You might also like

- Strategic and Tactical Asset Allocation: An Integrated ApproachFrom EverandStrategic and Tactical Asset Allocation: An Integrated ApproachNo ratings yet

- Microscopic Simulation of Financial Markets: From Investor Behavior to Market PhenomenaFrom EverandMicroscopic Simulation of Financial Markets: From Investor Behavior to Market PhenomenaNo ratings yet

- A Dynamic Model of The Limit Order Book: Ioanid Ros UDocument41 pagesA Dynamic Model of The Limit Order Book: Ioanid Ros Upinokio504No ratings yet

- TradeDocument6 pagesTradekyleleefakeNo ratings yet

- 0082 A Multi-Factor Model For Energy DerivativesDocument20 pages0082 A Multi-Factor Model For Energy DerivativesOureo LiNo ratings yet

- Fama-Macbeth Two Stage Factor Premium EstimationDocument5 pagesFama-Macbeth Two Stage Factor Premium Estimationkty21joy100% (1)

- Enterprise Risk Analytics for Capital Markets: Proactive and Real-Time Risk ManagementFrom EverandEnterprise Risk Analytics for Capital Markets: Proactive and Real-Time Risk ManagementNo ratings yet

- From Implied To Spot Volatilities: Valdo DurrlemanDocument21 pagesFrom Implied To Spot Volatilities: Valdo DurrlemanginovainmonaNo ratings yet

- Deep HedgingDocument21 pagesDeep HedgingRaju KaliperumalNo ratings yet

- Factor Investing RevisedDocument22 pagesFactor Investing Revisedalexa_sherpyNo ratings yet

- Predictingvolatility LazardresearchDocument9 pagesPredictingvolatility Lazardresearchhc87No ratings yet

- Book of Greeks Edition 1.0 (Preview)Document80 pagesBook of Greeks Edition 1.0 (Preview)fporwrwerNo ratings yet

- Trading Baskets ImplementationDocument44 pagesTrading Baskets ImplementationSanchit Gupta100% (1)

- VIX Market Volatility Index and U.S. Stock ReturnsDocument14 pagesVIX Market Volatility Index and U.S. Stock Returnsmm1979No ratings yet

- Introduction To Fast Fourier Transform inDocument31 pagesIntroduction To Fast Fourier Transform inALNo ratings yet

- Cutting Edge Investment Views on Non-Normal MarketsDocument10 pagesCutting Edge Investment Views on Non-Normal MarketsRichard LindseyNo ratings yet

- Flow Chart For Quant StrategiesDocument1 pageFlow Chart For Quant StrategiesKaustubh KeskarNo ratings yet

- Bias in Measuring Effective Bid-Ask SpreadsDocument62 pagesBias in Measuring Effective Bid-Ask SpreadsLuca PilottiNo ratings yet

- Option Pricing and The Black - Scholes Model: A Lecture Note From Master's Level Teaching Perspective - Kapil Dev SubediDocument5 pagesOption Pricing and The Black - Scholes Model: A Lecture Note From Master's Level Teaching Perspective - Kapil Dev Subedikapildeb100% (1)

- Sabr SLVDocument21 pagesSabr SLVArturo ZamudioNo ratings yet

- Optimal Delta Hedging For OptionsDocument11 pagesOptimal Delta Hedging For OptionsSandeep LimbasiyaNo ratings yet

- Static Versus Dynamic Hedging of Exotic OptionsDocument29 pagesStatic Versus Dynamic Hedging of Exotic OptionsjustinlfangNo ratings yet

- IEOR E4630 Spring 2016 SyllabusDocument2 pagesIEOR E4630 Spring 2016 Syllabuscef4No ratings yet

- MS&E448: Statistical Arbitrage: Group 5: Carolyn Soo, Zhengyi Lian, Jiayu Lou, Hang YangDocument31 pagesMS&E448: Statistical Arbitrage: Group 5: Carolyn Soo, Zhengyi Lian, Jiayu Lou, Hang Yang123No ratings yet

- A Practical ImplementationOfHJMDocument336 pagesA Practical ImplementationOfHJMTom WuNo ratings yet

