You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Chap1-Geometrical Optics - ExercisesDocument3 pagesChap1-Geometrical Optics - ExercisesReema HlohNo ratings yet

- Active Control of Flow Separation Over An Airfoil Using Synthetic JetsDocument9 pagesActive Control of Flow Separation Over An Airfoil Using Synthetic JetsDrSrujana ReddyNo ratings yet

- Design Rules CMOS Transistor LayoutDocument7 pagesDesign Rules CMOS Transistor LayoututpalwxyzNo ratings yet

- QUICK GUIDE ON WRITING PATENT SPECIFICATION v1Document37 pagesQUICK GUIDE ON WRITING PATENT SPECIFICATION v1Muhammad Azuan TukiarNo ratings yet

- Product Data Sheet: Linear Switch - iSSW - 2 C/O - 20A - 250 V AC - 3 PositionsDocument2 pagesProduct Data Sheet: Linear Switch - iSSW - 2 C/O - 20A - 250 V AC - 3 PositionsMR. TNo ratings yet

- Axial Shortening of Column in Tall Structure.Document9 pagesAxial Shortening of Column in Tall Structure.P.K.Mallick100% (1)

- Industrial HygieneDocument31 pagesIndustrial HygieneGautam SharmaNo ratings yet

- PMO ProceduresDocument21 pagesPMO ProceduresTariq JamalNo ratings yet

- Strength of A440 Steel Joints Connected With A325 Bolts PublicatDocument52 pagesStrength of A440 Steel Joints Connected With A325 Bolts Publicathal9000_mark1No ratings yet

- MTBE Presintation For IMCODocument26 pagesMTBE Presintation For IMCOMaryam AlqasimyNo ratings yet

- JonWeisseBUS450 04 HPDocument3 pagesJonWeisseBUS450 04 HPJonathan WeisseNo ratings yet

- SI Units in Geotechnical EngineeringDocument7 pagesSI Units in Geotechnical EngineeringfaroeldrNo ratings yet

- Brigada Eskwela Activities With PicsDocument6 pagesBrigada Eskwela Activities With PicsCharisse TocmoNo ratings yet

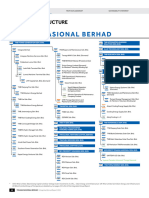

- TNB AR 2022 Corporate StructureDocument2 pagesTNB AR 2022 Corporate StructureZamzuri P AminNo ratings yet

- Manual Instalaciones Electricas para Centros de ComputoDocument65 pagesManual Instalaciones Electricas para Centros de ComputoJorge Estrada0% (3)

- JEDI Slides Intro1 Chapter 02 Introduction To JavaDocument17 pagesJEDI Slides Intro1 Chapter 02 Introduction To JavaredbutterflyNo ratings yet

- Inspection and Maintenance of Drillpipe Ebook PDFDocument39 pagesInspection and Maintenance of Drillpipe Ebook PDFAntónio OliveiraNo ratings yet

- 2 Biogas Kristianstad Brochure 2009Document4 pages2 Biogas Kristianstad Brochure 2009Baris SamirNo ratings yet

- SPW3 Manual Rev 5Document713 pagesSPW3 Manual Rev 5JPYadavNo ratings yet

- Masterseal 550Document4 pagesMasterseal 550Arjun MulluNo ratings yet

- DS450 Shop Manual (Prelim)Document94 pagesDS450 Shop Manual (Prelim)GuruRacerNo ratings yet

- Teradata Version DifferencesDocument3 pagesTeradata Version DifferencesShambuReddy100% (1)

- 21st Bomber Command Tactical Mission Report 146, OcrDocument54 pages21st Bomber Command Tactical Mission Report 146, OcrJapanAirRaidsNo ratings yet

- Assign 1Document5 pagesAssign 1Aubrey Camille Cabrera100% (1)

- Air Pak SCBA Ordering Specifications (HS 6701)Document8 pagesAir Pak SCBA Ordering Specifications (HS 6701)QHSE ManagerNo ratings yet

- 176Document3 pages176Karthik AmigoNo ratings yet

- Product Portfolio ManagementDocument10 pagesProduct Portfolio ManagementSandeep Singh RajawatNo ratings yet

- DPWH Standard Specifications for ShotcreteDocument12 pagesDPWH Standard Specifications for ShotcreteDino Garzon OcinoNo ratings yet

- DML Sro Karnal RMSDocument5 pagesDML Sro Karnal RMSEr Rohit MehraNo ratings yet

- Brake Pedals and ValveDocument4 pagesBrake Pedals and Valveala17No ratings yet