You might also like

- Financial Institution Fraud 2013 - Chapter ExcerptDocument15 pagesFinancial Institution Fraud 2013 - Chapter ExcerptLeynard ColladoNo ratings yet

- Ranco Costa Verda ContractDocument21 pagesRanco Costa Verda ContractGregory RussellNo ratings yet

- City of Minneapolis MPD Correspondence With MDHRDocument11 pagesCity of Minneapolis MPD Correspondence With MDHRScott JohnsonNo ratings yet

- ThePurpleLotus - Wattigney InformationDocument6 pagesThePurpleLotus - Wattigney InformationDeepDotWeb.comNo ratings yet

- Trakas LetterDocument3 pagesTrakas LetterMonica Celeste RyanNo ratings yet

- Letter To Police Re Volunteer Informant Mario ArenasDocument2 pagesLetter To Police Re Volunteer Informant Mario ArenasJames Alan BushNo ratings yet

- Government's Sentencing Memorandum For Steve StengerDocument12 pagesGovernment's Sentencing Memorandum For Steve StengerKelsi AndersonNo ratings yet

- JUUL Medical Authorization Packet - Tarek WegDocument4 pagesJUUL Medical Authorization Packet - Tarek WegTed RustNo ratings yet

- Financial CrisisDocument6 pagesFinancial CrisisForeclosure Fraud100% (1)

- Consumer Authorization Background Check FormDocument2 pagesConsumer Authorization Background Check Formapi-351412138No ratings yet

- #GoldenGoFer IndictmentDocument67 pages#GoldenGoFer IndictmentMichael_Lee_RobertsNo ratings yet

- Indictments Unsealed AlleginDocument5 pagesIndictments Unsealed AlleginVictoria MartinNo ratings yet

- Benefit Summary RPTDocument2 pagesBenefit Summary RPTJonathan LipscombNo ratings yet

- Emergency Motion Rechnitz Response-8!29!14Document75 pagesEmergency Motion Rechnitz Response-8!29!14Linda GonzalesNo ratings yet

- ALAN-I GOLDBERG Initial Disclosure 2015 06-17-5581e6768e791Document77 pagesALAN-I GOLDBERG Initial Disclosure 2015 06-17-5581e6768e791ALAN I GOLDBERGNo ratings yet

- Background Investigation FormDocument5 pagesBackground Investigation FormWDAScribdNo ratings yet

- Erby PetitionDocument9 pagesErby PetitionJordan PalmerNo ratings yet

- CC 081213 Dept 14 Lapp LDocument38 pagesCC 081213 Dept 14 Lapp LJudicial Watch, Inc.No ratings yet

- Plaintiff's Opposition On Preservation of Talc SamplesDocument26 pagesPlaintiff's Opposition On Preservation of Talc SamplesKirk HartleyNo ratings yet

- Walton Development, Tanzania Jesuits & Grupo AlcoDocument10 pagesWalton Development, Tanzania Jesuits & Grupo AlcoDavid LangerNo ratings yet

- View Completed FormsDocument13 pagesView Completed FormsKewan WNo ratings yet

- PUBLIC Order For Preparation Release of Transcript Record of Grand JuryDocument4 pagesPUBLIC Order For Preparation Release of Transcript Record of Grand Jurykc wildmoon100% (1)

- Brewer Federal WarrantDocument13 pagesBrewer Federal WarrantMegan Strickland SacryNo ratings yet

- People of The State of Illinois vs. Anthony McKinney - The People's Supplemental Response To The Motion To QuashDocument54 pagesPeople of The State of Illinois vs. Anthony McKinney - The People's Supplemental Response To The Motion To QuashChicago TribuneNo ratings yet

- Medina Arrest WarrantDocument5 pagesMedina Arrest WarrantAlfonso RobinsonNo ratings yet

- Criminal Complaint Filed Against Tarrant County College District With The District Attorney's OfficeDocument18 pagesCriminal Complaint Filed Against Tarrant County College District With The District Attorney's OfficeIsaiah X. SmithNo ratings yet

- Regina R Ross-1ab65dfcfca54a7 PDFDocument21 pagesRegina R Ross-1ab65dfcfca54a7 PDFGlenn ColemanNo ratings yet

- Group List of Extra Scrutiny Targets by IRSDocument10 pagesGroup List of Extra Scrutiny Targets by IRSAnonymous kprzCiZNo ratings yet

