You might also like

- Beyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkFrom EverandBeyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkNo ratings yet

- Cosmetology & Barber School Revenues World Summary: Market Values & Financials by CountryFrom EverandCosmetology & Barber School Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Income Statement: Presentation and LayoutsDocument4 pagesIncome Statement: Presentation and LayoutsCosmina Andreea ManeaNo ratings yet

- Income Statement: Presentation and LayoutsDocument4 pagesIncome Statement: Presentation and LayoutsCosmina Andreea ManeaNo ratings yet

- Accounting Excercises 2Document13 pagesAccounting Excercises 2Abdallah HassanNo ratings yet

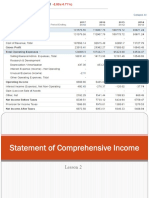

- Lesson 2 Statement of Comprehensive IncomeDocument23 pagesLesson 2 Statement of Comprehensive IncomePaulette Sarno80% (5)

- Basic Finance 19.11Document35 pagesBasic Finance 19.11Cristian VillanuevaNo ratings yet

- Quick Exercise BudgetingDocument5 pagesQuick Exercise Budgetinganand_studyNo ratings yet

- Think of Words That Best Describe Revenues. Expenses Statement of Comprehensive IncomeDocument30 pagesThink of Words That Best Describe Revenues. Expenses Statement of Comprehensive IncomeJasy Nupt GilloNo ratings yet

- Lecture 2Document16 pagesLecture 2hammadNo ratings yet

- Statement of Comprehensive Income (SCI)Document35 pagesStatement of Comprehensive Income (SCI)Jung WonnieNo ratings yet

- Methods of Estimating InventoryDocument46 pagesMethods of Estimating Inventoryone formanyNo ratings yet

- Correct Answers: 7500: CVP Analysis Chapter QuizDocument30 pagesCorrect Answers: 7500: CVP Analysis Chapter QuizABCNo ratings yet

- Mas - ProblemsDocument14 pagesMas - ProblemsIyang LopezNo ratings yet

- Unit 2 - Problem 1Document1 pageUnit 2 - Problem 1Ivana BalijaNo ratings yet

- Managerial Accounting Chapter 5 by GarrisonDocument4 pagesManagerial Accounting Chapter 5 by GarrisonJoshua Hines100% (1)

- Mas 8903 Cost Volume Profit AnalysisDocument9 pagesMas 8903 Cost Volume Profit AnalysisAngel Dela Cruz Co0% (1)

- StratDocument20 pagesStratDhea MaligayaNo ratings yet

- q2 ProbDocument11 pagesq2 ProbGamers HubNo ratings yet

- Joint Cost - Set A - QuestionDocument3 pagesJoint Cost - Set A - QuestionCheliah Mae ImperialNo ratings yet

- SEATWORKDocument4 pagesSEATWORKMarc MagbalonNo ratings yet

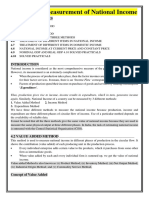

- Ch.4 - Measurement of National Income ( (Macro Economics - 12th Class) ) Green BookDocument120 pagesCh.4 - Measurement of National Income ( (Macro Economics - 12th Class) ) Green BookMayank MallNo ratings yet

- Management Accounting: Live Virtual Class - Session 1Document16 pagesManagement Accounting: Live Virtual Class - Session 1Srinivasan NarasimmanNo ratings yet

- 2012 Final Exam SolutionDocument14 pages2012 Final Exam SolutionOmar Ahmed ElkhalilNo ratings yet

- 3 & 4 - National Income AccountingDocument27 pages3 & 4 - National Income AccountingAshish SinghNo ratings yet

- F3 ACCA Financial Accounting - Inventory by MOCDocument10 pagesF3 ACCA Financial Accounting - Inventory by MOCMunyaradzi Onismas Chinyukwi100% (1)

