You might also like

- MOS FY09 Financial Data PDFDocument9 pagesMOS FY09 Financial Data PDFRafaelKwongNo ratings yet

- Pizza Hutt 2009annualreportDocument220 pagesPizza Hutt 2009annualreportevojulzNo ratings yet

- Ma - Capital Expenditure AnalysisDocument3 pagesMa - Capital Expenditure AnalysisRafaelKwongNo ratings yet

- Management Accounting - Project 1Document7 pagesManagement Accounting - Project 1RafaelKwongNo ratings yet

- MADocument12 pagesMARafaelKwongNo ratings yet

- Case Study (Section 2.4)Document5 pagesCase Study (Section 2.4)RafaelKwongNo ratings yet

- Burger King-10K2009 PDFDocument128 pagesBurger King-10K2009 PDFRafaelKwongNo ratings yet

- Cost Control and AnalysisDocument2 pagesCost Control and AnalysisRafaelKwongNo ratings yet

- Sales ForecastDocument2 pagesSales ForecastRafaelKwongNo ratings yet

- Management Accounting - Project 2Document3 pagesManagement Accounting - Project 2RafaelKwongNo ratings yet

- McDonald's Advertising and Pricing IIDocument2 pagesMcDonald's Advertising and Pricing IIRafaelKwongNo ratings yet

- Competitor AnalysisDocument4 pagesCompetitor AnalysisRafaelKwong100% (1)

- MA DisadvantageDocument1 pageMA DisadvantageRafaelKwongNo ratings yet

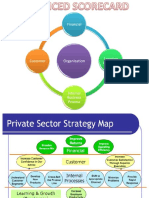

- Balanced Scorecard - Wells Fargo (BUSI0027D) PDFDocument12 pagesBalanced Scorecard - Wells Fargo (BUSI0027D) PDFRafaelKwong50% (4)

- MA Project 2 - McDonaldsDocument11 pagesMA Project 2 - McDonaldsRafaelKwongNo ratings yet

- MA Presentation Slide Finalized - PPSXDocument33 pagesMA Presentation Slide Finalized - PPSXRafaelKwongNo ratings yet

- Inventory Management of McDonald'sDocument2 pagesInventory Management of McDonald'sRafaelKwongNo ratings yet

- Advantages of Balanced ScorecardDocument1 pageAdvantages of Balanced ScorecardRafaelKwongNo ratings yet

- Budgeted Balance SheetDocument2 pagesBudgeted Balance SheetRafaelKwongNo ratings yet

- Income Statement NeatDocument2 pagesIncome Statement NeatRafaelKwongNo ratings yet

- Cash BudgetDocument1 pageCash BudgetRafaelKwongNo ratings yet

- McDonald's Industry, Competitor and Marketing AnalysisDocument20 pagesMcDonald's Industry, Competitor and Marketing AnalysisRafaelKwongNo ratings yet

- IS PictureDocument1 pageIS PictureRafaelKwongNo ratings yet

- Taxation Q21 Handout v3 PDFDocument11 pagesTaxation Q21 Handout v3 PDFRafaelKwongNo ratings yet

- 1011 Group Project AssignmentDocument1 page1011 Group Project AssignmentRafaelKwongNo ratings yet

- Management Accounting - Project 2Document3 pagesManagement Accounting - Project 2RafaelKwongNo ratings yet

- Mini Interview Instruction SheetDocument2 pagesMini Interview Instruction SheetRafaelKwongNo ratings yet

- Chapter 16 LeadershipDocument18 pagesChapter 16 LeadershipRafaelKwongNo ratings yet

- Answers For Question 2Document1 pageAnswers For Question 2RafaelKwongNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Lesson 6 Joint Solidary ObligationsDocument26 pagesLesson 6 Joint Solidary ObligationsJoseph Santos Gacayan100% (1)

- Court denies damages in easement disputeDocument2 pagesCourt denies damages in easement disputelil userNo ratings yet

- C.F. Sharp Crew Management Inc. vs. Espanol, Et. Al, G.R. No. 155903, September 14, 2007Document20 pagesC.F. Sharp Crew Management Inc. vs. Espanol, Et. Al, G.R. No. 155903, September 14, 2007Jana GonzalezNo ratings yet

- TAX 2 v2Document339 pagesTAX 2 v2Stephanie PeraltaNo ratings yet

- Raise The Age Letter To Gov Hochul 2022 08 10Document33 pagesRaise The Age Letter To Gov Hochul 2022 08 10Steven GetmanNo ratings yet

- Human Rights and Gun ConfiscationDocument43 pagesHuman Rights and Gun ConfiscationDebra KlyneNo ratings yet

