You might also like

- PHD DissertationDocument14 pagesPHD DissertationShito Ryu100% (1)

- OFTC Lesson 18 - Integrating Order Flow With Traditional Technical AnalysisDocument34 pagesOFTC Lesson 18 - Integrating Order Flow With Traditional Technical AnalysisThanhdat VoNo ratings yet

- Targeting Israeli Apartheid A Boycott Divestment and Sanctions Handbook.Document383 pagesTargeting Israeli Apartheid A Boycott Divestment and Sanctions Handbook.john_edmonstoneNo ratings yet

- Amara Raja Batteries - Initiating Coverage ICICIdirectDocument25 pagesAmara Raja Batteries - Initiating Coverage ICICIdirectanandvisNo ratings yet

- An Overview of Hemp Fibre PDFDocument4 pagesAn Overview of Hemp Fibre PDFscribbddNo ratings yet

- Inventory Assignment 2 PDFDocument10 pagesInventory Assignment 2 PDFMuhammad Naveed IkramNo ratings yet

- PepsiCo GRCDocument4 pagesPepsiCo GRCessamsha3banNo ratings yet

- How To Read The Annual Report of A Company - Varsity by ZerodhaDocument25 pagesHow To Read The Annual Report of A Company - Varsity by Zerodhashekhar0050% (1)

- MBA Project Listing on Printing ServicesDocument51 pagesMBA Project Listing on Printing ServicesDevrajNo ratings yet

- Property InvestmentDocument69 pagesProperty InvestmentEshantha Samarajiwa100% (1)

- Energy Efficiency in South Asia: Opportunities for Energy Sector TransformationFrom EverandEnergy Efficiency in South Asia: Opportunities for Energy Sector TransformationNo ratings yet

- Financial Statements and Ratio Analysis: ChapterDocument25 pagesFinancial Statements and Ratio Analysis: Chapterkarim67% (3)

- Kunci Kuis AKL 2Document9 pagesKunci Kuis AKL 2Ilham Dwi NoviantoNo ratings yet

- Tyre Factories in IndiaDocument47 pagesTyre Factories in IndiaKedar Kulkarni0% (1)

- Activitiy Plan - QM - 2 Dec 2018Document1 pageActivitiy Plan - QM - 2 Dec 2018rmdarisaNo ratings yet

- (Food Processing) Milk Dairy Sector, Supply Chain, Upstream Downstream Issues, Amul Model, Operation Flood MrunalDocument13 pages(Food Processing) Milk Dairy Sector, Supply Chain, Upstream Downstream Issues, Amul Model, Operation Flood Mrunalrajendrashekhawat123No ratings yet

- Contract Farming in Gujarat PanwarDocument20 pagesContract Farming in Gujarat Panwarpanwarrca100% (2)

- Lube Study Report - MumbaiDocument11 pagesLube Study Report - Mumbaivinod kumarNo ratings yet

- Cpri Vision 2050Document39 pagesCpri Vision 2050swatijoshi_niam08No ratings yet

- Abstarct BFT 2015Document191 pagesAbstarct BFT 2015RohitMishraNo ratings yet

- Overview of Contract Farming in Thailand: Lessons Learned: Songsak Sriboonchitta and Aree WiboonpoongseDocument21 pagesOverview of Contract Farming in Thailand: Lessons Learned: Songsak Sriboonchitta and Aree WiboonpoongseKogree Kyaw Win OoNo ratings yet

- AFM Model Test PaperDocument16 pagesAFM Model Test PaperNeelu AhluwaliaNo ratings yet

- ElasticityDocument5 pagesElasticityMike WooddellNo ratings yet

- Types of Contract FarmingDocument14 pagesTypes of Contract Farmingtacamp daNo ratings yet

- Vivekananda Suaro IIM KozhikodeDocument13 pagesVivekananda Suaro IIM KozhikodevivekNo ratings yet