- Irs General Criminal Tax Fraud & Tax Evasion Prosecution Summaries Fy 2008-2010 - A Review For South Carolina Criminal Tax Attorneys, Lawyers & Law FirmsDocument201 pagesIrs General Criminal Tax Fraud & Tax Evasion Prosecution Summaries Fy 2008-2010 - A Review For South Carolina Criminal Tax Attorneys, Lawyers & Law FirmsJoseph P. Griffith, Jr.No ratings yet

- Strongest and Weakest Banks and ThriftsDocument108 pagesStrongest and Weakest Banks and ThriftsMayur MahajanNo ratings yet

- 15-0564 - Viramontes Summary Report FINALDocument20 pages15-0564 - Viramontes Summary Report FINALTodd FeurerNo ratings yet

- Michael Richo Criminal ComplaintDocument16 pagesMichael Richo Criminal ComplaintSoftpedia100% (1)

- Corporate Fraud and Employee Theft: Impacts and Costs On BusinessDocument15 pagesCorporate Fraud and Employee Theft: Impacts and Costs On BusinessAkuw AjahNo ratings yet

- Congressmen Home Addresses PDFDocument27 pagesCongressmen Home Addresses PDFProfessor WatchlistNo ratings yet

- SCS 200 Research Check 2Document6 pagesSCS 200 Research Check 2Robin McFaddenNo ratings yet

- Michael and Julie Mardock v. Michael and Virginia McClaughryDocument17 pagesMichael and Julie Mardock v. Michael and Virginia McClaughryThe Department of Official InformationNo ratings yet

- Adding The PPS Credential To Your Master-2Document4 pagesAdding The PPS Credential To Your Master-2CSUFCounselorEdNo ratings yet

- Basic Income and Sovereign Money: The Alternative to Economic Crisis and Austerity PolicyFrom EverandBasic Income and Sovereign Money: The Alternative to Economic Crisis and Austerity PolicyNo ratings yet

- Please DocuSign These Documents UPS On-BoardDocument21 pagesPlease DocuSign These Documents UPS On-BoardJayeven EnglishNo ratings yet

- Completed Unclaimed Prop Dec20 - 202101141120520671Document692 pagesCompleted Unclaimed Prop Dec20 - 202101141120520671Naberius Customs LLCNo ratings yet

- How To Get What The US Government Owes You!Document4 pagesHow To Get What The US Government Owes You!creativemarcoNo ratings yet

- Https WWW - Dol.state - Ga.us WS4-MW5 CicsDocument4 pagesHttps WWW - Dol.state - Ga.us WS4-MW5 CicsDaniel MinnickNo ratings yet

- One SiteDocument2 pagesOne SiteVanessa Burbano AyalaNo ratings yet

- Background Search Clarence Jonathan WoodDocument20 pagesBackground Search Clarence Jonathan Woodkerry campbellNo ratings yet

- Transcript of The Hearing in The Mifepristone Lawsuit On March 14, 2023 in Amarillo, TexasDocument22 pagesTranscript of The Hearing in The Mifepristone Lawsuit On March 14, 2023 in Amarillo, TexasJamie BurchNo ratings yet

- Criminal Complaint Against Former San Bernardino County Assessor Bill PostmusDocument5 pagesCriminal Complaint Against Former San Bernardino County Assessor Bill PostmusThe Press-Enterprise / pressenterprise.comNo ratings yet

- Borland-Clifford House NominationDocument19 pagesBorland-Clifford House NominationReno Gazette JournalNo ratings yet

- A Child 3Document50 pagesA Child 3winona mae marzoccoNo ratings yet

- Better Covid ThingDocument4 pagesBetter Covid ThingAuguste RiedlNo ratings yet

- Letter To Police Re Illegal Gambling Operations in San Jose (Leo Rodriguez)Document2 pagesLetter To Police Re Illegal Gambling Operations in San Jose (Leo Rodriguez)James Alan BushNo ratings yet

- PEOPLE FOR THE ETHICAL OPERATION OF PROSECUTORS AND LAW ENFORCEMENT (P.E.O.P.L.E.), BETHANY WEBB, THERESA SMITH, and TINA JACKSON, vs. ANTHONY J. RACKAUCKASDocument40 pagesPEOPLE FOR THE ETHICAL OPERATION OF PROSECUTORS AND LAW ENFORCEMENT (P.E.O.P.L.E.), BETHANY WEBB, THERESA SMITH, and TINA JACKSON, vs. ANTHONY J. RACKAUCKASFindLawNo ratings yet

