You might also like

- Why Should You Choose AccountancyDocument4 pagesWhy Should You Choose AccountancyJR GabrielNo ratings yet

- Case Analysis For Human Behavior in Organization (MIDTERM EXAM)Document3 pagesCase Analysis For Human Behavior in Organization (MIDTERM EXAM)Honeylet SigesmundoNo ratings yet

- MCQ With AnswersDocument3 pagesMCQ With AnswersLakshmiRengarajan90% (10)

- Roque Quick Auditing Theory Chapter 12 PDFDocument133 pagesRoque Quick Auditing Theory Chapter 12 PDFSherene Faith Carampatan0% (1)

- Study Note 2.1 Page (60-79)Document20 pagesStudy Note 2.1 Page (60-79)s4sahith88% (8)

- Chapter 4 - Industry AnalysisDocument37 pagesChapter 4 - Industry AnalysisMichael John OliveriaNo ratings yet

- Finacle Menu and TablesDocument72 pagesFinacle Menu and TablesVikash Palhan54% (13)

- Error CorrectionDocument8 pagesError CorrectionCharlie Magne G. SantiaguelNo ratings yet

- Acchievement Test Fabm2Document5 pagesAcchievement Test Fabm2Carmelo John Delacruz100% (1)

- Chapter 7 SolutionsDocument6 pagesChapter 7 SolutionsJay100% (1)

- Accounting for merchandising businessesDocument13 pagesAccounting for merchandising businessesAprilNo ratings yet

- Lumban Senior High School: "The Home of Future Leaders."Document6 pagesLumban Senior High School: "The Home of Future Leaders."Francesnova B. Dela PeñaNo ratings yet

- Afar Preliminary QuestionsDocument22 pagesAfar Preliminary QuestionsAiko YoonNo ratings yet

- Business Finance - LAS - q1 - w1 Introduction To Financial Management PDFDocument9 pagesBusiness Finance - LAS - q1 - w1 Introduction To Financial Management PDFJustineNo ratings yet

- Ap Tip Preweek 2017Document58 pagesAp Tip Preweek 2017Jay-L Tan100% (1)

- Sallys Struthers - Answer KeyDocument7 pagesSallys Struthers - Answer KeyLlyod Francis LaylayNo ratings yet

- Challenges of Sole Proprietorship BusinessesDocument20 pagesChallenges of Sole Proprietorship BusinessesIvy CoronelNo ratings yet

- Financial Assets at Fair Value Through Profit or LossDocument13 pagesFinancial Assets at Fair Value Through Profit or LossALEJANDRE, Chris Shaira M.No ratings yet

- Sales DiscountsDocument42 pagesSales DiscountsOliviaDuchessNo ratings yet

- Lesson on Sets - Definitions, Types, Operations and RepresentationsDocument12 pagesLesson on Sets - Definitions, Types, Operations and RepresentationsLiandysan23No ratings yet

- Business LogicDocument4 pagesBusiness LogicAhcy SongNo ratings yet

- Summary Enhancing Qualitative CharacteristicsDocument3 pagesSummary Enhancing Qualitative CharacteristicsCahyani PrastutiNo ratings yet

- Fabm Module4Document50 pagesFabm Module4Paulo VisitacionNo ratings yet

- Lesson 1 Prepared By: Asst. Prof. Sherylyn T. Trinidad: The Management ScienceDocument17 pagesLesson 1 Prepared By: Asst. Prof. Sherylyn T. Trinidad: The Management ScienceErine ContranoNo ratings yet

- Script College of Orientation ProgramDocument7 pagesScript College of Orientation ProgramCara GreatNo ratings yet

- Statute of Fraud ExceptionsDocument2 pagesStatute of Fraud ExceptionsMelwin CalubayanNo ratings yet

- Identify Financial Statement ElementsDocument2 pagesIdentify Financial Statement ElementsMarlyn Lotivio100% (1)

- Module 2 - Introduction To BusinessDocument4 pagesModule 2 - Introduction To BusinessMarjorie Rose GuarinoNo ratings yet

- AC 4103 OBEdized SyllabusDocument21 pagesAC 4103 OBEdized SyllabusAyame KusuragiNo ratings yet

- Fundamentals of Accountancy, Business and Management 1 Accounting Cycle of A Merchandising BusinessDocument15 pagesFundamentals of Accountancy, Business and Management 1 Accounting Cycle of A Merchandising BusinessVeniceNo ratings yet