- Statistical Arbitrage Models of FTSE 100Document11 pagesStatistical Arbitrage Models of FTSE 100greg100% (20)

- Hans Buehler DissDocument164 pagesHans Buehler DissAgatha MurgociNo ratings yet

- DynamicVIXFuturesVersion2Rev1 PDFDocument19 pagesDynamicVIXFuturesVersion2Rev1 PDFsamuelcwlsonNo ratings yet

- A Simple and Reliable Way To Compute Option-Based Risk-Neutral DistributionsDocument42 pagesA Simple and Reliable Way To Compute Option-Based Risk-Neutral Distributionsalanpicard2303No ratings yet

- Option Pricing Under Power Laws A RobustDocument5 pagesOption Pricing Under Power Laws A RobustLucas D'AmelioNo ratings yet

- BLK Risk Factor Investing Revealed PDFDocument8 pagesBLK Risk Factor Investing Revealed PDFShaun RodriguezNo ratings yet

- The Swiss Army Knife of Options AnalyticsDocument4 pagesThe Swiss Army Knife of Options AnalyticsdanNo ratings yet

- Creditrisk Plus PDFDocument72 pagesCreditrisk Plus PDFNayeline CastilloNo ratings yet

- A Practical Guide To Volatility Forecasting Through Calm and StormDocument23 pagesA Practical Guide To Volatility Forecasting Through Calm and StormwillyNo ratings yet

- Jackel 2006 - ByImplication PDFDocument6 pagesJackel 2006 - ByImplication PDFpukkapadNo ratings yet

- Fed Funds Futures Probability Tree CalculatorDocument4 pagesFed Funds Futures Probability Tree CalculatorAlok Singh100% (1)

- Forecasting Government Bond Yields with Nelson-Siegel ModelDocument28 pagesForecasting Government Bond Yields with Nelson-Siegel Modelstan32lem32No ratings yet

- 215 Years of Global Multi-Asset Momentum: 1800-2014Document84 pages215 Years of Global Multi-Asset Momentum: 1800-2014superbuddyNo ratings yet

- Asset Lia Version of CAPmDocument21 pagesAsset Lia Version of CAPmkunal_sharma2811No ratings yet

- VIX SPX AnalysisDocument2 pagesVIX SPX Analysisberrypatch268096No ratings yet

- CBOT-Understanding BasisDocument26 pagesCBOT-Understanding BasisIshan SaneNo ratings yet

- Assignment Option Pricing ModelDocument28 pagesAssignment Option Pricing Modeleccentric123No ratings yet

- MarketMaking Models - SummaryDocument35 pagesMarketMaking Models - SummaryRemoCPINo ratings yet

- Pricing and Hedging Volatility Derivatives: Mark Broadie Ashish Jain January 10, 2008Document40 pagesPricing and Hedging Volatility Derivatives: Mark Broadie Ashish Jain January 10, 2008Aakash KhandelwalNo ratings yet

- Cutting Edge Dividend AdjustmentDocument2 pagesCutting Edge Dividend AdjustmentVeeken Chaglassian100% (1)

- Change Point DetectionDocument23 pagesChange Point DetectionSalbani ChakraborttyNo ratings yet

- Implied Vol Surface Parametrization PDFDocument40 pagesImplied Vol Surface Parametrization PDFsoumensahilNo ratings yet

- Diebold 2Document30 pagesDiebold 2fedegrassoNo ratings yet

- The Vol Smile Problem - FX FocusDocument5 pagesThe Vol Smile Problem - FX FocusVeeken ChaglassianNo ratings yet

- The Two-Factor Hull-White ModelDocument47 pagesThe Two-Factor Hull-White ModelALNo ratings yet

- Modeling Autocallable Structured ProductsDocument21 pagesModeling Autocallable Structured Productsjohan oldmanNo ratings yet

- OVME User Guide: Pricing Options and StrategiesDocument21 pagesOVME User Guide: Pricing Options and StrategiesRaphaël FromEverNo ratings yet

- Change of Measure in Midcurve Pricing Model Captures Correlation SkewDocument17 pagesChange of Measure in Midcurve Pricing Model Captures Correlation Skewchinicoco100% (1)

