You might also like

- Third Order Elastic ConstantsDocument3 pagesThird Order Elastic ConstantsElango PaulchamyNo ratings yet

- Fatigue Behavior of Concrete BridgesDocument11 pagesFatigue Behavior of Concrete BridgesElango PaulchamyNo ratings yet

- Concrete Fatigue TestDocument108 pagesConcrete Fatigue TestElango Paulchamy100% (1)

- Settlement ClaimsDocument2 pagesSettlement ClaimsElango PaulchamyNo ratings yet

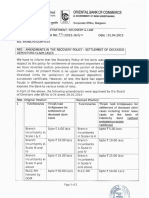

- Oriental Bank interest rates on domestic term depositsDocument1 pageOriental Bank interest rates on domestic term depositsElango PaulchamyNo ratings yet

- Ultrasonic Sensing FundamentalsDocument20 pagesUltrasonic Sensing FundamentalsJagadish_kNo ratings yet

- Concrete Pavements - Journal PaperDocument11 pagesConcrete Pavements - Journal PaperElango PaulchamyNo ratings yet

- Geopolymer Concrete - A New Eco-Friendly Material of ConstructionDocument4 pagesGeopolymer Concrete - A New Eco-Friendly Material of ConstructionElango Paulchamy100% (1)

- Fatigue Behavior of Concrete BridgesDocument11 pagesFatigue Behavior of Concrete BridgesElango PaulchamyNo ratings yet

- Chennai Floods 2015: E. Sakthi Aravind Grade - 8ADocument6 pagesChennai Floods 2015: E. Sakthi Aravind Grade - 8AElango PaulchamyNo ratings yet

- H LoanDocument136 pagesH LoanElango PaulchamyNo ratings yet

- Loan Policy LatestDocument114 pagesLoan Policy LatestElango PaulchamyNo ratings yet

- Effect of Metakaolin Content On The Properties of High Strength ConcreteDocument9 pagesEffect of Metakaolin Content On The Properties of High Strength ConcreteElango PaulchamyNo ratings yet

- Accelerated Curing - Concrete Mix DesignDocument6 pagesAccelerated Curing - Concrete Mix DesignElango PaulchamyNo ratings yet

- Tamil Essay Competition On Smart CityDocument6 pagesTamil Essay Competition On Smart CityElango PaulchamyNo ratings yet

- Highways ResearchDocument175 pagesHighways ResearchElango PaulchamyNo ratings yet

- Presentation 3Document10 pagesPresentation 3Elango PaulchamyNo ratings yet

- IS-456 ACCEPTANCE CRITERIADocument2 pagesIS-456 ACCEPTANCE CRITERIAElango PaulchamyNo ratings yet

- Slot StressDocument1 pageSlot StressElango PaulchamyNo ratings yet

- IS 456 Amendments - 2013 PDFDocument9 pagesIS 456 Amendments - 2013 PDFAshish JainNo ratings yet

- A Review On Use of Metakaolin in Concrete: AbstractDocument6 pagesA Review On Use of Metakaolin in Concrete: AbstractjumahjessiNo ratings yet

- From Ancient Concrete To Geopolymers: Geopolymer InstituteDocument6 pagesFrom Ancient Concrete To Geopolymers: Geopolymer InstituteMithun BMNo ratings yet

- METAKAOLIN BOOSTS CONCRETEDocument4 pagesMETAKAOLIN BOOSTS CONCRETEElango PaulchamyNo ratings yet

- Fatigue Strength of ConcreteDocument59 pagesFatigue Strength of ConcreteElango PaulchamyNo ratings yet

- Robotics ProjectDocument1 pageRobotics ProjectElango PaulchamyNo ratings yet

- Indian ElephantDocument1 pageIndian ElephantElango PaulchamyNo ratings yet

- Uscan: Ultrasonic Detection of Broken WiresDocument1 pageUscan: Ultrasonic Detection of Broken WiresElango PaulchamyNo ratings yet