- Ethics 3.1 1Document38 pagesEthics 3.1 1Nicole Tonog AretañoNo ratings yet

- Causes and Effects of Public Speaking Anxiety among E-MQI FreshmenDocument47 pagesCauses and Effects of Public Speaking Anxiety among E-MQI FreshmenVi Diễm QuỳnhNo ratings yet

- Ba 43: Marketing and Finance EssentialsDocument10 pagesBa 43: Marketing and Finance EssentialsCharles GalidoNo ratings yet

- Introduction To Financial ManagementDocument17 pagesIntroduction To Financial ManagementAisah ReemNo ratings yet

- 11-Responsibilty AccountingDocument10 pages11-Responsibilty AccountingBhagaban DasNo ratings yet

- Flow of Funds ModuleDocument7 pagesFlow of Funds ModuleKanton FernandezNo ratings yet

- Learn the Fundamentals of Volleyball ServingDocument4 pagesLearn the Fundamentals of Volleyball ServingKim Tanjuan100% (1)

- Southland College: Rizal ST., Kabankalan City, Negros OccidentalDocument17 pagesSouthland College: Rizal ST., Kabankalan City, Negros OccidentalJohn Paul ChavezNo ratings yet

- College of AccountancyDocument11 pagesCollege of Accountancyjim fuentesNo ratings yet

- Accrued Revenue: This Is Handout 020 Accruals Please Use This Handout For Lesson 020 Adjusting Entries 4 - AccrualsDocument3 pagesAccrued Revenue: This Is Handout 020 Accruals Please Use This Handout For Lesson 020 Adjusting Entries 4 - AccrualsCaryl May Esparrago MiraNo ratings yet

- Thesis/Dissertation Adviser'S Review GuideDocument8 pagesThesis/Dissertation Adviser'S Review Guideisko dapakersNo ratings yet

- Main components of a computer systemDocument6 pagesMain components of a computer systemLarry RicoNo ratings yet

- BSMA PrE 417 PERFORMANCE MANAGEMENT SYSTEMDocument8 pagesBSMA PrE 417 PERFORMANCE MANAGEMENT SYSTEMDonna ZanduetaNo ratings yet

- Suggestions For Final Exam: Course Title: Financial ManagementDocument28 pagesSuggestions For Final Exam: Course Title: Financial ManagementShams IstehaadNo ratings yet

- Bookkeeping Lesson EditedDocument23 pagesBookkeeping Lesson EditedLu CioNo ratings yet

- CH 9 - Completing The Cycle - MerchandisingDocument38 pagesCH 9 - Completing The Cycle - MerchandisingJem Bobiles100% (1)

- Accounting in Our Daily LifeDocument3 pagesAccounting in Our Daily LifeJaeseupeo JHas VicenteNo ratings yet

- Managing Accounts Receivables and its Effect on Hardware Store PerformanceDocument33 pagesManaging Accounts Receivables and its Effect on Hardware Store PerformanceJobelle MalabananNo ratings yet

- MGMT 540 Midterm Exam ReviewDocument9 pagesMGMT 540 Midterm Exam Reviewliu anNo ratings yet

- Service Rate 3 Minutes/call or 10 Calls/30 minutes/CSR Utilization (U) Demand Rate/ ( (Service Rate) (Number of Servers) )Document8 pagesService Rate 3 Minutes/call or 10 Calls/30 minutes/CSR Utilization (U) Demand Rate/ ( (Service Rate) (Number of Servers) )Nilisha DeshbhratarNo ratings yet

- Factors Affecting Accounting Students in Choosing Accounting Career PathDocument14 pagesFactors Affecting Accounting Students in Choosing Accounting Career PathGONZALES CamilleNo ratings yet

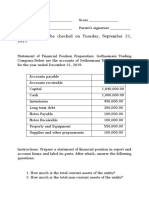

- Answer This To Be Checked On Tuesday, September 21, 2021Document2 pagesAnswer This To Be Checked On Tuesday, September 21, 2021Teresa Mae OrquiaNo ratings yet

- Obedelicious Prime's Foodflix Business Simulation Accomplishment ReportDocument37 pagesObedelicious Prime's Foodflix Business Simulation Accomplishment ReportEricka DeguzmanNo ratings yet

