You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- MBFI Quiz KeyDocument7 pagesMBFI Quiz Keypunitha_pNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Partial Discharge Diagnostic Testing and Monitoring Solutions For High Voltage CablesDocument55 pagesPartial Discharge Diagnostic Testing and Monitoring Solutions For High Voltage CablesElsan BalucanNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Workbook, Exercises-Unit 8Document6 pagesWorkbook, Exercises-Unit 8Melanie ValdezNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Pat Lintas Minat Bahasa Inggris Kelas XDocument16 pagesPat Lintas Minat Bahasa Inggris Kelas XEka MurniatiNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Hyundai Monitor ManualDocument26 pagesHyundai Monitor ManualSamNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- IT Quiz QuestionsDocument10 pagesIT Quiz QuestionsbrittosabuNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

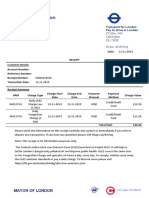

- Transport For London Pay To Drive in London: PO Box 344 Darlington Dl1 9qe TFL - Gov.uk/drivingDocument1 pageTransport For London Pay To Drive in London: PO Box 344 Darlington Dl1 9qe TFL - Gov.uk/drivingDanyy MaciucNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- NHS FPX 5004 Assessment 4 Self-Assessment of Leadership, Collaboration, and EthicsDocument4 pagesNHS FPX 5004 Assessment 4 Self-Assessment of Leadership, Collaboration, and EthicsEmma WatsonNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Misurata UniversityDocument11 pagesMisurata UniversityDustin EllisNo ratings yet

- Experiment No 9 - Part1Document38 pagesExperiment No 9 - Part1Nipun GosaiNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Duraguard MsdsDocument1 pageDuraguard MsdsSantosh Kumar GoudaNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- MBA CurriculumDocument93 pagesMBA CurriculumkaranNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- LeasesDocument9 pagesLeasesCris Joy BiabasNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Mechanical FPD P.sanchezDocument9 pagesMechanical FPD P.sanchezHailley DensonNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- TelekomDocument2 pagesTelekomAnonymous eS7MLJvPZCNo ratings yet

- MCQ (Chapter 6)Document4 pagesMCQ (Chapter 6)trail meNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Philippine Forest Facts and Figures PDFDocument34 pagesPhilippine Forest Facts and Figures PDFPamela L. FallerNo ratings yet

- Sustainable Project Management. The GPM Reference Guide: March 2018Document26 pagesSustainable Project Management. The GPM Reference Guide: March 2018Carlos Andres PinzonNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Submersible Sewage Ejector Pump: Pump Installation and Service ManualDocument8 pagesSubmersible Sewage Ejector Pump: Pump Installation and Service Manualallen_worstNo ratings yet

- Brand Plan - SingulairDocument11 pagesBrand Plan - Singulairshashank100% (2)

- Tran Date Value Date Tran Particular Credit Debit BalanceDocument96 pagesTran Date Value Date Tran Particular Credit Debit BalanceGenji MaNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Unix Training ContentDocument5 pagesUnix Training ContentsathishkumarNo ratings yet

- Persuasion 101Document19 pagesPersuasion 101gnmantel0% (1)

- 2012 Brochure Keltan Final en PDFDocument20 pages2012 Brochure Keltan Final en PDFJorge Zegarra100% (1)

- Sales Force TrainingDocument18 pagesSales Force Trainingsaurabh shekhar100% (2)

- Archer AX53 (EU) 1.0 - DatasheetDocument7 pagesArcher AX53 (EU) 1.0 - DatasheetLucNo ratings yet

- QP02Document11 pagesQP02zakwanmustafa0% (1)

- ET275 Unit 2 - Lesson Plan - SlidesDocument27 pagesET275 Unit 2 - Lesson Plan - SlidesDonald LeedyNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Dump Truck TBTDocument1 pageDump Truck TBTLiaquat MuhammadNo ratings yet

- New CVLRDocument2 pagesNew CVLRanahata2014No ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)