- Accounting For Raw Material and LaborDocument24 pagesAccounting For Raw Material and LaborAntony HermawanNo ratings yet

- CCA Level 1Document12 pagesCCA Level 1Rob De CastroNo ratings yet

- Strat CostDocument39 pagesStrat Costyen c aNo ratings yet

- Sample Paper Cost & Management Accounting Question BankDocument17 pagesSample Paper Cost & Management Accounting Question BankAnsh Sharma100% (1)

- Quiz For Finals For PrintingDocument4 pagesQuiz For Finals For PrintingPopol KupaNo ratings yet

- Intacc QuizDocument4 pagesIntacc QuizKhamil Kaye GajultosNo ratings yet

- Takehome - Quiz - Manac - Docx Filename - UTF-8''Takehome Quiz Manac-1Document3 pagesTakehome - Quiz - Manac - Docx Filename - UTF-8''Takehome Quiz Manac-1Sharmaine SurNo ratings yet

- Variable Costing vs. Absorption CostingDocument7 pagesVariable Costing vs. Absorption CostingGêmTürÏngånÖNo ratings yet

- Biru Kuning Simpel Abstrak Presentasi Tugas Kelompok - 20231011 - 143052 - 0000Document18 pagesBiru Kuning Simpel Abstrak Presentasi Tugas Kelompok - 20231011 - 143052 - 0000Said BayuNo ratings yet

- (At) 01 - Preface, Framework, EtcDocument8 pages(At) 01 - Preface, Framework, EtcCykee Hanna Quizo LumongsodNo ratings yet

- Cost-Volume Profit AnalysisDocument26 pagesCost-Volume Profit AnalysisClarizza20% (5)

- Final Delivery Blue DolphinDocument8 pagesFinal Delivery Blue DolphinJorge PcNo ratings yet

- Managerial AccountingMid Term ExaminationDocument3 pagesManagerial AccountingMid Term ExaminationjaeNo ratings yet

- Inventory and Cost of Goods Sold Quiz - Accounting CoachDocument3 pagesInventory and Cost of Goods Sold Quiz - Accounting CoachSudip BhattacharyaNo ratings yet

- F2 ACCA Financial Accounting - Inventory by MOCDocument10 pagesF2 ACCA Financial Accounting - Inventory by MOCMunyaradzi Onismas Chinyukwi100% (1)

- Managerial AccountingMid Term Examination (1) - CONSULTADocument7 pagesManagerial AccountingMid Term Examination (1) - CONSULTAMay Ramos100% (1)

- Team 2 - VFood - Expenditure Plan - 15.12Document9 pagesTeam 2 - VFood - Expenditure Plan - 15.12vfoodNo ratings yet

- LT - 081914Document8 pagesLT - 081914Jun Guerzon PaneloNo ratings yet

- Finals Quiz 2Document6 pagesFinals Quiz 2Sevastian jedd EdicNo ratings yet

- EL201 Accounting Learning Module Lessons 51Document19 pagesEL201 Accounting Learning Module Lessons 51keanjervylingonNo ratings yet

- Working Capital, Pricing & Performance Management: Afzal Ahmed, Fca Finance Controller NagadDocument26 pagesWorking Capital, Pricing & Performance Management: Afzal Ahmed, Fca Finance Controller NagadsajedulNo ratings yet

- CH 14Document27 pagesCH 14ReneeNo ratings yet

- Module 2 Productivity and ProfitabilityDocument10 pagesModule 2 Productivity and ProfitabilityAngel HermosisimaNo ratings yet

- Module 2 Productivity and ProfitabilityDocument10 pagesModule 2 Productivity and ProfitabilityJulie Mae TorefielNo ratings yet

- Quiz 1 Cost Accounting FDocument5 pagesQuiz 1 Cost Accounting Fretchiel love calinogNo ratings yet

- Meaning of Cost Sheet:: SampleDocument16 pagesMeaning of Cost Sheet:: SampleSunil Shekhar NayakNo ratings yet