- FAR 2 NotesDocument3 pagesFAR 2 NotesMARK RANIEL ANTAZONo ratings yet

- CHAPTER 6 - 1 Cash and Marketable SecuritiesDocument15 pagesCHAPTER 6 - 1 Cash and Marketable SecuritiesAhmad Ridhuwan AbdullahNo ratings yet

- 22 Finance Company OperationsDocument18 pages22 Finance Company OperationsPaula Ella BatasNo ratings yet

- Lab Posttest 1 - The Accounting Equation and The Double Entry SystemDocument1 pageLab Posttest 1 - The Accounting Equation and The Double Entry SystemRaymond PacaldoNo ratings yet

- Reading 19: Introduction To Financial Statement AnalysisDocument43 pagesReading 19: Introduction To Financial Statement AnalysisAlex PaulNo ratings yet

- Financial Reporting EssentialsDocument20 pagesFinancial Reporting EssentialsAnastasha Grey100% (1)

- Lesson 1 Statement of Financial PositionDocument22 pagesLesson 1 Statement of Financial PositionMylene SantiagoNo ratings yet

- Introduction to Accounting Fundamentals Practice TestDocument4 pagesIntroduction to Accounting Fundamentals Practice TestNorie EcijaNo ratings yet

- A Cool Escape To BaguioDocument16 pagesA Cool Escape To BaguioMaria Lourdes Christina.No ratings yet

- This Study Resource Was: Discussion QuestionsDocument2 pagesThis Study Resource Was: Discussion QuestionsitsmenatoyNo ratings yet

- Understanding Formal Institutions - Politics, Laws and EconomicsDocument4 pagesUnderstanding Formal Institutions - Politics, Laws and EconomicsLeoncio BocoNo ratings yet

- Business Finance Semi ExamDocument1 pageBusiness Finance Semi ExamAimelenne Jay Aninion100% (1)

- Ethical analysis of a tragic road rage incidentDocument7 pagesEthical analysis of a tragic road rage incidentEzekylah AlbaNo ratings yet

- Lec 5 Variables and IndicatorsDocument12 pagesLec 5 Variables and IndicatorsAbdifatah Muhumed100% (1)

- Activity-Financial AnalysisDocument2 pagesActivity-Financial AnalysisXienaNo ratings yet

- ch04.ppt - Income Statement and Related InformationDocument68 pagesch04.ppt - Income Statement and Related InformationAmir ContrerasNo ratings yet

- Study Note 9.1, Page 647-672Document26 pagesStudy Note 9.1, Page 647-672s4sahithNo ratings yet

- Study Note 9.2, Page 673-680Document8 pagesStudy Note 9.2, Page 673-680s4sahithNo ratings yet

- Study Note 8, Page 565-646Document82 pagesStudy Note 8, Page 565-646s4sahithNo ratings yet

- NewDocument2 pagesNews4sahithNo ratings yet

- Study Note - 7.3, Page 535-541Document7 pagesStudy Note - 7.3, Page 535-541s4sahith100% (1)

- Study Note 5.2 (353-378)Document26 pagesStudy Note 5.2 (353-378)s4sahith100% (1)

- Study Note 7.2, Page 523-534Document12 pagesStudy Note 7.2, Page 523-534s4sahithNo ratings yet

- Study Note - 7.2 Page (509-522)Document14 pagesStudy Note - 7.2 Page (509-522)s4sahithNo ratings yet

- Study Note 5.1 (328-352)Document25 pagesStudy Note 5.1 (328-352)s4sahithNo ratings yet

- Study Note - 7.4, Page 542-564Document23 pagesStudy Note - 7.4, Page 542-564s4sahithNo ratings yet

- Accounting Standards 32Document91 pagesAccounting Standards 32bathinisridhar100% (3)

- Study Note 7.1, Page 470 508Document39 pagesStudy Note 7.1, Page 470 508s4sahithNo ratings yet

- Study Note 4.5, Page (290-327)Document38 pagesStudy Note 4.5, Page (290-327)s4sahith100% (1)

- Study Note 4.2, Page 169-197Document29 pagesStudy Note 4.2, Page 169-197s4sahith0% (1)

- Study Note 4.3, Page 198-263Document66 pagesStudy Note 4.3, Page 198-263s4sahithNo ratings yet