- Half-Day Reversal - QuantPediaDocument7 pagesHalf-Day Reversal - QuantPediaJames LiuNo ratings yet

- Value and Momentum EverywhereDocument58 pagesValue and Momentum EverywhereDessy ParamitaNo ratings yet

- Statistical Modelling of Financial Time Series - An IntroductionDocument41 pagesStatistical Modelling of Financial Time Series - An IntroductionKofi Appiah-Danquah100% (1)

- Princeton Financial Math PDFDocument46 pagesPrinceton Financial Math PDF6doitNo ratings yet

- The Value of Queue Position in A Limit Order BookDocument48 pagesThe Value of Queue Position in A Limit Order Bookadeka1100% (1)

- Factory Method .NET Design Pattern in C# and VB - DofactoryDocument10 pagesFactory Method .NET Design Pattern in C# and VB - DofactoryChun Ming Jeffy Tam100% (1)

- NSP Premia ManualDocument10 pagesNSP Premia ManualChun Ming Jeffy TamNo ratings yet

- Pjotr Iljitsch Tschaikowski SchwanenseeDocument173 pagesPjotr Iljitsch Tschaikowski Schwanenseewerner64No ratings yet

- Patrick Cheridito - Pricing and Hedging CoCos PDFDocument26 pagesPatrick Cheridito - Pricing and Hedging CoCos PDFChun Ming Jeffy TamNo ratings yet

- Dilip Madan - On Pricing Contingent Capital Notes PDFDocument24 pagesDilip Madan - On Pricing Contingent Capital Notes PDFChun Ming Jeffy TamNo ratings yet

- Ravel La Valse PianoDocument24 pagesRavel La Valse PianomusiquetrovaNo ratings yet

- UMC 0.000% 18-May-2020Document76 pagesUMC 0.000% 18-May-2020Chun Ming Jeffy TamNo ratings yet

- Phil Hunt, Joanne Kennedy, Antoon Pelsser - Markov-Functional Interest Rate Models PDFDocument18 pagesPhil Hunt, Joanne Kennedy, Antoon Pelsser - Markov-Functional Interest Rate Models PDFChun Ming Jeffy TamNo ratings yet

- Tribute Concert Honors Rosalyn Tureck's Bach Legacy at Lincoln CenterDocument12 pagesTribute Concert Honors Rosalyn Tureck's Bach Legacy at Lincoln CenterChun Ming Jeffy TamNo ratings yet

- F&s BGKDocument28 pagesF&s BGKChun Ming Jeffy TamNo ratings yet

- T.E. Duncan - Prediction For Some Processes Related To A Fractional Brownian MotionDocument7 pagesT.E. Duncan - Prediction For Some Processes Related To A Fractional Brownian MotionChun Ming Jeffy TamNo ratings yet

- DuffiePanSingleton Jumps Econometrica 00 PDFDocument34 pagesDuffiePanSingleton Jumps Econometrica 00 PDFChun Ming Jeffy TamNo ratings yet

- Simona Svoboda - Libor Market Model With Stochastic Volatility PDFDocument66 pagesSimona Svoboda - Libor Market Model With Stochastic Volatility PDFChun Ming Jeffy TamNo ratings yet

- Comment On Pricing Double Barrier Options Using Comment On 'Laplace Transforms' by Antoon Pelsser PDFDocument3 pagesComment On Pricing Double Barrier Options Using Comment On 'Laplace Transforms' by Antoon Pelsser PDFChun Ming Jeffy TamNo ratings yet

- Duffie - AFFINE PROCESSES AND APPLICATIONS IN FINANCE PDFDocument59 pagesDuffie - AFFINE PROCESSES AND APPLICATIONS IN FINANCE PDFChun Ming Jeffy TamNo ratings yet

- Paul Glasserman - Numerical Solution of Jump-Diffusion LIBOR Market Models PDFDocument27 pagesPaul Glasserman - Numerical Solution of Jump-Diffusion LIBOR Market Models PDFChun Ming Jeffy TamNo ratings yet

