You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Automated EWhore Traffic MethodDocument7 pagesAutomated EWhore Traffic MethodCalvin CarterNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Training Institute Business PlanDocument6 pagesTraining Institute Business PlanRehan Yousaf83% (6)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- QuestionaireDocument5 pagesQuestionaireMohsan SheikhNo ratings yet

- Terms and Conditions: (Receipt For The Recipient)Document1 pageTerms and Conditions: (Receipt For The Recipient)sagar aroraNo ratings yet

- Pessi OrdinanceDocument34 pagesPessi OrdinanceMohsan Sheikh100% (1)

- June NLDocument20 pagesJune NLMohsan SheikhNo ratings yet

- Team Alfalah: Pakistan Super League - 2017Document19 pagesTeam Alfalah: Pakistan Super League - 2017Mohsan SheikhNo ratings yet

- August Newsletter AficDocument18 pagesAugust Newsletter AficMohsan SheikhNo ratings yet

- Cover Page Team AlfalahDocument19 pagesCover Page Team AlfalahMohsan SheikhNo ratings yet

- April NLDocument17 pagesApril NLMohsan SheikhNo ratings yet

- SRO-Code of Corporate Governance For Insurers, 2016Document36 pagesSRO-Code of Corporate Governance For Insurers, 2016Mohsan SheikhNo ratings yet

- Zakatushr1980 PDFDocument37 pagesZakatushr1980 PDFMohsan SheikhNo ratings yet

- National Insurance CorporationAnnual Report 2009Document135 pagesNational Insurance CorporationAnnual Report 2009Mohsan SheikhNo ratings yet

- GK II Subjective 2014Document1 pageGK II Subjective 2014Daniyal ArifNo ratings yet

- Most Commonly Used Abbreviations & Their Meanings: Abbreviation Used in ITDocument2 pagesMost Commonly Used Abbreviations & Their Meanings: Abbreviation Used in ITMohsan SheikhNo ratings yet

- Insurance Ordinance, 2000: (Amended Upto November 2011)Document125 pagesInsurance Ordinance, 2000: (Amended Upto November 2011)6128437No ratings yet

- Adamjee InsuranceDocument80 pagesAdamjee InsuranceMohsan SheikhNo ratings yet

- PAK HR AddressesDocument104 pagesPAK HR AddressesFaisal Mustafa100% (1)

- General Insurance in Pakistan-PACRADocument20 pagesGeneral Insurance in Pakistan-PACRAMohsan SheikhNo ratings yet

- QsDocument3 pagesQsMohsan SheikhNo ratings yet

- PlanDocument51 pagesPlanVipul KaushikNo ratings yet

- Dessler - HRM12e - Ch8-Performance Management and AppraisalDocument29 pagesDessler - HRM12e - Ch8-Performance Management and AppraisalMohsan SheikhNo ratings yet

- WT G Assignment 3 Fa 131Document1 pageWT G Assignment 3 Fa 131Mohsan SheikhNo ratings yet

- Ch#4Document10 pagesCh#4Mohsan SheikhNo ratings yet

- Marine Insurance: Chapter No.6Document11 pagesMarine Insurance: Chapter No.6Mohsan SheikhNo ratings yet

- The Stamp Act, 1899Document52 pagesThe Stamp Act, 1899Mohsan SheikhNo ratings yet

- Title ReinsuranceDocument2 pagesTitle ReinsuranceMohsan SheikhNo ratings yet

- Dessler 10Document22 pagesDessler 10Mohsan Sheikh67% (3)

- pp07Document14 pagespp07Mohsan Sheikh0% (1)

- Annual Report 2012 Servis IndustriesDocument96 pagesAnnual Report 2012 Servis IndustriesMohsan SheikhNo ratings yet

- Sehr IshDocument44 pagesSehr Ishmohsan_tanveer486No ratings yet

- Miss Ntuli Ned NovDocument4 pagesMiss Ntuli Ned NovBilal Same50% (2)

- Your Vi Bill: Rs 299.00 Rs 310.00 Rs 0.00 Rs 299.00 Rs 338.00Document2 pagesYour Vi Bill: Rs 299.00 Rs 310.00 Rs 0.00 Rs 299.00 Rs 338.00Rahul KumarNo ratings yet