- Indian ElephantDocument1 pageIndian ElephantElango PaulchamyNo ratings yet

- Gravity of GravityDocument25 pagesGravity of Gravitydrgopibams1100% (1)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- TDS - Manufacturing Crca Welded Ducts. - Kitchen ExhDocument9 pagesTDS - Manufacturing Crca Welded Ducts. - Kitchen ExhSandeep GalhotraNo ratings yet

- Dfpro 4 16 Dust CollectorsDocument10 pagesDfpro 4 16 Dust CollectorsNathanNo ratings yet

- RFP Medical Device Park YeidaDocument53 pagesRFP Medical Device Park YeidaJyoti SwarupNo ratings yet

- Post Graduate StudentDocument5 pagesPost Graduate StudentHatem HusseinNo ratings yet

- Case 5 - DatavisionDocument5 pagesCase 5 - DatavisionSri Nandhni100% (1)

- Heyer SagaDocument575 pagesHeyer SagaTawanannaNo ratings yet

- VSL News 2010 1Document40 pagesVSL News 2010 1DrPadipat ChaemmangkangNo ratings yet

- Gcaug PDFDocument174 pagesGcaug PDFThi NguyenNo ratings yet

- SQL Server Migration Offer DatasheetDocument1 pageSQL Server Migration Offer Datasheetsajal_0171No ratings yet

- EPCM TheMisunderstoodContractDocument6 pagesEPCM TheMisunderstoodContractmonikatickoo4412100% (2)

- CFD Analysis of Static Pressure and Dynamic Pressure For Naca 4412Document8 pagesCFD Analysis of Static Pressure and Dynamic Pressure For Naca 4412seventhsensegroup100% (1)

- Baron 55Document1,113 pagesBaron 55Dú VieiraNo ratings yet

- ACE For IC Business TransactionDocument29 pagesACE For IC Business TransactionnavabhattNo ratings yet

- KP Efisiensi PompaDocument2 pagesKP Efisiensi Pompamuhammad ilhamNo ratings yet

- Contact details of architectural firmsDocument21 pagesContact details of architectural firmsshubhankNo ratings yet

- Conveyor Design PDFDocument73 pagesConveyor Design PDFRamesh Subramani RamachandranNo ratings yet

- Hawker 00XPC LimitationsDocument31 pagesHawker 00XPC LimitationsAngel Abraham Guerrero GarzaNo ratings yet

- Informatica HCLDocument221 pagesInformatica HCLminnusiri100% (1)

- Fork Lift Truck Training BizHouse - UkDocument3 pagesFork Lift Truck Training BizHouse - UkAlex BekeNo ratings yet

- Project Mercury A ChronologyDocument255 pagesProject Mercury A ChronologyBob Andrepont100% (1)

- ASME PTC 22 (1997) Gas Turbines PDFDocument46 pagesASME PTC 22 (1997) Gas Turbines PDFDaniel OrigelNo ratings yet

- Magnet Field v300 Help Manual en PDFDocument474 pagesMagnet Field v300 Help Manual en PDFSami Abdelgadir MohammedNo ratings yet

- Cochin Port Traffic - ProcessDocument6 pagesCochin Port Traffic - ProcessdhinakarajjNo ratings yet

- Titan Support SystemDocument12 pagesTitan Support SystemKovacs Zsolt-IstvanNo ratings yet

- Product Lifecycle Management: UnderstandingDocument20 pagesProduct Lifecycle Management: Understandinganurag_kapila3901No ratings yet

- Improving BOLDFlash's Internal ProcessesDocument10 pagesImproving BOLDFlash's Internal Processessivaabhilash100% (1)

- Eurocell Building Plastics: Specification GuideDocument68 pagesEurocell Building Plastics: Specification GuideWilton Antony QcNo ratings yet

- Underpinning: TypesDocument5 pagesUnderpinning: TypesEnggUsmanZafarNo ratings yet

- SQL Narayana ReddyDocument124 pagesSQL Narayana ReddyTarikh Khan100% (1)

- Sage015061 PDFDocument13 pagesSage015061 PDFaliNo ratings yet