You might also like

- General Ledger Debits and Credits Normal Account Balances Journal Entries The Income StatementDocument11 pagesGeneral Ledger Debits and Credits Normal Account Balances Journal Entries The Income Statementpri_dulkar4679No ratings yet

- Accounting Equation and Financial Statements ExplainedDocument12 pagesAccounting Equation and Financial Statements ExplainedAishah Rafat Abdussattar100% (1)

- Types of Major Accounts: An Account Is The Basic Storage of Information in AccountingDocument15 pagesTypes of Major Accounts: An Account Is The Basic Storage of Information in AccountingGab GamboaNo ratings yet

- Accounting Fundamental: BY: Bayani D. Edlagan Ma. Cecilia S. MercadoDocument270 pagesAccounting Fundamental: BY: Bayani D. Edlagan Ma. Cecilia S. MercadoSai Kumar Ponna100% (2)

- Module 7 - Completing The Accounting CycleDocument6 pagesModule 7 - Completing The Accounting CycleMJ San PedroNo ratings yet

- Excel Skills - Basic Accounting Template: InstructionsDocument39 pagesExcel Skills - Basic Accounting Template: InstructionsStorage BankNo ratings yet

- Sample Accounting ExcelDocument23 pagesSample Accounting ExcelClarisse30No ratings yet

- Journalizing, Posting and BalancingDocument21 pagesJournalizing, Posting and Balancinganuradha100% (1)

- ACC10 L1 01 Fundamentals of Accounting CgomezDocument6 pagesACC10 L1 01 Fundamentals of Accounting CgomezccgomezNo ratings yet

- Financial Accounting and Accounting StandardsDocument31 pagesFinancial Accounting and Accounting StandardsIrwan JanuarNo ratings yet

- Adjusting EntriesDocument7 pagesAdjusting EntriesJon PangilinanNo ratings yet

- Business Finance: Financial Statement Preparation, Analysis, and InterpretationDocument7 pagesBusiness Finance: Financial Statement Preparation, Analysis, and InterpretationRosalyn Mauricio VelascoNo ratings yet

- Sales Journal and Accounts Receivable Subsidiary LedgerDocument4 pagesSales Journal and Accounts Receivable Subsidiary LedgerMary100% (5)

- Understanding Accounting Fundamentals and Business EntitiesDocument27 pagesUnderstanding Accounting Fundamentals and Business Entitiesdhanyasugukumar100% (2)

- Accounting in Action 12eDocument65 pagesAccounting in Action 12eMd Shawfiqul Islam0% (1)

- Chapter 4 Books of Accounts and Double Entry SystemDocument61 pagesChapter 4 Books of Accounts and Double Entry SystemMonica BuscatoNo ratings yet

- Corporation Accounting - Retained EarningsDocument3 pagesCorporation Accounting - Retained EarningsGuadaMichelleGripalNo ratings yet

- One Full Accounting Cycle Process ExplainedDocument11 pagesOne Full Accounting Cycle Process ExplainedRiaz Ahmed100% (1)

- Manufacturing AccountDocument36 pagesManufacturing AccountSaksham RainaNo ratings yet

- Journal Entries - Financial AccountingDocument3 pagesJournal Entries - Financial AccountingElham JabarkhailNo ratings yet

- Understanding The Income StatementDocument4 pagesUnderstanding The Income Statementluvujaya100% (1)

- Accounting EquationDocument31 pagesAccounting EquationgganyanNo ratings yet

- Worksheet Multiple ChoiceDocument11 pagesWorksheet Multiple ChoiceiamjnschrstnNo ratings yet

- Accounting PrinciplesDocument11 pagesAccounting PrinciplesPiyush AjmeraNo ratings yet

- Reversing EntriesDocument9 pagesReversing EntriesHumair Ahmed100% (1)

- ACCOUNTINGDocument31 pagesACCOUNTINGCHARAK RAYNo ratings yet

- Manual Accounting Practice SetDocument13 pagesManual Accounting Practice SetNguyen Thien Anh Tran100% (2)

- Basic Accounting Final ExamDocument7 pagesBasic Accounting Final ExamCharmae Agan Caroro75% (4)