- Study Note 4.1, Page 143-168Document26 pagesStudy Note 4.1, Page 143-168s4sahith40% (5)

- Studdy Note 7Document42 pagesStuddy Note 7s4sahith100% (1)

- Study Note 4.4 Page (264-289)Document26 pagesStudy Note 4.4 Page (264-289)s4sahith75% (24)

- Study Note 1.4, Page 47 59Document13 pagesStudy Note 1.4, Page 47 59s4sahithNo ratings yet

- Study Note 2.2 Page (80-113)Document34 pagesStudy Note 2.2 Page (80-113)s4sahithNo ratings yet

- Study Note 3, Page 114-142Document29 pagesStudy Note 3, Page 114-142s4sahithNo ratings yet

- Studdy Note 8Document59 pagesStuddy Note 8s4sahithNo ratings yet

- Studdy Note 6Document54 pagesStuddy Note 6s4sahithNo ratings yet

- Study Note-1.3, Page 33-46Document14 pagesStudy Note-1.3, Page 33-46s4sahithNo ratings yet

- Studdy Note 9Document19 pagesStuddy Note 9s4sahithNo ratings yet

- Study Bote-1.1, Page 1-11Document11 pagesStudy Bote-1.1, Page 1-11s4sahithNo ratings yet

- Studdy Note 5Document22 pagesStuddy Note 5s4sahithNo ratings yet

- Front PageDocument2 pagesFront Pages4sahithNo ratings yet

- Bank Statement IndusindDocument28 pagesBank Statement IndusindRohit RajagopalNo ratings yet

- Ignou Eco - 2 Solved Assignment 218-19Document34 pagesIgnou Eco - 2 Solved Assignment 218-19NEW THINK CLASSESNo ratings yet

- 5 5Document7 pages5 5Evelyn MorilloNo ratings yet

- Karkits Corporation PDFDocument4 pagesKarkits Corporation PDFRachel LeachonNo ratings yet

- Chapter 3 The Double-Entry System: Discussion QuestionsDocument16 pagesChapter 3 The Double-Entry System: Discussion QuestionskietNo ratings yet

- Z.A.Corporation (PVT) LTD Spinning Unit: 50-010-0001 Account # Cash in HandDocument28 pagesZ.A.Corporation (PVT) LTD Spinning Unit: 50-010-0001 Account # Cash in HandArslan NisarNo ratings yet

- The Activities of the Accounts Department at Green Peak Holdings LtdDocument47 pagesThe Activities of the Accounts Department at Green Peak Holdings LtdRishav PrasadNo ratings yet

- Lesson Plan Grade 11: Department of EducationDocument3 pagesLesson Plan Grade 11: Department of EducationMary Grace Pagalan LadaranNo ratings yet

- MAS 2nd Monthly AssessmentDocument11 pagesMAS 2nd Monthly AssessmentCiena Mae AsasNo ratings yet

- Computer Application II Certificate NotesDocument102 pagesComputer Application II Certificate NotesJoy KananuNo ratings yet

- Accounting 202 Notes - David HornungDocument28 pagesAccounting 202 Notes - David HornungAvi Goodstein100% (1)

- Pors 1 04-Dec-2012 Policy & OthersDocument110 pagesPors 1 04-Dec-2012 Policy & OthersKartik GoyalNo ratings yet

- AnaCredit Manual Part II Datasets and Data Attributes - enDocument275 pagesAnaCredit Manual Part II Datasets and Data Attributes - ensgjatharNo ratings yet

- Papjdm Tugas 5-1Document17 pagesPapjdm Tugas 5-1lizaNo ratings yet

- Introduction to Accounting BasicsDocument14 pagesIntroduction to Accounting BasicsJunaid IslamNo ratings yet

- Expanded Accounting EquationDocument18 pagesExpanded Accounting EquationBelen GonzalesNo ratings yet

- PGT CommerceDocument33 pagesPGT CommerceSanjiv GautamNo ratings yet

- University of Zambia financial accounting assignmentDocument4 pagesUniversity of Zambia financial accounting assignmentNguvuluNo ratings yet

- Muhammad ShoaibDocument2 pagesMuhammad ShoaibHammad AslamNo ratings yet

- PDF SYBCom - F Div - Paper AFM IIIDocument16 pagesPDF SYBCom - F Div - Paper AFM IIIPushkar DereNo ratings yet