You might also like

- Boisdale Cocktail List 2010 3rdDocument56 pagesBoisdale Cocktail List 2010 3rdAditya JagtapNo ratings yet

- AK Adak (Aug14)Document2 pagesAK Adak (Aug14)Aditya JagtapNo ratings yet

- Study of Home Loan Appraisal ProcessDocument4 pagesStudy of Home Loan Appraisal ProcessAditya JagtapNo ratings yet

- There Are Two Types of Teaching PrinciplesDocument4 pagesThere Are Two Types of Teaching PrinciplesAditya Jagtap33% (3)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Case 2 LinkedIn and Modern Recruitment - 5 - 6 - 920220720193429Document16 pagesCase 2 LinkedIn and Modern Recruitment - 5 - 6 - 920220720193429Isha AggarwalNo ratings yet

- Build Home September 2017Document148 pagesBuild Home September 2017meddy100% (2)

- CH 03 Financial Statements ExercisesDocument39 pagesCH 03 Financial Statements ExercisesJocelyneKarolinaArriagaRangel100% (1)

- Predictive AnalyticsDocument3 pagesPredictive AnalyticsAmir KhanNo ratings yet

- 07.) Arya Kusuma XII AKL 1 Lembar Kerja Buku Besar PT MargatapaDocument4 pages07.) Arya Kusuma XII AKL 1 Lembar Kerja Buku Besar PT MargatapaArya KusumaNo ratings yet

- CUSTOMS - ICES Advisory No. 13 - Capturing Additional Details For Certificate of Origin COO in Bil 278269Document2 pagesCUSTOMS - ICES Advisory No. 13 - Capturing Additional Details For Certificate of Origin COO in Bil 278269Kundan YadavNo ratings yet

- COMKA1 Group AssignmentDocument10 pagesCOMKA1 Group AssignmentLouie VillainNo ratings yet

- Sony Company Overview PDFDocument31 pagesSony Company Overview PDFVinay Kalra100% (1)

- Sportswear Industry Targets Untapped 45+ Age Group with Smart Shoe MVPDocument9 pagesSportswear Industry Targets Untapped 45+ Age Group with Smart Shoe MVPNik SatNo ratings yet

- Prepare Project ProposalsDocument2 pagesPrepare Project ProposalsMSWDO STA. MAGDALENANo ratings yet

- LCS Lambton Brochure 2023Document16 pagesLCS Lambton Brochure 2023nobubele masukuNo ratings yet

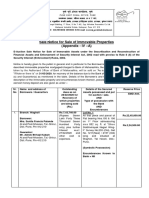

- Sale Notice For Sale of Immovable Properties (Appendix - IV - A)Document7 pagesSale Notice For Sale of Immovable Properties (Appendix - IV - A)Nikhil ShindeNo ratings yet

- Examen 4: 5 Out of 5 PointsDocument5 pagesExamen 4: 5 Out of 5 PointsAngel L Rolon TorresNo ratings yet

- International Business Report on Organizational StructureDocument4 pagesInternational Business Report on Organizational StructureRhein VillasistaNo ratings yet

- Chapter 19 Manajemen Operasi Dan Rantai NilaiDocument23 pagesChapter 19 Manajemen Operasi Dan Rantai Nilainia sania kNo ratings yet

- Adv Strategy IndiaDocument6 pagesAdv Strategy Indiagadgethut360No ratings yet

- Empower Citizen Developers With 3 Data-Driven StepsDocument12 pagesEmpower Citizen Developers With 3 Data-Driven StepsJuan David Gómez ZapataNo ratings yet

- Zanger 1998-02-06Document1 pageZanger 1998-02-06Harvey DychiaoNo ratings yet

- Business Plan (TOW)Document33 pagesBusiness Plan (TOW)patricia yasminNo ratings yet

- AENOR Product Certificate: Façade Scaffolding SystemDocument4 pagesAENOR Product Certificate: Façade Scaffolding SystemJussel Villafuerte AnamariaNo ratings yet

- Group Assignment - Questions - RevisedDocument6 pagesGroup Assignment - Questions - Revised31231023949No ratings yet

- Marketing Management: (Document Subtitle)Document21 pagesMarketing Management: (Document Subtitle)aseni herathNo ratings yet

- Busines Plan-FashiondesignDocument7 pagesBusines Plan-FashiondesignCollins OtienoNo ratings yet

- CHAP-1-Organizational BehaviorDocument34 pagesCHAP-1-Organizational BehaviorYen HoangNo ratings yet

- Audtheo Reviewer 1 PDFDocument8 pagesAudtheo Reviewer 1 PDFmacmac29No ratings yet

- Updated CEMS 5302 BOP Marketing Course Syllabus Fall 2023Document11 pagesUpdated CEMS 5302 BOP Marketing Course Syllabus Fall 2023srmajistoreNo ratings yet

- Impact of Social Media On Consumer BehaviourDocument6 pagesImpact of Social Media On Consumer BehaviourShahzad SaifNo ratings yet

- Beli Tanggal Saham Harga Lot Biaya Fee (0,17%) TotalDocument39 pagesBeli Tanggal Saham Harga Lot Biaya Fee (0,17%) TotalPrihastya WishnutamaNo ratings yet

- 1.0 Segment Market: 1.1 - Identify Criteria For Use in Segmenting Market in Accordance With Marketing PlanDocument23 pages1.0 Segment Market: 1.1 - Identify Criteria For Use in Segmenting Market in Accordance With Marketing PlanMelaii VeeuNo ratings yet

- DESN30117 Pecha Kucha Presentation Template 1Document10 pagesDESN30117 Pecha Kucha Presentation Template 1PaoloNo ratings yet