You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- SSRN Id1025424Document27 pagesSSRN Id1025424Montasser KhelifiNo ratings yet

- FMR Special Report 2015-004 19-01-2015 GBDocument2 pagesFMR Special Report 2015-004 19-01-2015 GBMontasser KhelifiNo ratings yet

- LatAm investment opportunities in 2015: Mexico, Colombia, Chile, BrazilDocument4 pagesLatAm investment opportunities in 2015: Mexico, Colombia, Chile, BrazilMontasser KhelifiNo ratings yet

- FMR Special Report 2015-008 02-02-2015 GBDocument5 pagesFMR Special Report 2015-008 02-02-2015 GBMontasser KhelifiNo ratings yet

- FMR Special Report 2015-005 19-01-2015 GBDocument4 pagesFMR Special Report 2015-005 19-01-2015 GBMontasser KhelifiNo ratings yet

- MergerDocument15 pagesMergernkhljainNo ratings yet

- FMR Special Report 2015-007 22-01-2015 GBDocument5 pagesFMR Special Report 2015-007 22-01-2015 GBMontasser KhelifiNo ratings yet

- FMR Flash Economy 2015-061 30-01-2015 GBDocument7 pagesFMR Flash Economy 2015-061 30-01-2015 GBMontasser KhelifiNo ratings yet

- Using The Bloomberg Terminal For Data: Contents of PackageDocument41 pagesUsing The Bloomberg Terminal For Data: Contents of PackageMontasser KhelifiNo ratings yet

- JPM Credit DerivativesDocument180 pagesJPM Credit DerivativesJohn AvlakiotisNo ratings yet

- Corporate RatingsDocument7 pagesCorporate Ratingsgorgeoussans30No ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Jamuna BankDocument88 pagesJamuna BankMasood PervezNo ratings yet

- Cash Book: Cash Book Is A Book of Original Entry in WhichDocument10 pagesCash Book: Cash Book Is A Book of Original Entry in WhichCT SunilkumarNo ratings yet

- WetFeet I-Banking Overview PDFDocument3 pagesWetFeet I-Banking Overview PDFNaman AgarwalNo ratings yet

- LISTDocument4 pagesLISTNadimpalli ChaituNo ratings yet

- Mercedes BenzDocument16 pagesMercedes BenzRahul Bansal100% (1)

- Refrigerator CaseDocument3 pagesRefrigerator CaseTimothy Au-yongNo ratings yet

- Key terms in strategic planningDocument17 pagesKey terms in strategic planningDhez BolutanoNo ratings yet

- Sick CompanyDocument9 pagesSick CompanyPiyush PatelNo ratings yet

- ....Document60 pages....Ankit MaldeNo ratings yet

- 11a Reactions of Capital Markets To Financial ReportingDocument29 pages11a Reactions of Capital Markets To Financial ReportingRezha Setyo100% (3)

- Auditing Chapter 2 Professional StandardsDocument10 pagesAuditing Chapter 2 Professional StandardsBrianNo ratings yet

- Entrepreneurship Chapter 14 - Accessing ResourcesDocument4 pagesEntrepreneurship Chapter 14 - Accessing ResourcesSoledad Perez100% (1)

- Organization and Environmental Factors: S.Bharathi Mca, Mba., M.Phil, PGDPM&LLDocument25 pagesOrganization and Environmental Factors: S.Bharathi Mca, Mba., M.Phil, PGDPM&LLbharathimanian100% (1)

- Fundamental and Technical Analysis - Technical PaperDocument16 pagesFundamental and Technical Analysis - Technical PaperGauree AravkarNo ratings yet

- NO Company NameDocument26 pagesNO Company Namepravinpatil4643No ratings yet

- RMC No 37-2016Document6 pagesRMC No 37-2016sandra100% (1)

- Airline Industry One Fragile Industries Market Since TragiDocument4 pagesAirline Industry One Fragile Industries Market Since TragilsinožićNo ratings yet

- Motivation - Case StudyDocument4 pagesMotivation - Case Studysunnysopal100% (1)

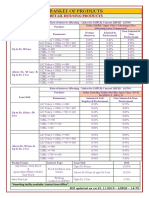

- BASKET OF RETAIL PRODUCTS RATESDocument3 pagesBASKET OF RETAIL PRODUCTS RATESVirendra K VermaNo ratings yet

- Invoice 82537Document1 pageInvoice 82537javwoxNo ratings yet

- RRB Exam Previous Year ModelDocument3 pagesRRB Exam Previous Year ModelShijumon XavierNo ratings yet

- New York State Urban Development Corporation D/b/a Empire State DevelopmentDocument166 pagesNew York State Urban Development Corporation D/b/a Empire State DevelopmentjspectorNo ratings yet

- ReviewerDocument27 pagesReviewerJedaiah CruzNo ratings yet

- F Annual Report 2011 ITDocument164 pagesF Annual Report 2011 ITwarun88No ratings yet

- Saudi Petrochemical Industry Report SummaryDocument8 pagesSaudi Petrochemical Industry Report SummaryHossam Mohamed KandilNo ratings yet

- Plastic Money in IndiaDocument71 pagesPlastic Money in IndiaDexter LoboNo ratings yet

- Go Ahead For F&O Report 16 December 2011-Mansukh Investment and Trading SolutionDocument6 pagesGo Ahead For F&O Report 16 December 2011-Mansukh Investment and Trading SolutionMansukh Investment & Trading SolutionsNo ratings yet

- 1000cc (GSXR1000 BZ111 2003-2004)Document71 pages1000cc (GSXR1000 BZ111 2003-2004)Radovan Katancevic100% (1)

- SA220Document22 pagesSA220Laura D'souza0% (1)

- The Changing Role of Managerial Accounting in A Global Business EnvironmentDocument14 pagesThe Changing Role of Managerial Accounting in A Global Business EnvironmentNastia Putri PertiwiNo ratings yet