- Vincent Gagliardi and Sally Gagliardi v. The Village of Pawling Joseph Governale Louis Musella Thomas Sage Darrell Dumas Robert Nielsen, Individually and as Members of the Board of Appeals of Pawling the Board of Appeals of the Village of Pawling the Planning Board of the Village of Pawling the Board of Trustees of the Village of Pawling Bluford Jackson, Building Inspector of the Village of Pawling, Lumelite Corporation, 18 F.3d 188, 2d Cir. (1994)Document12 pagesVincent Gagliardi and Sally Gagliardi v. The Village of Pawling Joseph Governale Louis Musella Thomas Sage Darrell Dumas Robert Nielsen, Individually and as Members of the Board of Appeals of Pawling the Board of Appeals of the Village of Pawling the Planning Board of the Village of Pawling the Board of Trustees of the Village of Pawling Bluford Jackson, Building Inspector of the Village of Pawling, Lumelite Corporation, 18 F.3d 188, 2d Cir. (1994)Scribd Government DocsNo ratings yet

- Labor Law Bar Exam Questions (2006)Document4 pagesLabor Law Bar Exam Questions (2006)Joshua Became A CatNo ratings yet

- 2014 LHC 7323Document14 pages2014 LHC 7323KhaliqNo ratings yet

- Special AppearanceDocument8 pagesSpecial AppearanceApril Clay100% (5)

- Vishal Income Tax NoticeDocument4 pagesVishal Income Tax NoticePriyank SisodiaNo ratings yet

- Vendor CA 587 - Non-ResidentDocument3 pagesVendor CA 587 - Non-ResidentЛена КиселеваNo ratings yet

- The Loans For Agricultural, Commercial and IndustrialDocument5 pagesThe Loans For Agricultural, Commercial and IndustrialShahidHussainBashoviNo ratings yet

- US V Tan PiacoDocument3 pagesUS V Tan PiacoCastle CastellanoNo ratings yet

- When Civil Action May Be Consolidated With Subsequent Criminal Action - Case No. 4Document1 pageWhen Civil Action May Be Consolidated With Subsequent Criminal Action - Case No. 4Khaiye De Asis AggabaoNo ratings yet

- Motion For Joint Administration of Entities Doc 3Document12 pagesMotion For Joint Administration of Entities Doc 3Dentist The MenaceNo ratings yet

- Provincial Assessor of Agusan Del Sur V. Filipinas Palm Oil Plantation G.R. NO 183416, OCTOBER 5, 2016 (Leonen, J.) DoctrineDocument4 pagesProvincial Assessor of Agusan Del Sur V. Filipinas Palm Oil Plantation G.R. NO 183416, OCTOBER 5, 2016 (Leonen, J.) DoctrineCharlene MillaresNo ratings yet

- An Application For Succession CertificateDocument2 pagesAn Application For Succession CertificatePalash Banerjee100% (2)

- Pro Se HandbookDocument60 pagesPro Se HandbookA JohnsonNo ratings yet

- Supreme Court of the Philippines upholds termination of insurance agentDocument11 pagesSupreme Court of the Philippines upholds termination of insurance agentJaycil GaaNo ratings yet

- Mrx. Ruth Brockman Cain, of The Estate of William Pinckney Cain, Deceased v. John H. Beecher, and Little John Beecher & His Orchestra, Inc., 310 F.2d 241, 4th Cir. (1962)Document4 pagesMrx. Ruth Brockman Cain, of The Estate of William Pinckney Cain, Deceased v. John H. Beecher, and Little John Beecher & His Orchestra, Inc., 310 F.2d 241, 4th Cir. (1962)Scribd Government DocsNo ratings yet

- Rivera Iii V Comelec (1991) : Term Limits - Sandoval-Gutierrez, J. - G.R. No. 167591, G.R. No. 170577Document2 pagesRivera Iii V Comelec (1991) : Term Limits - Sandoval-Gutierrez, J. - G.R. No. 167591, G.R. No. 170577Chelle BelenzoNo ratings yet

- Land Laws (Mid Notes)Document18 pagesLand Laws (Mid Notes)Sadaqat UllahNo ratings yet

- Selegna Management and Development Corp. v. UCPB, GR 165662, May 3, 2006, 489 SCRA 125Document1 pageSelegna Management and Development Corp. v. UCPB, GR 165662, May 3, 2006, 489 SCRA 125Gia Dimayuga100% (1)

- BOC Vs DevanaderaDocument19 pagesBOC Vs DevanaderamarvinNo ratings yet

- Hornilla vs. SalunatDocument8 pagesHornilla vs. SalunatJustine Claire RicoNo ratings yet

- FAA Code of EngagementDocument33 pagesFAA Code of EngagementViliame CawaruNo ratings yet

- 017-People v. AlmazanDocument2 pages017-People v. AlmazanJanineNo ratings yet

- Due Care and Information Asymmetry in Financial AdviceDocument47 pagesDue Care and Information Asymmetry in Financial AdviceDuankai LinNo ratings yet

- Labor Relations Book 5Document36 pagesLabor Relations Book 5Jerry Barad Sario100% (1)