- NCERT Solutions Class 12 Chemistry Chapter 1 Solid StateDocument17 pagesNCERT Solutions Class 12 Chemistry Chapter 1 Solid StateVidyakulNo ratings yet

- Appex Corporation: Executive SummaryDocument4 pagesAppex Corporation: Executive SummaryAfiaSiddiqui100% (1)

- Prospects for Potato Processing and Export in BangladeshDocument17 pagesProspects for Potato Processing and Export in BangladeshSohel Khan0% (1)

- Dairy ScienceDocument3 pagesDairy ScienceRizwan AliNo ratings yet

- Sop Lays Feritos Sonia CompleteDocument1 pageSop Lays Feritos Sonia CompleteSONIA NABI0% (1)

- LSS Unit 1Document75 pagesLSS Unit 1Kamal KannanNo ratings yet

- Vermicomposting Biotechnology An Ecoloving Approach For Recycling of Solid Organic Wastes Into Valuable Biofertilizers 2155 6202.1000113 PDFDocument8 pagesVermicomposting Biotechnology An Ecoloving Approach For Recycling of Solid Organic Wastes Into Valuable Biofertilizers 2155 6202.1000113 PDFShopShort RoadNo ratings yet

- Factors That Affect Your Bike's Fuel EfficiencyDocument8 pagesFactors That Affect Your Bike's Fuel Efficiencynonu740No ratings yet

- Alternative Choices and DecisionsDocument29 pagesAlternative Choices and DecisionsAman BansalNo ratings yet

- Cvsandeepkumarshivhare Iimrohtak Consultinggeneralmanagement 4yearsexp 131108062109 Phpapp02 PDFDocument2 pagesCvsandeepkumarshivhare Iimrohtak Consultinggeneralmanagement 4yearsexp 131108062109 Phpapp02 PDFSai Swaroop MandalNo ratings yet

- Manual Mother DairyDocument89 pagesManual Mother DairyFahimNo ratings yet

- Coping with COVID-19: Impact on workforce and future of workDocument2 pagesCoping with COVID-19: Impact on workforce and future of workUnnikrishnan SNo ratings yet

- Saras DairyDocument53 pagesSaras DairyPallav SinghNo ratings yet

- Operation Theory AnswerDocument2 pagesOperation Theory AnswerMeenakshi sundhiNo ratings yet

- 300621-Sbi Ar 2021Document306 pages300621-Sbi Ar 2021manojNo ratings yet

- E4-E5 - PPT - Chapter 5.restructuring and Responsibility MatrixDocument21 pagesE4-E5 - PPT - Chapter 5.restructuring and Responsibility MatrixSanjay KumarNo ratings yet

- Cost Accounting Final ProjectDocument12 pagesCost Accounting Final ProjectJawad1997No ratings yet

- Frito Lay's PaperDocument9 pagesFrito Lay's Paperpunam89No ratings yet

- Dairy CooperativesDocument11 pagesDairy CooperativesRahul SadhNo ratings yet

- Customer Visit SOPDocument2 pagesCustomer Visit SOPMalik Ameer HamzaNo ratings yet

- Bharti Airtel Investor Presentation Highlights Strong GrowthDocument40 pagesBharti Airtel Investor Presentation Highlights Strong GrowthAbhimanyu Gupta100% (1)

- Case Amara RajaDocument2 pagesCase Amara RajaAnand JohnNo ratings yet

- 5.0 International Finance Compile Final All 5.0Document43 pages5.0 International Finance Compile Final All 5.0Min Yan LeeNo ratings yet

- 7Document62 pages7BilalNo ratings yet

- Cold Chain Industry in India A ReportDocument5 pagesCold Chain Industry in India A ReportANKUSHSINGH2690No ratings yet

- JIT - Case StudyDocument4 pagesJIT - Case StudyAsif Iqbal 2016289090No ratings yet

- Boston Creamery Variance Analysis Reveals $71K Profit GainDocument9 pagesBoston Creamery Variance Analysis Reveals $71K Profit GainwahyuNo ratings yet