- 6 Completion of Accounting Cycle UDDocument28 pages6 Completion of Accounting Cycle UDERICK MLINGWANo ratings yet

- TOPIC 6 - Bookeeping ProceduresDocument31 pagesTOPIC 6 - Bookeeping Procedureseizah_osman3408100% (1)

- All Tally TheoryDocument21 pagesAll Tally Theoryvijay024088% (17)

- Week11-Completing The Accounting CycleDocument44 pagesWeek11-Completing The Accounting CycleAmir Indrabudiman100% (2)

- Comprehensive Problem Accounting 101Document2 pagesComprehensive Problem Accounting 101Heidi Norris Dawson25% (4)

- Financial Accounting Vol. 2 Example QuestionsDocument8 pagesFinancial Accounting Vol. 2 Example QuestionsMarisolNo ratings yet

- Intro to Accounting: Tracking Business EventsDocument22 pagesIntro to Accounting: Tracking Business EventsTeacher Roschelle mariñasNo ratings yet

- Chapter 6 - Preparation of Financial StatementsDocument10 pagesChapter 6 - Preparation of Financial StatementspolymeianNo ratings yet

- Worksheet ProblemsDocument3 pagesWorksheet ProblemsClaren Sidnne MadridNo ratings yet

- Acct TutorDocument22 pagesAcct TutorKthln Mntlla100% (1)

- Special Journals Accounting)Document15 pagesSpecial Journals Accounting)Ardialyn100% (3)

- 1 Completing The Accounting Cycle-1Document17 pages1 Completing The Accounting Cycle-1Toshi PrataNo ratings yet

- Adjusting Entries ExplainedDocument47 pagesAdjusting Entries Explainedqqdelossantos100% (1)

- Accounting ProblemsDocument7 pagesAccounting ProblemsMarisolNo ratings yet

- CHAPTER 3 - Accounting EquationDocument16 pagesCHAPTER 3 - Accounting Equationyow jing pei100% (2)

- Bookkeeping NC III exam guide and reviewerDocument7 pagesBookkeeping NC III exam guide and reviewerali ulamaNo ratings yet

- Depreciation Lesson 8Document39 pagesDepreciation Lesson 8Charos Aslonovna100% (5)

- Chap-1 Accounting in Action Basic Accountin Equation Financial Statement Chp-1Document51 pagesChap-1 Accounting in Action Basic Accountin Equation Financial Statement Chp-1IH MarufNo ratings yet

- UNIT II Branches of AccountingDocument40 pagesUNIT II Branches of AccountingJOHN ,MARK LIGPUSANNo ratings yet

- Accounting Principles and Concepts LectureDocument9 pagesAccounting Principles and Concepts LectureMary De JesusNo ratings yet

- Introduction to the Accounting EquationDocument8 pagesIntroduction to the Accounting EquationAlma Dimaranan-AcuñaNo ratings yet

- Accounting Assignment 04A 207Document10 pagesAccounting Assignment 04A 207Aniyah's RanticsNo ratings yet

- Reviewer 2, Fundamentals of Accounting 2Document22 pagesReviewer 2, Fundamentals of Accounting 2Hunson Abadeer100% (2)

- Accounting 10 HandoutsDocument18 pagesAccounting 10 HandoutsYssa SadjiNo ratings yet

- Accounting 1: Fundamental ofDocument78 pagesAccounting 1: Fundamental ofLuisitoNo ratings yet

- Accounting Equation and Double Entry System3Document11 pagesAccounting Equation and Double Entry System3Malvin Roix OrenseNo ratings yet

- Basic Accounting Course ModuleDocument5 pagesBasic Accounting Course ModuleBlairEmrallafNo ratings yet

- Completing The Accounting CycleDocument52 pagesCompleting The Accounting CycleHEM CHEA100% (2)

- Problems Journal EntryDocument5 pagesProblems Journal EntryColleen GuimbalNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Entry Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Entry Level: Australian EditionNo ratings yet

- Computerised Accounting Practice Set Using Xero Online Accounting: Australian EditionFrom EverandComputerised Accounting Practice Set Using Xero Online Accounting: Australian EditionNo ratings yet

- Budget and BudgetryDocument6 pagesBudget and Budgetryram sagar100% (1)