- Kamus Ilmiah Populer: Rating: (40 Votes) ID Number: KA-1F7426AEECFFB85 - Format: EnglishDocument2 pagesKamus Ilmiah Populer: Rating: (40 Votes) ID Number: KA-1F7426AEECFFB85 - Format: EnglishUzi SuruziNo ratings yet

- Airbnb Travel Receipt, Confirmation Code HMAB5TZXYKDocument2 pagesAirbnb Travel Receipt, Confirmation Code HMAB5TZXYKAirbnb USNo ratings yet

- Reliance Mutual Funds ProjectDocument58 pagesReliance Mutual Funds ProjectShivangi SinghNo ratings yet

- DCCPDFDocument20 pagesDCCPDFKirti MahajanNo ratings yet

- Engineering Economy and Blockchain Technology: Abstract - Engineering Economy Is A Discipline That Plays ADocument4 pagesEngineering Economy and Blockchain Technology: Abstract - Engineering Economy Is A Discipline That Plays AInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- CS/PS Core Network Planning: Who Should Attend?Document3 pagesCS/PS Core Network Planning: Who Should Attend?algard 29No ratings yet

- Non-Store Retailing Is The Selling of Goods and Services Outside The Confines of A RetailDocument1 pageNon-Store Retailing Is The Selling of Goods and Services Outside The Confines of A RetailAkash Girish DoshiNo ratings yet

- BIB-HSE-OCP31-R0 Coal Hauling Safety ProcedureDocument4 pagesBIB-HSE-OCP31-R0 Coal Hauling Safety Procedurelamosy78No ratings yet

- Introduction To NetSimDocument8 pagesIntroduction To NetSimgowdamandaviNo ratings yet

- Receipt PDFDocument1 pageReceipt PDFAffendi Hj AriffinNo ratings yet

- PremiumDocument14 pagesPremiumWis MarketingNo ratings yet

- RP-091353 Report RAN 45 SevilleDocument155 pagesRP-091353 Report RAN 45 SevilleDellNo ratings yet

- Rescheduling LetterDocument2 pagesRescheduling Letterمحمدريحان سعيد بتيلNo ratings yet

- The Top Hedge Funds Everyone Wants To Work For, and Why - eFinancialCareersDocument3 pagesThe Top Hedge Funds Everyone Wants To Work For, and Why - eFinancialCareersMaryNo ratings yet

- ElearningDocument5 pagesElearningRaj KumarNo ratings yet

- Adrian - Borbe - CHAPTER 1 5 1Document149 pagesAdrian - Borbe - CHAPTER 1 5 1ecilaborbe2003No ratings yet

- E-Ticket: Trip 1: Patna To SuratDocument2 pagesE-Ticket: Trip 1: Patna To Suratenjoy begening lifeNo ratings yet

- Comparative Analysis On NBFC & Banks NPADocument33 pagesComparative Analysis On NBFC & Banks NPABHAVESH KHOMNENo ratings yet

- Report Lpco BNK Expr PermDocument1 pageReport Lpco BNK Expr PermBézã Atsëdå ÂlêxNo ratings yet

- Mobile Money Service Provistion in EthiopiaDocument111 pagesMobile Money Service Provistion in Ethiopiahaymanot kabaNo ratings yet

- Radio Gateway Unit (Translator To Existing Marine and Air To GND)Document2 pagesRadio Gateway Unit (Translator To Existing Marine and Air To GND)jittiman NittayawaNo ratings yet

- Udchalo Itinerary (Dfy1Th) : Passenger InformationDocument2 pagesUdchalo Itinerary (Dfy1Th) : Passenger InformationNarenderNo ratings yet

- Gift CardDocument1 pageGift CardJuan José RamirezNo ratings yet

- Nasib R Awan Forensic MedicineDocument101 pagesNasib R Awan Forensic Medicineoh mrymNo ratings yet

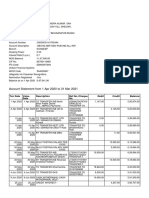

- Account Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument3 pagesAccount Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAbhay RajNo ratings yet

- EXAM ITIL Foundation Examination SampleA v5.1 Questions & Answers RetDocument10 pagesEXAM ITIL Foundation Examination SampleA v5.1 Questions & Answers RetjuancarhdezNo ratings yet