- MarutiSuzukiFS2019-2020 (2021 - 12 - 15 12 - 08 - 53 UTC)Document353 pagesMarutiSuzukiFS2019-2020 (2021 - 12 - 15 12 - 08 - 53 UTC)HardikNo ratings yet

- In-depth Scrutiny of Service Invoices Reveals Cost SavingsDocument50 pagesIn-depth Scrutiny of Service Invoices Reveals Cost SavingsRohit YadavNo ratings yet

- Bisleri: Study On Bisleri - An Art of Successful BrandingDocument68 pagesBisleri: Study On Bisleri - An Art of Successful BrandingAashika ShahNo ratings yet

- Learning Curves: Dr. Anurag Tiwari IIM RohtakDocument27 pagesLearning Curves: Dr. Anurag Tiwari IIM Rohtaksili coreNo ratings yet

- Amara Raja Slides1Document13 pagesAmara Raja Slides1Javeed GurramkondaNo ratings yet

- Khimji Ramdas JDDocument2 pagesKhimji Ramdas JDAditya ChandolaNo ratings yet

- MONDELEZ INDIA FACTORY TRAININGDocument12 pagesMONDELEZ INDIA FACTORY TRAININGMonika JhaNo ratings yet

- Extruded Pellets From Maida For FryingDocument14 pagesExtruded Pellets From Maida For Frying124swadeshiNo ratings yet

- Technological - : Category Factors (PESTLE) Micromax LED TVDocument5 pagesTechnological - : Category Factors (PESTLE) Micromax LED TVrockyNo ratings yet

- SMSC 52 Command Reference Manual PDFDocument1,508 pagesSMSC 52 Command Reference Manual PDFTomNo ratings yet

- Prospects and Challenges of Contract Farming For Potato in IndiaDocument33 pagesProspects and Challenges of Contract Farming For Potato in IndiaPooraniNo ratings yet

- ExportDocument18 pagesExportUsha BastikarNo ratings yet

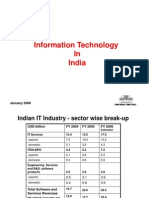

- Information Technology in India: January 2006Document18 pagesInformation Technology in India: January 2006richdev009_106456088100% (1)

- Amara Raja Vs ExideDocument50 pagesAmara Raja Vs ExideVarun BaxiNo ratings yet

- Exide Industries LTDDocument8 pagesExide Industries LTDVikram FernandezNo ratings yet

- Battery Industry in IndiaDocument43 pagesBattery Industry in IndiaSamrat ManchekarNo ratings yet

- Vacancy AdvertisementDocument1 pageVacancy AdvertisementJayangi PereraNo ratings yet

- HFB 1 F 61Document1 pageHFB 1 F 61Jayangi PereraNo ratings yet

- Gukj 3Document1 pageGukj 3Jayangi PereraNo ratings yet

- Brand Positioning & Competitive Advantage and Competitors Analysys KKKKKKKK Gvaiudbasdvmasvsvadnsacm MC cacsccvvvsfffffffdvghwigvwepgwhwhgre+g5G5WGWDocument1 pageBrand Positioning & Competitive Advantage and Competitors Analysys KKKKKKKK Gvaiudbasdvmasvsvadnsacm MC cacsccvvvsfffffffdvghwigvwepgwhwhgre+g5G5WGWJayangi PereraNo ratings yet

- Fjencvsmvs Lmvlmvldb":Dbzsb62 6S 3asvDocument1 pageFjencvsmvs Lmvlmvldb":Dbzsb62 6S 3asvJayangi PereraNo ratings yet