- Credit OwnDocument1 pageCredit OwnLuis Miguel PedemonteNo ratings yet

- Valuation Form Kirby 2021-05-04-17-01-19 1Document240 pagesValuation Form Kirby 2021-05-04-17-01-19 1La Rams FanNo ratings yet

- Driver License/identification Card and REAL ID ChecklistDocument3 pagesDriver License/identification Card and REAL ID ChecklistMuneeb QayyumNo ratings yet

- Affidavit of Hipkiss vs. ShinDocument26 pagesAffidavit of Hipkiss vs. ShinP-R HipkissNo ratings yet

- Original Social Security Card Back - Google SearchDocument1 pageOriginal Social Security Card Back - Google SearchhannahNo ratings yet

- TRENT COLBY GEERDES ReportDocument36 pagesTRENT COLBY GEERDES ReportYyNo ratings yet

- Emanuel Emails From March 2012 To August 2012Document140 pagesEmanuel Emails From March 2012 To August 2012Steve WarmbirNo ratings yet

- One of The Heavily Redacted State Documents On YouthCare Released by IllinoisDocument83 pagesOne of The Heavily Redacted State Documents On YouthCare Released by IllinoisSteve WarmbirNo ratings yet

- Emanuel Emails 6Document111 pagesEmanuel Emails 6Steve WarmbirNo ratings yet

- Emanuel Emails From February 2014 To September 2014Document99 pagesEmanuel Emails From February 2014 To September 2014Steve WarmbirNo ratings yet

- Emanuel Emails From September 2012 To December 2012Document68 pagesEmanuel Emails From September 2012 To December 2012Steve WarmbirNo ratings yet

- October 2014 Through December 2014Document98 pagesOctober 2014 Through December 2014dnainfojenNo ratings yet

- Emails Regarding SUPES ContractDocument2 pagesEmails Regarding SUPES ContractSteve WarmbirNo ratings yet

- May 2011 Through July 2011.Document159 pagesMay 2011 Through July 2011.dnainfojenNo ratings yet

- November 2011 Through February 2012Document130 pagesNovember 2011 Through February 2012dnainfojenNo ratings yet

- Copa OrdinanceDocument22 pagesCopa OrdinanceSteve WarmbirNo ratings yet

- CPS Inspector General's ReportDocument6 pagesCPS Inspector General's ReportSteve WarmbirNo ratings yet

- Blagojevich en Banc AppealDocument46 pagesBlagojevich en Banc AppealSteve WarmbirNo ratings yet

- August 2011 Through October 2011Document126 pagesAugust 2011 Through October 2011dnainfojenNo ratings yet

- Aldo Brown Criminal ComplaintDocument5 pagesAldo Brown Criminal ComplaintSteve WarmbirNo ratings yet

- Federal Appellate RulingDocument1 pageFederal Appellate RulingSteve WarmbirNo ratings yet

- CTU Report On Special Ed CutsDocument8 pagesCTU Report On Special Ed CutsSteve WarmbirNo ratings yet

- Sentencing Memo For Steven ZamiarDocument19 pagesSentencing Memo For Steven ZamiarSteve WarmbirNo ratings yet

- Brian Howard PleaDocument18 pagesBrian Howard PleaSteve WarmbirNo ratings yet

- Parcc Prelim State LVL Results 4Document1 pageParcc Prelim State LVL Results 4Steve WarmbirNo ratings yet

- 2016 Budget AddressDocument10 pages2016 Budget AddressCrainsChicagoBusinessNo ratings yet

- NLRB OpinionDocument19 pagesNLRB OpinionAnonymous 6f8RIS6No ratings yet

- CPS Bell Times Change in Policy 081015Document5 pagesCPS Bell Times Change in Policy 081015Chicago Alderman Scott WaguespackNo ratings yet

- Bibbs Complaint FiledDocument30 pagesBibbs Complaint FiledSteve WarmbirNo ratings yet

- Vaughan Plea AgreementDocument16 pagesVaughan Plea AgreementSteve WarmbirNo ratings yet

- Pension RulingDocument35 pagesPension RulingSteve WarmbirNo ratings yet

- Back Page OrderDocument2 pagesBack Page OrderSteve WarmbirNo ratings yet

- Warner 7th Cir July 10 2015 (Sentence Affirmed)Document33 pagesWarner 7th Cir July 10 2015 (Sentence Affirmed)Steve WarmbirNo ratings yet

- Rod Blagojevich RulingDocument23 pagesRod Blagojevich RulingSteve WarmbirNo ratings yet

