You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Why Documentation Is Necessary in Business TransactionsDocument19 pagesWhy Documentation Is Necessary in Business Transactionsrohan100% (2)

- Beyond Diet Meal PlansDocument72 pagesBeyond Diet Meal Plansintankamaruddin100% (3)

- Base Tables For Order To CashDocument5 pagesBase Tables For Order To CashVishal100% (1)

- A Flying SaucerDocument15 pagesA Flying SaucerIsa RosaeNo ratings yet

- Marketing Plan - Nestle Fruita VitalsDocument33 pagesMarketing Plan - Nestle Fruita VitalsJaweria SaghirNo ratings yet

- A Trio of Pretty Baby Hats Free PatternDocument5 pagesA Trio of Pretty Baby Hats Free PatternThimany00No ratings yet

- Effective Visual Merchandising in Fashion RetailDocument183 pagesEffective Visual Merchandising in Fashion RetailFABIONo ratings yet

- Softwash Lavamac FinalengDocument12 pagesSoftwash Lavamac FinalengRodrigo SócrateNo ratings yet

- The Determination of Ascorbic AcidDocument5 pagesThe Determination of Ascorbic AcidCarina JLNo ratings yet

- Diagnostic Test in Dressmaking Grade 10Document3 pagesDiagnostic Test in Dressmaking Grade 10CARYL ARANJUEZNo ratings yet

- We Buy Junk Cars: D DeelliigghhttDocument16 pagesWe Buy Junk Cars: D DeelliigghhttCoolerAdsNo ratings yet

- Chicago Electric Welder 68887 PDFDocument28 pagesChicago Electric Welder 68887 PDFJohnNo ratings yet

- Borcure - Packaging ConferenceDocument5 pagesBorcure - Packaging ConferencegandhiannexNo ratings yet

- 2008 Customs Tariff - TV NigeriaDocument552 pages2008 Customs Tariff - TV NigeriaAriKurniawanNo ratings yet

- Kmart: Kegagalan Enterprise ArchitectureDocument3 pagesKmart: Kegagalan Enterprise ArchitectureSaintz ZeeNo ratings yet

- Li FungDocument8 pagesLi FungSai VasudevanNo ratings yet

- Sales Presentation - Consumer DurablesDocument50 pagesSales Presentation - Consumer DurablesdrifterdriverNo ratings yet

- Runner Ru4rxDocument45 pagesRunner Ru4rxfcdypmsbssNo ratings yet

- Fratelli CaseDocument28 pagesFratelli Casetsimpo12No ratings yet

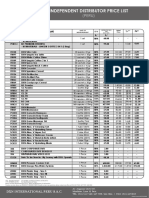

- Independent Distributor Price List: (PERU)Document1 pageIndependent Distributor Price List: (PERU)Giomar SotoNo ratings yet

- Grasim Industries LimitedDocument4 pagesGrasim Industries LimitedAvani KukrejaNo ratings yet

- Design Brief - Water FiltrationDocument2 pagesDesign Brief - Water Filtrationapi-398736122No ratings yet

- Costco PDFDocument4 pagesCostco PDFmessiNo ratings yet

- Floor PlanDocument1 pageFloor Planapi-496031599No ratings yet

- Business PlanDocument26 pagesBusiness PlanBarbie BleuNo ratings yet

- Bahrain FlyerDocument3 pagesBahrain Flyerzahid_497No ratings yet

- Dealers Attitude QuestionnaireDocument3 pagesDealers Attitude QuestionnaireSUKUMAR80% (10)

- How To Make A Quick & Easy Amtgard-Legal Shield'Document5 pagesHow To Make A Quick & Easy Amtgard-Legal Shield'Royce A R PorterNo ratings yet

- 2013 版 ASME BPVC 价格表Document3 pages2013 版 ASME BPVC 价格表Andri Dwi MaryantoNo ratings yet

- Kootenay Lake Pennywise - July 16, 2013Document56 pagesKootenay Lake Pennywise - July 16, 2013Pennywise PublishingNo ratings yet