- Brand Positioning & Competitive Advantage and Competitors Analysys KKKKKKKK Gvaiudbasdvmasvsvadnsacm MC cacsccvvvsfffffffdvghwigvwepgwhwhgre+g5G5WGWDocument1 pageBrand Positioning & Competitive Advantage and Competitors Analysys KKKKKKKK Gvaiudbasdvmasvsvadnsacm MC cacsccvvvsfffffffdvghwigvwepgwhwhgre+g5G5WGWJayangi PereraNo ratings yet

- DVD5+V5A+V+V5AS+SABABASVDocument1 pageDVD5+V5A+V+V5AS+SABABASVJayangi PereraNo ratings yet

- Event Line UpMod2Document1 pageEvent Line UpMod2Jayangi PereraNo ratings yet

- Scsa Z ZDocument1 pageScsa Z ZJayangi PereraNo ratings yet

- Gvhwepvsa BMS' Bsfb5Ws B2 Dwv2Q+Gv Dsav +D4Bv+WbwsbsfbsbwsbDocument1 pageGvhwepvsa BMS' Bsfb5Ws B2 Dwv2Q+Gv Dsav +D4Bv+WbwsbsfbsbwsbJayangi PereraNo ratings yet

- Kbmsdbnmb'0062bdfzb314ng 5n1656+46vb6 5ds4bsDocument1 pageKbmsdbnmb'0062bdfzb314ng 5n1656+46vb6 5ds4bsJayangi PereraNo ratings yet

- BSD system documentationDocument1 pageBSD system documentationJayangi PereraNo ratings yet

- Brand Positioning & Competitive Advantage and Competitors Analysys KKKKKKKK Gvaiudbasdvmasvsvadnsacm MC CacsccvvvsfffffffDocument1 pageBrand Positioning & Competitive Advantage and Competitors Analysys KKKKKKKK Gvaiudbasdvmasvsvadnsacm MC CacsccvvvsfffffffJayangi PereraNo ratings yet

- Brand Positioning & Competitive Advantage and Competitors Analysys KKKKKKKK Gvaiudbasdvmasvsvadnsacm MC cacsccvvvsfffffffdvghwigvwepgwhwhgre+g5G5WGWDocument1 pageBrand Positioning & Competitive Advantage and Competitors Analysys KKKKKKKK Gvaiudbasdvmasvsvadnsacm MC cacsccvvvsfffffffdvghwigvwepgwhwhgre+g5G5WGWJayangi PereraNo ratings yet

- Brand Positioning & Competitive Advantage and Competitors AnalysysDocument1 pageBrand Positioning & Competitive Advantage and Competitors AnalysysJayangi PereraNo ratings yet

- Brand Positioning & Competitive Advantage and Competitors Analysys KKKKKKKK GvaiudbasdvmasvsvaDocument1 pageBrand Positioning & Competitive Advantage and Competitors Analysys KKKKKKKK GvaiudbasdvmasvsvaJayangi PereraNo ratings yet

- Practical training Division Manager letterDocument1 pagePractical training Division Manager letterJayangi PereraNo ratings yet

- Brand Positioning & Competitive Advantage and Competitors Analysys KKKKKKKK Gvaiudbasdvmasvsvadnsacm MC CacsccvvvsDocument1 pageBrand Positioning & Competitive Advantage and Competitors Analysys KKKKKKKK Gvaiudbasdvmasvsvadnsacm MC CacsccvvvsJayangi PereraNo ratings yet

- Amaron Don 36Document1 pageAmaron Don 36Jayangi PereraNo ratings yet

- Amaron New2Document1 pageAmaron New2Jayangi PereraNo ratings yet

- ExcideDocument2 pagesExcideJayangi PereraNo ratings yet

- Amaron New2Document1 pageAmaron New2Jayangi PereraNo ratings yet

- Private & Confidential: 5 June, 2007Document1 pagePrivate & Confidential: 5 June, 2007Jayangi PereraNo ratings yet

- Re Coo Mend AtionsDocument1 pageRe Coo Mend AtionsJayangi PereraNo ratings yet

- Practical training Division Manager letterDocument1 pagePractical training Division Manager letterJayangi PereraNo ratings yet