- Ias 16 - Property Plant and Equipment - Revaluations PDFDocument9 pagesIas 16 - Property Plant and Equipment - Revaluations PDFAntora HoqueNo ratings yet

- Gross Profit Net Sales - Cost of Goods Sold Operating Income Gross Profit - Operating Expense Net Income Operating Income + Non Operating ItemsDocument8 pagesGross Profit Net Sales - Cost of Goods Sold Operating Income Gross Profit - Operating Expense Net Income Operating Income + Non Operating ItemsIan VinoyaNo ratings yet

- EL201 Accounting Learning Module Lessons 51Document19 pagesEL201 Accounting Learning Module Lessons 51BabyjoyNo ratings yet

- Profitability Analysis in Simple FinanceDocument9 pagesProfitability Analysis in Simple FinancemonaNo ratings yet

- 8508Document9 pages8508ZunairaAslamNo ratings yet

- Financial Study 107Document22 pagesFinancial Study 107Mariel ManadaoNo ratings yet

- Cost AccountingDocument5 pagesCost Accountingretchiel love calinogNo ratings yet

- ICAEW Financial Accounting Questions March 2015 To March 2016 (SPirate)Document49 pagesICAEW Financial Accounting Questions March 2015 To March 2016 (SPirate)Ahmed Raza Mir100% (4)

- About Research Publications Regions Issues Experts EventsDocument8 pagesAbout Research Publications Regions Issues Experts EventsValentina OlteanuNo ratings yet

- MAIe LectureNotes PM 2017 Part1Document61 pagesMAIe LectureNotes PM 2017 Part1Valentina OlteanuNo ratings yet

- 65453Document491 pages65453Valentina OlteanuNo ratings yet

- Course II "International Financial Markets and Institutions"Document22 pagesCourse II "International Financial Markets and Institutions"Valentina OlteanuNo ratings yet

- Course 6 Econometrics RegressionDocument6 pagesCourse 6 Econometrics RegressionValentina OlteanuNo ratings yet

- Switzerland: Bucharest University of Economic Studies Faculty of International Business and EconomicsDocument6 pagesSwitzerland: Bucharest University of Economic Studies Faculty of International Business and EconomicsValentina OlteanuNo ratings yet

- Discovery of Comparative Advantage - Aldrich 2004Document21 pagesDiscovery of Comparative Advantage - Aldrich 2004Oana CozmaNo ratings yet

- Ludwig Von Mises - Economic PolicyDocument122 pagesLudwig Von Mises - Economic Policynbk13geoNo ratings yet

- Camil PetrescuDocument5 pagesCamil PetrescuValentina OlteanuNo ratings yet

- S2 CS TOCE MapleLeaf 14p Organizational ChartDocument14 pagesS2 CS TOCE MapleLeaf 14p Organizational ChartValentina OlteanuNo ratings yet

- Economic History of World War IIDocument2 pagesEconomic History of World War IIValentina OlteanuNo ratings yet

- Switzerland: Bucharest University of Economic Studies Faculty of International Business and EconomicsDocument6 pagesSwitzerland: Bucharest University of Economic Studies Faculty of International Business and EconomicsValentina OlteanuNo ratings yet

- Ludwig Von Mises - Economic PolicyDocument122 pagesLudwig Von Mises - Economic Policynbk13geoNo ratings yet

- Ludwig Von Mises - Economic PolicyDocument122 pagesLudwig Von Mises - Economic Policynbk13geoNo ratings yet

- 501 Critical Reading QuestionsDocument283 pages501 Critical Reading Questionsapi-3813392100% (9)

- Cost AccountingDocument47 pagesCost AccountingCarlos John Talania 1923No ratings yet

- Inventory ManagementDocument100 pagesInventory Managementgshetty08_966675801No ratings yet