- Ram Dhondiba SagarDocument12 pagesRam Dhondiba Sagarram sagarNo ratings yet

- Computer BasicsDocument403 pagesComputer Basicsram sagar90% (10)

- Books of AccountsDocument3 pagesBooks of Accountsram sagar83% (6)

- When Cities Take Bicycles SeriouslyDocument4 pagesWhen Cities Take Bicycles SeriouslyDaisyNo ratings yet

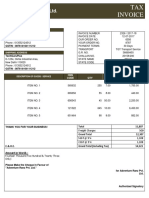

- Adventure Ranz Pvt. Ltd. tax invoice for TechGuruPlusDocument1 pageAdventure Ranz Pvt. Ltd. tax invoice for TechGuruPlusArindam ChandaNo ratings yet

- Quiz 2Document54 pagesQuiz 2Karthik Vee33% (3)

- History of ShippingDocument10 pagesHistory of Shippingbarakkat72100% (1)

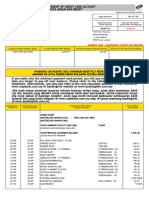

- Statement 2022 10 25Document5 pagesStatement 2022 10 25Vincenzo MarsalaNo ratings yet

- Surrender or Chargee Form PDFDocument1 pageSurrender or Chargee Form PDFSherlyn PhoonNo ratings yet

- SAP Mannual FinanceDocument212 pagesSAP Mannual FinanceHridya PrasadNo ratings yet

- Maybank Card - Convenience, Savings and Rewards: Maybank Islamic Berhad (787435-M)Document4 pagesMaybank Card - Convenience, Savings and Rewards: Maybank Islamic Berhad (787435-M)azjNo ratings yet

- Lorenza Morales Vargas, DeudaDocument1 pageLorenza Morales Vargas, DeudaalarchorrNo ratings yet

- OdunDocument3 pagesOdunLoco CocoNo ratings yet

- Mpesa Transaction HistoryDocument12 pagesMpesa Transaction HistoryMadeleiGOOGYXNo ratings yet

- The Study of Electronic Payment SystemsDocument4 pagesThe Study of Electronic Payment SystemsasalihovicNo ratings yet

- Soa 102021Document2 pagesSoa 102021Jethro VillahermosaNo ratings yet

- SMS LOG ANALYSISDocument43 pagesSMS LOG ANALYSISSwasthi Vachanam100% (1)

- Annex B 2 RR 11 2018 PDFDocument1 pageAnnex B 2 RR 11 2018 PDFDnrxsNo ratings yet

- 1z0 1055Document4 pages1z0 1055AliNo ratings yet

- Professor T. R. Lakshmanan: September 9, 2008Document25 pagesProfessor T. R. Lakshmanan: September 9, 2008Khoo Beng KiatNo ratings yet

- CPA Review: Introduction to Regular Income TaxDocument3 pagesCPA Review: Introduction to Regular Income TaxJennifer ArcadioNo ratings yet

- BillsDocument2 pagesBillsdevNo ratings yet

- APTC form-40-A-GPFDocument2 pagesAPTC form-40-A-GPFvijay_dilse100% (1)

- Kelas 2Document2 pagesKelas 2Okvita FirliNo ratings yet

- Jawaban Ud WirastriDocument17 pagesJawaban Ud WirastriDevitaNo ratings yet

- Customer bank statement overviewDocument4 pagesCustomer bank statement overviewsamaa adelNo ratings yet

- Slice Account Statement - Jun '22Document7 pagesSlice Account Statement - Jun '22Gowtham ChallaNo ratings yet

- Lorry BillDocument2 pagesLorry BillShyam SNo ratings yet

- 1537121139046Document5 pages1537121139046mkr9466No ratings yet

- Tax Filing Reminders: OutlineDocument30 pagesTax Filing Reminders: OutlineMarc Nathaniel RanayNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument8 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancehemanth7390No ratings yet

- PT Graha Inti Jaya: Purchase OrderDocument1 pagePT Graha Inti Jaya: Purchase OrderDessy MonalisaNo ratings yet

- DD Form HDFCDocument1 pageDD Form HDFCVikas LokhandeNo ratings yet