 1Q15 - X-LinksDocument2 pagesCSMN Factsheet 1Q15 - X-Linksaklank_218105No ratings yet

- Week Nine Assignment - 0001Document1 pageWeek Nine Assignment - 0001aklank_218105No ratings yet

- Index Movements: Index Based Graphical RepresentationDocument1 pageIndex Movements: Index Based Graphical Representationaklank_218105No ratings yet

- FCFI FactSheet FINAL 6 1 15Document2 pagesFCFI FactSheet FINAL 6 1 15aklank_218105No ratings yet

- Mansarover Home Elecrticty Bill Receipt - OnlinePayment - Dec14Document1 pageMansarover Home Elecrticty Bill Receipt - OnlinePayment - Dec14aklank_218105No ratings yet

- SolutionDocument1 pageSolutionaklank_218105No ratings yet

- BSNL - Pay Landline Bills - JanDocument1 pageBSNL - Pay Landline Bills - Janaklank_218105No ratings yet

- INV2001082Document1 pageINV2001082Bisi AgomoNo ratings yet

- The Nairobi Stock Exchange (NSE) Sectors ReconfiguredDocument5 pagesThe Nairobi Stock Exchange (NSE) Sectors ReconfiguredPatrick Kiragu Mwangi BA, BSc., MA, ACSINo ratings yet

- t8. Money Growth and InflationDocument53 pagest8. Money Growth and Inflationmimi96No ratings yet

- Top 12 Webinars Traders Should Watch To Learn About Technical AnalysisDocument15 pagesTop 12 Webinars Traders Should Watch To Learn About Technical Analysiswolf1No ratings yet

- Final Exam/2: Multiple ChoiceDocument4 pagesFinal Exam/2: Multiple ChoiceJing SongNo ratings yet

- Analyzation of Robinson's Clan's Three Months TransactionsDocument4 pagesAnalyzation of Robinson's Clan's Three Months TransactionsNoralyn de SilvaNo ratings yet

- Principles of Financial Accounting 12th Edition Needles Solutions ManualDocument25 pagesPrinciples of Financial Accounting 12th Edition Needles Solutions ManualJacquelineHillqtbs100% (54)

- Ark Israel Innovative Technology Etf Izrl HoldingsDocument2 pagesArk Israel Innovative Technology Etf Izrl HoldingsmikiNo ratings yet

- Chapter 16 - Management of Current AssetsDocument7 pagesChapter 16 - Management of Current Assetslou-924No ratings yet

- Capital Structure and Firm Efficiency: Dimitris Margaritis and Maria PsillakiDocument23 pagesCapital Structure and Firm Efficiency: Dimitris Margaritis and Maria PsillakiRafael G. MaciasNo ratings yet

- Finance Act 2021 - PWC Insight Series and Sector Analysis Interactive 2Document25 pagesFinance Act 2021 - PWC Insight Series and Sector Analysis Interactive 2Oyeleye TofunmiNo ratings yet

- Chapter 4 Recording of TransactiosDocument24 pagesChapter 4 Recording of TransactiosJohn Mark MaligaligNo ratings yet

- Paper 5-Financial Accounting: Answer To MTP - Intermediate - Syllabus 2012 - Dec2015 - Set 2Document22 pagesPaper 5-Financial Accounting: Answer To MTP - Intermediate - Syllabus 2012 - Dec2015 - Set 2AK Aru ShettyNo ratings yet

- Credit Card Statement SummaryDocument6 pagesCredit Card Statement SummaryLim Su PingNo ratings yet

- Registration flow and documentsDocument22 pagesRegistration flow and documentsmdzainiNo ratings yet

- Grade 7 Practice: Calculating Percent Changes and DiscountsDocument3 pagesGrade 7 Practice: Calculating Percent Changes and DiscountsRizky HermawanNo ratings yet

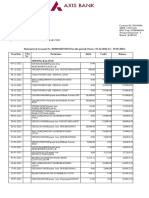

- Garima Axis Bank SDocument3 pagesGarima Axis Bank SSajan Sharma100% (1)

- Consolidated CSOFP of Jasin Bhd GroupDocument4 pagesConsolidated CSOFP of Jasin Bhd GroupNoor ShukirrahNo ratings yet

- Template Excel Pengantar AkuntansiiDocument15 pagesTemplate Excel Pengantar AkuntansiiKim SeokjinNo ratings yet

- OBLICON - Chapter 1 ProblemDocument1 pageOBLICON - Chapter 1 ProblemArahNo ratings yet

- Risk Management Strategies G2 - 20.3 (Final)Document4 pagesRisk Management Strategies G2 - 20.3 (Final)Phuong Anh NguyenNo ratings yet

- SATURDAYDocument20 pagesSATURDAYkristine bandaviaNo ratings yet

- Types of CapitalDocument24 pagesTypes of CapitalAnkita N VyasNo ratings yet

- Subramanian Cibil ReportDocument13 pagesSubramanian Cibil ReportManish KumarNo ratings yet

- Daily Current Affairs: 20 January 2024Document17 pagesDaily Current Affairs: 20 January 2024YASH PANDEYNo ratings yet

- ECB & Fed A Comparison A Comparison: International Summer ProgramDocument40 pagesECB & Fed A Comparison A Comparison: International Summer Programsabiha12No ratings yet

- Real Estate Presentation - Chapter 12Document27 pagesReal Estate Presentation - Chapter 12Cedric McCorkleNo ratings yet

- Educational Institution Tax Exemption CaseDocument1 pageEducational Institution Tax Exemption Casenil qawNo ratings yet