- David Lando - Cox Process and Risky Securities PDFDocument22 pagesDavid Lando - Cox Process and Risky Securities PDFChun Ming Jeffy TamNo ratings yet

- C.H. Hui - Using First-Passage-Time Density To Assess Realignment Risk of A Target Zone PDFDocument24 pagesC.H. Hui - Using First-Passage-Time Density To Assess Realignment Risk of A Target Zone PDFChun Ming Jeffy TamNo ratings yet

- Philip Stahl, Philipp B Rindler - Robust Calculation of MFIV From Calibrated Surface PDFDocument20 pagesPhilip Stahl, Philipp B Rindler - Robust Calculation of MFIV From Calibrated Surface PDFChun Ming Jeffy TamNo ratings yet

- Simulation of FBM Thesis NL PDFDocument77 pagesSimulation of FBM Thesis NL PDFChun Ming Jeffy TamNo ratings yet

- Robert Jarrow - Smiles - JF - 07 PDFDocument38 pagesRobert Jarrow - Smiles - JF - 07 PDFChun Ming Jeffy TamNo ratings yet

- Antoon Pelsser - Pricing Double Barrier Options Using Laplace Transforms PDFDocument10 pagesAntoon Pelsser - Pricing Double Barrier Options Using Laplace Transforms PDFChun Ming Jeffy TamNo ratings yet

- Robert Elliott - Pricing Volatility Swap and Variance Swap Under Heston Model With Regime Switching PDFDocument46 pagesRobert Elliott - Pricing Volatility Swap and Variance Swap Under Heston Model With Regime Switching PDFChun Ming Jeffy TamNo ratings yet

- Paul Glasserman - Saddlepoint Approximations For Affine Jump-Diffusion Models PDFDocument35 pagesPaul Glasserman - Saddlepoint Approximations For Affine Jump-Diffusion Models PDFChun Ming Jeffy TamNo ratings yet

- Print - Lesson 6 - Multivariate Conditional Distribution and Partial Correlation PDFDocument11 pagesPrint - Lesson 6 - Multivariate Conditional Distribution and Partial Correlation PDFChun Ming Jeffy TamNo ratings yet

- Patrice Abry, Fabrice Sellan - The Wavelet-Based Synthesis For Fractional Brownian Motion PDFDocument7 pagesPatrice Abry, Fabrice Sellan - The Wavelet-Based Synthesis For Fractional Brownian Motion PDFChun Ming Jeffy TamNo ratings yet

- Pitman Estimators NovikovKord June 30 2012 Final 15 EngSW PDFDocument10 pagesPitman Estimators NovikovKord June 30 2012 Final 15 EngSW PDFChun Ming Jeffy TamNo ratings yet

- Nathanael Enriquez - A Simple Construction of The Fractional Brownian Motion PDFDocument21 pagesNathanael Enriquez - A Simple Construction of The Fractional Brownian Motion PDFChun Ming Jeffy TamNo ratings yet

- Paul Glasserman - Malliavin Greeks Without Malliavin Calculus PDFDocument35 pagesPaul Glasserman - Malliavin Greeks Without Malliavin Calculus PDFChun Ming Jeffy TamNo ratings yet

- Leif Andersen - Extended Libor Market Models With Stochastic Volatility PDFDocument43 pagesLeif Andersen - Extended Libor Market Models With Stochastic Volatility PDFChun Ming Jeffy TamNo ratings yet

- Dynamic Trend Trading The SystemDocument151 pagesDynamic Trend Trading The Systemmangelbel674988% (26)

- Acctg 4 Quiz 3 Debt Restructuring Payables 1Document11 pagesAcctg 4 Quiz 3 Debt Restructuring Payables 1Competente, Jhonna W.No ratings yet

- Chapter 3 Beams 13ed RevisedDocument31 pagesChapter 3 Beams 13ed RevisedEvan AnwariNo ratings yet

- Daftar Nama Akun PT JayatamaDocument2 pagesDaftar Nama Akun PT Jayatamastriii906No ratings yet

- How To Spot 90% Winners Instantly With Nothing More Than A Hand-Held Calculator, Don Fishback 2012Document4 pagesHow To Spot 90% Winners Instantly With Nothing More Than A Hand-Held Calculator, Don Fishback 2012Rakesh Jain100% (1)

