You might also like

- Chapter 4 Practice Exam QuestionsDocument6 pagesChapter 4 Practice Exam QuestionsMd. Saidul IslamNo ratings yet

- Acg 4361 Chapter 17 Study Probes SolutionDocument18 pagesAcg 4361 Chapter 17 Study Probes SolutionPatDabzNo ratings yet

- Chapter 6 Practice QuestionsDocument9 pagesChapter 6 Practice QuestionsAbdul Wajid Nazeer CheemaNo ratings yet

- Departemen A Physical Units Flow Analysis and Cost ReconciliationDocument14 pagesDepartemen A Physical Units Flow Analysis and Cost ReconciliationAnji GoyNo ratings yet

- D. All of The Above Are True.: AMIS 3300 Pop Quiz - Chapter 17Document5 pagesD. All of The Above Are True.: AMIS 3300 Pop Quiz - Chapter 17DIGNA HERNANDEZNo ratings yet

- Quizzes For Finals 1 Compilation Chap6,7,1,2Document35 pagesQuizzes For Finals 1 Compilation Chap6,7,1,2Saeym SegoviaNo ratings yet

- CH 06 Process CostingDocument67 pagesCH 06 Process CostingShannon Bánañas100% (2)

- Holton Tool Company Has Two Departments Assembly and FinishingDocument1 pageHolton Tool Company Has Two Departments Assembly and FinishingAmit PandeyNo ratings yet

- Key answers and process costing calculationsDocument6 pagesKey answers and process costing calculationsJessica Shirl Vipinosa100% (1)

- Process CostingDocument6 pagesProcess CostingLara CelestialNo ratings yet

- IIMV PGP 2021-23 Class Handout on Petrochemical Process CostingDocument6 pagesIIMV PGP 2021-23 Class Handout on Petrochemical Process CostingRitwik MahajanNo ratings yet

- Practice Sheet 3 - CH4 - 4ADocument4 pagesPractice Sheet 3 - CH4 - 4AAhmed HyderNo ratings yet

- Chapter 11Document22 pagesChapter 11Christian Jay S. de la CruzNo ratings yet

- rESEARCH QUESTIONS FbiDocument35 pagesrESEARCH QUESTIONS FbiBOOMERBADNo ratings yet

- P2 BautistaDocument8 pagesP2 BautistaMedalla NikkoNo ratings yet

- 6 2014 Questions and Answers - CompressDocument23 pages6 2014 Questions and Answers - CompressJohn Lloyd CarrilloNo ratings yet

- Finals Exam On Cost Accounting - Set ADocument3 pagesFinals Exam On Cost Accounting - Set ADe Chavez May Ann M.No ratings yet

- Process CostingDocument17 pagesProcess CostingSweta JaiswalNo ratings yet

- Chapter 6 Quiz and AssignmentDocument25 pagesChapter 6 Quiz and AssignmentSaeym SegoviaNo ratings yet

- Chapter 4 Homework QuestionsDocument4 pagesChapter 4 Homework Questionsanon_665127674100% (4)

- CHAPTER 6 - Process Cost Accounting Additional ProcedueDocument28 pagesCHAPTER 6 - Process Cost Accounting Additional Proceduelap91% (11)

- Chapter 4Document14 pagesChapter 4mikeNo ratings yet

- 2011-02-21 011838 CaseyDocument5 pages2011-02-21 011838 CaseyAshish BhallaNo ratings yet

- Additional Examples With Solutions 17Document24 pagesAdditional Examples With Solutions 17Dachi ChaduneliNo ratings yet

- Process-Costing Self-Study-Activity With AnswersDocument9 pagesProcess-Costing Self-Study-Activity With AnswersDane PerezNo ratings yet

- Process Costing-Practice SheetDocument37 pagesProcess Costing-Practice SheetSuvro Avro100% (3)

- Lec3 ProcesscostingDocument25 pagesLec3 Processcostingnathan panNo ratings yet

- ACT3131 - Process Costing ExercisesDocument6 pagesACT3131 - Process Costing ExercisesPrince RyanNo ratings yet

- Process CostingDocument19 pagesProcess CostingmilleranNo ratings yet

- Cost Accounting Chapter 4Document18 pagesCost Accounting Chapter 4Matthew cNo ratings yet

- Chap.14 Guerrero Process CostingQuestionsDocument22 pagesChap.14 Guerrero Process CostingQuestionshoneylove uNo ratings yet