- CPS School BudgetsDocument32 pagesCPS School BudgetsSteve WarmbirNo ratings yet

- Current Account Statement: United Bank LimitedDocument1 pageCurrent Account Statement: United Bank LimitedkarinaNo ratings yet

- Dec - 21Document17 pagesDec - 21Amit KumarNo ratings yet

- Object Oriented System Analysis and Design (Oosad) INSY3063: Prepared by Meseret Hailu (2022) 1 5/31/2022Document151 pagesObject Oriented System Analysis and Design (Oosad) INSY3063: Prepared by Meseret Hailu (2022) 1 5/31/2022taye teferaNo ratings yet

- Sudhir Kumar 6m Axis FundsDocument2 pagesSudhir Kumar 6m Axis FundsSajan SharmaNo ratings yet

- A STUDY of NPA ProjectDocument74 pagesA STUDY of NPA ProjectAman RajakNo ratings yet

- Project Report On ATM SystemDocument55 pagesProject Report On ATM SystemJaydip Patel100% (3)

- Working of ATMDocument3 pagesWorking of ATMNarendran SrinivasanNo ratings yet

- Axis Bank FinalDocument109 pagesAxis Bank Finalashu1630100% (9)

- MX8700 1Document2 pagesMX8700 1MariyappanSubhash100% (1)

- Chasebankusanationalassociation 489913 Wilmingtondelaware 19Document39 pagesChasebankusanationalassociation 489913 Wilmingtondelaware 19Efrain CabreraNo ratings yet

- Case Study: ATM Machine II: Identifying Class AttributesDocument16 pagesCase Study: ATM Machine II: Identifying Class AttributesCharmi yantinaNo ratings yet

- NBP Bank ChargesDocument28 pagesNBP Bank Chargesayub_balticNo ratings yet

- 05 Ooad-Uml 05Document27 pages05 Ooad-Uml 05Hiren BhingaradiyaNo ratings yet

- Annual Report 2010 2011 PDFDocument31 pagesAnnual Report 2010 2011 PDFbekele abomsaNo ratings yet

- Tax Return Receipt ConfirmationDocument5 pagesTax Return Receipt ConfirmationAntoni Boyd Montejo AlicanteNo ratings yet

- Sagicor Bank Account Terms and Conditions July 27 2020Document9 pagesSagicor Bank Account Terms and Conditions July 27 2020Maxwell R. SmithNo ratings yet

- Mod 1 Mbfs PDF NewDocument22 pagesMod 1 Mbfs PDF NewWalidahmad AlamNo ratings yet

- ATM MachineDocument19 pagesATM MachinevaishalisamNo ratings yet

- FBL (Final)Document88 pagesFBL (Final)Muhammad Rizwan KhanNo ratings yet

- Paket Full 4 StudentDocument5 pagesPaket Full 4 Studentdara mudaNo ratings yet

- Money and Banking TerminologyDocument3 pagesMoney and Banking TerminologythamiztNo ratings yet

- AccDocument7 pagesAccALLIA AHMADNo ratings yet

- Account Statement As of 15-06-2019 14:28:53 GMT +0530 Customer Name Branch Account Number Customer Id Account Currency Opening Balance Closing BalanceDocument11 pagesAccount Statement As of 15-06-2019 14:28:53 GMT +0530 Customer Name Branch Account Number Customer Id Account Currency Opening Balance Closing BalanceNIMMANAGANTI RAMAKRISHNANo ratings yet

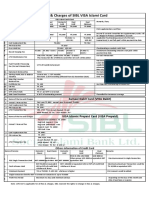

- Fees and Charges of SIBL Islami CardDocument1 pageFees and Charges of SIBL Islami CardMd YusufNo ratings yet

- Checking Account Simulation Powerpoint Presentation 171g1Document77 pagesChecking Account Simulation Powerpoint Presentation 171g1deepag100% (3)

- At The Bank: Speaking A Word To BeginDocument2 pagesAt The Bank: Speaking A Word To BeginJosé Juan SuárezNo ratings yet

- Deposita BrochureDocument2 pagesDeposita BrochuresafinditNo ratings yet

- Soneri Bank Report CompressDocument66 pagesSoneri Bank Report Compressناظم راجپوت بھٹیNo ratings yet

- Case 12 Menton BankDocument2 pagesCase 12 Menton BankJi Jason100% (1)

- Retail 2Document32 pagesRetail 2Pravali SaraswatNo ratings yet