- Up Chapter 6-7 (1) - 2 (Compatibility Mode)Document39 pagesUp Chapter 6-7 (1) - 2 (Compatibility Mode)EftaNo ratings yet

- Cfap6 Audit Past Papers and AnswersDocument148 pagesCfap6 Audit Past Papers and AnswersZareen AbbasNo ratings yet

- SecAB, Assignment#4, Rebecca HamiltonDocument11 pagesSecAB, Assignment#4, Rebecca HamiltonBeccaNo ratings yet

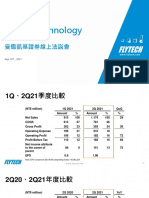

- Flytech TechnologyDocument7 pagesFlytech TechnologyLouis ChenNo ratings yet

- Corporate finance project on Hindustan UnileverDocument20 pagesCorporate finance project on Hindustan UnileverAnkit Jaiswal0% (1)

- Forecasting Exchange Rates 1Document32 pagesForecasting Exchange Rates 1Afrianto Budi Aan100% (1)

- Note On Public IssueDocument9 pagesNote On Public IssueKrish KalraNo ratings yet

- Laporan Keuangan Konsolidasian Q3 DPNSDocument105 pagesLaporan Keuangan Konsolidasian Q3 DPNSSyaifudin ZauhariNo ratings yet

- Corporate Banking 1Document34 pagesCorporate Banking 1Pravah ShuklaNo ratings yet

- Accounting Assignment: Company Name:-Bajaj AutoDocument5 pagesAccounting Assignment: Company Name:-Bajaj Autonand bhushanNo ratings yet

- Home LK TW I 2015Document57 pagesHome LK TW I 2015Lucky PermanaNo ratings yet

- Inferior Investment Alternatives What Will Be The ExpectedDocument1 pageInferior Investment Alternatives What Will Be The ExpectedM Bilal SaleemNo ratings yet

- 597 PDFsam 290120 CUDocument197 pages597 PDFsam 290120 CUSomenath PaulNo ratings yet

- DMU ACFN Model ExamDocument17 pagesDMU ACFN Model Examkassahunabate3717No ratings yet

- David Einhorn's Greenlight Capital Q3 LetterDocument5 pagesDavid Einhorn's Greenlight Capital Q3 Lettermarketfolly.com100% (1)

- First Semester Business English Exams Agenla 2016-2017 Level II AccountingDocument2 pagesFirst Semester Business English Exams Agenla 2016-2017 Level II AccountingLysongo OruNo ratings yet

- Annual-Report-2020 FKSDocument12 pagesAnnual-Report-2020 FKSHalizasnNo ratings yet

- Book 1 - Foundations of Risk Management PDFDocument19 pagesBook 1 - Foundations of Risk Management PDFmohamed0% (1)

- Add Bab 11 PDFDocument44 pagesAdd Bab 11 PDFdiana sartikaNo ratings yet

- PG Diploma in Securities - Introduction to Capital Markets & Securities Law MCQsDocument9 pagesPG Diploma in Securities - Introduction to Capital Markets & Securities Law MCQsAnandNo ratings yet

- Quiz 1 Solution Chapter 1 and 3Document9 pagesQuiz 1 Solution Chapter 1 and 3Saadat ShaikhNo ratings yet

- Issues:: - Ashish Kumar Chauhan, Vice-President, National Stock Exchange (NSE)Document3 pagesIssues:: - Ashish Kumar Chauhan, Vice-President, National Stock Exchange (NSE)Bhupendra ChauhanNo ratings yet

- IFS - B.com End Sem. Que. Paper PDFDocument4 pagesIFS - B.com End Sem. Que. Paper PDFpranav2411No ratings yet

- Essentials of Corporate Finance Australian 3rd Edition Ross Solutions ManualDocument34 pagesEssentials of Corporate Finance Australian 3rd Edition Ross Solutions Manualupwindscatterf9ebp100% (28)

- Radio OneDocument1 pageRadio OneTommy Choi100% (1)