- Mymie B. Maandig MBA-1 Dr. Marco Ilano Problem 4-13A RequiredDocument9 pagesMymie B. Maandig MBA-1 Dr. Marco Ilano Problem 4-13A RequiredMymie MaandigNo ratings yet

- 121 Mt2 Process Cost KeyDocument2 pages121 Mt2 Process Cost KeyMichelle LeeNo ratings yet

- Process Costing Problems 1Document9 pagesProcess Costing Problems 1RoMaNo ratings yet

- Portal Manufacturing Process Costing AnalysisDocument6 pagesPortal Manufacturing Process Costing AnalysisKutlu SaracNo ratings yet

- Weighted Average Method CostingDocument6 pagesWeighted Average Method CostingFirmana PutraNo ratings yet

- Midterm - Ch. 17Document7 pagesMidterm - Ch. 17Cameron BelangerNo ratings yet

- bài tập ktqt chương 2Document10 pagesbài tập ktqt chương 2Liêm PhanNo ratings yet

- 3.4moravia CompanyDocument1 page3.4moravia CompanyGuru Charan ChitikenaNo ratings yet

- Process Costing ProblemsDocument9 pagesProcess Costing ProblemsAries Bautista67% (3)

- 4 5879525209899272176 PDFDocument4 pages4 5879525209899272176 PDFYaredNo ratings yet

- Process Costing 4Document3 pagesProcess Costing 4Mark Michael LegaspiNo ratings yet

- ACCT505 Practice Quiz 1Document6 pagesACCT505 Practice Quiz 1Michael GuyNo ratings yet

- BTVN Chap 4Document4 pagesBTVN Chap 4Hà LêNo ratings yet

- COST ACCOUNTING Final Exam UCPDocument7 pagesCOST ACCOUNTING Final Exam UCPlois martinNo ratings yet

- Job Order and Process CostingDocument13 pagesJob Order and Process CostingAnuar LoboNo ratings yet

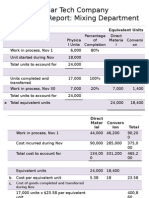

- Solar Tech Company Production Report: Mixing Department: Equivalent UnitsDocument4 pagesSolar Tech Company Production Report: Mixing Department: Equivalent UnitsYen Zi JoyceNo ratings yet

- © The Mcgraw-Hill Companies, Inc., 2005. All Rights Reserved. Solutions Manual, Chapter 4 1Document50 pages© The Mcgraw-Hill Companies, Inc., 2005. All Rights Reserved. Solutions Manual, Chapter 4 1Chiyo MizukiNo ratings yet

- C6 (MC) - Cost Accounting by Carter (Part3)Document5 pagesC6 (MC) - Cost Accounting by Carter (Part3)AkiNo ratings yet

- Chapter 2 Part 2Document6 pagesChapter 2 Part 2Aya MasoudNo ratings yet

- 2311 Acct6131039 Lhfa TK1-W3-S4-R2 Team8Document8 pages2311 Acct6131039 Lhfa TK1-W3-S4-R2 Team8Nadilla NurNo ratings yet

- Exercise 4 ProcesscostingDocument10 pagesExercise 4 ProcesscostingChiyo MizukiNo ratings yet

- Christmas Opening Hours 2014Document1 pageChristmas Opening Hours 2014mingren93No ratings yet

- Ngo ListDocument5 pagesNgo Listmingren93No ratings yet

- ACC103 Q2 (D)Document2 pagesACC103 Q2 (D)mingren93No ratings yet

- Acc103 Assignment Ques3 2013Document4 pagesAcc103 Assignment Ques3 2013mingren93No ratings yet

- ACC103 Q2 (D)Document2 pagesACC103 Q2 (D)mingren93No ratings yet

- Weighted Average Costing of Work in ProcessDocument4 pagesWeighted Average Costing of Work in Processmingren93No ratings yet

- The Effect of International Staffing PracticesDocument25 pagesThe Effect of International Staffing PracticesBryan JiangNo ratings yet

- Buff Dudes 12 Week Workout ProgramDocument8 pagesBuff Dudes 12 Week Workout ProgramPhilip Salmony88% (8)

- CS-LitReview-ExpectancyModelDocument2 pagesCS-LitReview-ExpectancyModelmingren93100% (1)

- Residential Services Student Accommodation Survey 2012: 1. Information Before Arrival Our Students SayDocument7 pagesResidential Services Student Accommodation Survey 2012: 1. Information Before Arrival Our Students Saymingren93No ratings yet

- HR Department Organization QuestionnaireDocument13 pagesHR Department Organization Questionnairepallavi100% (2)