- Group Five Efficient Capital Market TheoryDocument21 pagesGroup Five Efficient Capital Market TheoryAmbrose Ageng'aNo ratings yet

- Reading 32 Introduction To Commodities and Commodity DerivativesDocument5 pagesReading 32 Introduction To Commodities and Commodity Derivativestristan.riolsNo ratings yet

- December 2012 With WatermarkDocument175 pagesDecember 2012 With WatermarkNageswaran GopuNo ratings yet

- Lydia Sumipat v. Brigido BangaDocument2 pagesLydia Sumipat v. Brigido BangaRosanne SoliteNo ratings yet

- IMLI-Marine Insurance LawDocument25 pagesIMLI-Marine Insurance LawHERBERTO PARDONo ratings yet

- A Great Volatility TradeDocument3 pagesA Great Volatility TradeBaljeet SinghNo ratings yet

- HDFC BankDocument78 pagesHDFC Bankinfo.rkvkjalNo ratings yet

- Taxation Law Bar Exam Questions 2011 AnswersDocument14 pagesTaxation Law Bar Exam Questions 2011 AnswersYochabel Eureca BorjeNo ratings yet

- Deepak NitriteDocument169 pagesDeepak NitriteTejendra PatelNo ratings yet

- T MobileDocument1 pageT MobileMelissa AnneNo ratings yet

- Lia Lafico Laico ZawyaDocument4 pagesLia Lafico Laico Zawyaapi-13892656No ratings yet

- HDFC Card DetailsDocument12 pagesHDFC Card DetailsRahul AskNo ratings yet

- Check List LOANDocument12 pagesCheck List LOANshushanNo ratings yet

- Masters VlerickDocument16 pagesMasters VlerickAndree MaldonadoNo ratings yet

- Fake - Fake Money Fake Teachers Fake Assets Robert Kiyosaki Book Novel by WWW - Indianpdf.com - Download PDF Online Free 21 30Document10 pagesFake - Fake Money Fake Teachers Fake Assets Robert Kiyosaki Book Novel by WWW - Indianpdf.com - Download PDF Online Free 21 30hfxNo ratings yet

- Management of Financial ServicesDocument8 pagesManagement of Financial ServicesShikha100% (1)

- Appoinment Letter Gram Sevika 0Document6 pagesAppoinment Letter Gram Sevika 0Deepak PatelNo ratings yet

- Audit Report ResponseDocument15 pagesAudit Report ResponseGOK SpokespersonNo ratings yet

- Case Study South Dakota MicrobreweryDocument1 pageCase Study South Dakota Microbreweryjman02120No ratings yet

- PBCom v. CA, 195 SCRA 567 (1991)Document21 pagesPBCom v. CA, 195 SCRA 567 (1991)inno KalNo ratings yet

- Mutual Fund:: Asset Management CompanyDocument43 pagesMutual Fund:: Asset Management CompanymalaynvNo ratings yet

- CFADocument79 pagesCFATuan TrinhNo ratings yet

- Data ShortDocument5 pagesData Shortgk concepcion0% (1)

- Money (Part II) Please Go Over The Following Terms and Their DefinitionsDocument4 pagesMoney (Part II) Please Go Over The Following Terms and Their DefinitionsDelia LupascuNo ratings yet

- Chapter-1: Submitted By: Bipin SahooDocument48 pagesChapter-1: Submitted By: Bipin SahooAshis Sahoo100% (1)

- Demo 04 - Journal Entries & Ledger Posting & T.B. - Rizvi Co (Compatibility Mode)Document31 pagesDemo 04 - Journal Entries & Ledger Posting & T.B. - Rizvi Co (Compatibility Mode)Evergreen FosterNo ratings yet

- Final Draft - Pleading, Drafting and ConveyancingDocument6 pagesFinal Draft - Pleading, Drafting and ConveyancingMeghna SinghNo ratings yet

- The Garden PlaceDocument2 pagesThe Garden Placeaayushi dubeyNo ratings yet