- Letter of ResignationDocument1 pageLetter of ResignationJayangi Perera100% (1)

- Practical training Division Manager letterDocument1 pagePractical training Division Manager letterJayangi PereraNo ratings yet

- Training RequestDocument1 pageTraining RequestJayangi PereraNo ratings yet

- Training RequestDocument1 pageTraining RequestJayangi PereraNo ratings yet

- Feasibility Study On Establishment of A Boondi Manufacturing PlantDocument35 pagesFeasibility Study On Establishment of A Boondi Manufacturing PlantSukitha KothalawalaNo ratings yet

- Analyzing Stock Market Data with PandasDocument16 pagesAnalyzing Stock Market Data with PandasAbhisek KeshariNo ratings yet

- Financial Statement Analysis TechniquesDocument8 pagesFinancial Statement Analysis TechniquesJomar VillenaNo ratings yet

- RH Perennial - Nov 21Document46 pagesRH Perennial - Nov 21sambitNo ratings yet

- Factors Affecting Subjective Financial Well-Being of Emerging Adults in MalaysiaDocument17 pagesFactors Affecting Subjective Financial Well-Being of Emerging Adults in MalaysiaMeisha GunnNo ratings yet

- Hull: Fundamentals of Futures and Options Markets, Ninth Edition Chapter 1: Introduction Multiple Choice Test BankDocument5 pagesHull: Fundamentals of Futures and Options Markets, Ninth Edition Chapter 1: Introduction Multiple Choice Test BankfdvdfvNo ratings yet

- Bihar Startup Policy 2016Document35 pagesBihar Startup Policy 2016Vikash KushwahaNo ratings yet

- LC Business Overseas BranchesDocument202 pagesLC Business Overseas BranchesSumalNo ratings yet

- Questionnaire: Respected Sir/MadamDocument4 pagesQuestionnaire: Respected Sir/MadamhunnyNo ratings yet

- New Format Application Form CLRDocument8 pagesNew Format Application Form CLRtheonelNo ratings yet

- Designing Corporate Venturing Capital Successfully Startup Intellect Featured Insight Report FinalDocument24 pagesDesigning Corporate Venturing Capital Successfully Startup Intellect Featured Insight Report Finalali sharifzadehNo ratings yet

- SEBI rules PGF business a collective investment schemeDocument23 pagesSEBI rules PGF business a collective investment schemejay1singheeNo ratings yet

- Determine equilibrium price and output under demand and supplyDocument10 pagesDetermine equilibrium price and output under demand and supplyBisweswar DashNo ratings yet

- Limit Pricing, Entry Deterrence and Predatory PricingDocument16 pagesLimit Pricing, Entry Deterrence and Predatory PricingAnwesha GhoshNo ratings yet

- Company Law Study PlanDocument10 pagesCompany Law Study PlanSheharyar RafiqNo ratings yet

- IPR April 2017 Issue 1 Ipad FinalDocument84 pagesIPR April 2017 Issue 1 Ipad FinalamittekaleNo ratings yet

- 370 - 13735 - EA221 - 2010 - 1 - 1 - 1 - Linear Programming 1Document73 pages370 - 13735 - EA221 - 2010 - 1 - 1 - 1 - Linear Programming 1Catrina NunezNo ratings yet

- Basics of Profit & Loss ConceptsDocument10 pagesBasics of Profit & Loss ConceptsNirnay AkelaNo ratings yet

- CMA Blank FormDocument34 pagesCMA Blank FormbipinNo ratings yet

- Chapter 11 15FinAcc2Document55 pagesChapter 11 15FinAcc2Kariz Codog22% (9)

- Reading 25 Non-Current (Long-Term) LiabilitiesDocument18 pagesReading 25 Non-Current (Long-Term) LiabilitiesARPIT ARYANo ratings yet

- BirlasoftDocument3 pagesBirlasoftlubna ghazalNo ratings yet