- Aberdeen Research ReportDocument12 pagesAberdeen Research ReportDavid BriggsNo ratings yet

- Project Status Report Template-AdvancedDocument3 pagesProject Status Report Template-AdvancedSaikumar SelaNo ratings yet

- Certificate in Sale ManagementDocument35 pagesCertificate in Sale ManagementYoon WutyeeNo ratings yet

- Brand Portfolio ManagementDocument10 pagesBrand Portfolio ManagementMaria GutzNo ratings yet

- The Upcycling IndustryDocument24 pagesThe Upcycling IndustryAndrew Sell100% (1)

- Chapter-1 OPeration ManagementDocument2 pagesChapter-1 OPeration ManagementAyman Fergeion100% (1)

- Immrp Unit 5Document29 pagesImmrp Unit 5vikramvsuNo ratings yet

- Leadership Styles - Types of Leadership Styles - BBA - MantraDocument5 pagesLeadership Styles - Types of Leadership Styles - BBA - Mantrakarthik sarangNo ratings yet

- Chapter 5 Job Order Costing 2019 Problem 2 Golden Shower CompanyDocument4 pagesChapter 5 Job Order Costing 2019 Problem 2 Golden Shower CompanyCertified Public AccountantNo ratings yet

- PA L5 - SP1 - Assessment GuideDocument59 pagesPA L5 - SP1 - Assessment Guidelineo100% (1)

- Research-Informed Curriculum Design For A Master's-Level Program in Project ManagementDocument32 pagesResearch-Informed Curriculum Design For A Master's-Level Program in Project ManagementMariaNo ratings yet

- Outsourcing The I.T. FunctionDocument6 pagesOutsourcing The I.T. FunctionWilbert Carlo RachoNo ratings yet

- Traditional Marketing Metrics, Strategic Customer-Based Value Metrics, Customer PrivacyDocument10 pagesTraditional Marketing Metrics, Strategic Customer-Based Value Metrics, Customer PrivacyRedwanul IslamNo ratings yet

- Coso Erm 2017Document44 pagesCoso Erm 2017Daniel Garcia100% (4)

- PMBOK Cost (6th Edition) - 268-307-4Document3 pagesPMBOK Cost (6th Edition) - 268-307-4Nathan yemaneNo ratings yet

- Swot, Segmentation, Branding of ICI DuluxDocument7 pagesSwot, Segmentation, Branding of ICI Duluxgaurav0211987No ratings yet

- Ramneet Kaur HR Professional ResumeDocument2 pagesRamneet Kaur HR Professional ResumeSikander SinghNo ratings yet

- MGMT2106 Comparative Management Systems S12012Document17 pagesMGMT2106 Comparative Management Systems S12012Chaucer19No ratings yet

- Responsibilities Include:: Page 1 of 2 Saurabh BectorDocument2 pagesResponsibilities Include:: Page 1 of 2 Saurabh BectorsaurabhbectorNo ratings yet

- Inventory ControlDocument38 pagesInventory ControlKholoud AtefNo ratings yet

- Syllabus For Management of Education ChangeDocument9 pagesSyllabus For Management of Education ChangeTeachers Without BordersNo ratings yet

- Marketing Strategy For GreatWhite Electricals PVTDocument9 pagesMarketing Strategy For GreatWhite Electricals PVTankurgupta61No ratings yet

- Cima Edition 18 Vision, Values, Culture, Mission, Aims, Objectives, Strategy and TacticsDocument22 pagesCima Edition 18 Vision, Values, Culture, Mission, Aims, Objectives, Strategy and Tacticswaqar hattarNo ratings yet

- Batch - 1 EemDocument17 pagesBatch - 1 EemTummeti SujithNo ratings yet

- Issai 1315 PNDocument8 pagesIssai 1315 PNMohammad Jasim UddinNo ratings yet

- Introduction To ISO 14001 PDFDocument139 pagesIntroduction To ISO 14001 PDFAmerDaradkeh100% (1)

- Group 4 - Value Chain Analysis of WalmartDocument4 pagesGroup 4 - Value Chain Analysis of WalmartEsha ChaudharyNo ratings yet

- Non-Conformity Report: Commercial Aircraft GroupDocument2 pagesNon-Conformity Report: Commercial Aircraft GroupLalit Bom MallaNo ratings yet

- MDSL804D Lean Supply Chain Management PDFDocument302 pagesMDSL804D Lean Supply Chain Management PDFShashi KanwalNo ratings yet