You might also like

- Chap 020Document25 pagesChap 020mas azizNo ratings yet

- Bank Audit Process and TypesDocument33 pagesBank Audit Process and TypesVivek Tiwari50% (2)

- 2.1. What Is Auditing Standard?: General Standards Standards of Fieldwork Standards of ReportingDocument56 pages2.1. What Is Auditing Standard?: General Standards Standards of Fieldwork Standards of ReportingFackallofyouNo ratings yet

- Answers Chapter 1Document43 pagesAnswers Chapter 1Maricel Inoc FallerNo ratings yet

- Auditing The Finance and Accounting FunctionsDocument19 pagesAuditing The Finance and Accounting FunctionsMark Angelo BustosNo ratings yet

- AIS Chapter 3 Ethics 2Document7 pagesAIS Chapter 3 Ethics 2boa1315100% (1)

- Audit Two AaaDocument84 pagesAudit Two AaaYonasNo ratings yet

- New Client Audit Process and Materiality EvaluationDocument11 pagesNew Client Audit Process and Materiality EvaluationYee HooiNo ratings yet

- Capital BudgetingDocument4 pagesCapital Budgetingrachmmm0% (3)

- Asfaw, Audit II Chapter 5Document3 pagesAsfaw, Audit II Chapter 5alemayehu100% (1)

- Mount Kenya University Assignment 1 BSJ 4233: Forensic AccountingDocument2 pagesMount Kenya University Assignment 1 BSJ 4233: Forensic Accountinganastasia chegeNo ratings yet

- Auditing Revenue Cycle AuditsDocument42 pagesAuditing Revenue Cycle AuditsSweet Emme100% (1)

- Transaction Processing Systems LectureDocument40 pagesTransaction Processing Systems LectureShanmugapriyaVinodkumarNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and Errors: MFRS 108Document9 pagesAccounting Policies, Changes in Accounting Estimates and Errors: MFRS 108Nurul AsmidaNo ratings yet

- Study Notes Acct 311 Final Exam: Chapter 6 Payroll and Fixed Assets SystemsDocument3 pagesStudy Notes Acct 311 Final Exam: Chapter 6 Payroll and Fixed Assets SystemspsbacloudNo ratings yet

- AIS Report (Chapter 8)Document24 pagesAIS Report (Chapter 8)Cherlynn MagatNo ratings yet

- Audit Payroll Personnel Cycle Procedures Tests ControlsDocument22 pagesAudit Payroll Personnel Cycle Procedures Tests ControlsVironica ValentineNo ratings yet

- Tax Adminin L 3 CTODocument11 pagesTax Adminin L 3 CTOZIHERAMBERE AnastaseNo ratings yet

- Audit: Airline CompanyDocument4 pagesAudit: Airline CompanyArianna Maouna Serneo BernardoNo ratings yet

- Audit 1 Chapter 2Document37 pagesAudit 1 Chapter 2Meseret Asefa100% (1)

- CH 09 SMDocument25 pagesCH 09 SMNafisah MambuayNo ratings yet

- Audit Ch4Document42 pagesAudit Ch4Eyuel SintayehuNo ratings yet

- Responsibility Accounting1Document14 pagesResponsibility Accounting1Sujeet GuptaNo ratings yet

- Introduction to Internal AuditingDocument18 pagesIntroduction to Internal AuditingJhon Ray RabaraNo ratings yet

- Chapter - 04, Process of Assurance - Evidence and ReportingDocument5 pagesChapter - 04, Process of Assurance - Evidence and Reportingmahbub khanNo ratings yet

- Chapter 4Document5 pagesChapter 4Bonn GeorgeNo ratings yet

- Audit Report: - Communicating Key Audit Matters in The Independent Auditor's ReportDocument30 pagesAudit Report: - Communicating Key Audit Matters in The Independent Auditor's Reportyea okayNo ratings yet

- Income Tax Part 1Document16 pagesIncome Tax Part 1mary jhoyNo ratings yet

- True or FalseDocument1 pageTrue or FalseStela Marie CarandangNo ratings yet

- VIII. Consideration of Internal ControlDocument15 pagesVIII. Consideration of Internal ControlKrizza MaeNo ratings yet

- Chapter 6-Audit ReportDocument14 pagesChapter 6-Audit ReportDawit WorkuNo ratings yet

- Acctg 14 - Final ExamDocument7 pagesAcctg 14 - Final ExamMary Grace Castillo AlmonedaNo ratings yet

- Cash Count Working PaperDocument2 pagesCash Count Working PaperDebbieNo ratings yet

- Chapter 1: The Demand For Audit and Other Assurance ServicesDocument32 pagesChapter 1: The Demand For Audit and Other Assurance Servicessamuel debebeNo ratings yet

- Internal Auditing - PSA SummaryDocument42 pagesInternal Auditing - PSA Summaryjinkyjoyamorin100% (1)

- Presentation 2012Document257 pagesPresentation 2012lemonbandit100% (1)

- Auditing: Chapter 1: Introduction To AuditingDocument45 pagesAuditing: Chapter 1: Introduction To AuditingMIR AADILNo ratings yet

- Aas 28 The Auditor S Report On Financial StatementsDocument13 pagesAas 28 The Auditor S Report On Financial StatementsRishabh GuptaNo ratings yet

- Audit 2Document1 pageAudit 2MuhammadIjazAslamNo ratings yet

- Objectives and Risks for Payroll ManagementDocument2 pagesObjectives and Risks for Payroll ManagementEric Ashalley Tetteh100% (3)

- Approaches To Accounting Theory MidDocument11 pagesApproaches To Accounting Theory MidMd Mubashwir Chowdhury100% (1)

- Reviewer in LeasesDocument3 pagesReviewer in LeasesNicolaus CopernicusNo ratings yet

- Differences between Sampling and Non-Sampling RiskDocument1 pageDifferences between Sampling and Non-Sampling RiskBethelhemNo ratings yet

- Module 2Document8 pagesModule 2ysa tolosaNo ratings yet

- Issai 1330 PNDocument5 pagesIssai 1330 PNCharlie MaineNo ratings yet

- Psa 260Document10 pagesPsa 260shambiruarNo ratings yet

- Practical Auditing Notes - JeganrajDocument3 pagesPractical Auditing Notes - JeganrajjeganrajrajNo ratings yet

- Audit Responsibilities and ObjectivesDocument13 pagesAudit Responsibilities and ObjectivesDina Widiyanti67% (3)

- Internal Auditing Quiz 2Document3 pagesInternal Auditing Quiz 2richarddiagmelNo ratings yet

- Chapter 4 - Joint Arrangements-PROFE01Document6 pagesChapter 4 - Joint Arrangements-PROFE01Steffany RoqueNo ratings yet

- Chap-6-Verification of Assets and LiabilitiesDocument48 pagesChap-6-Verification of Assets and LiabilitiesAkash GuptaNo ratings yet

- Final Assessment S1, 2021Document5 pagesFinal Assessment S1, 2021Dilrukshi WanasingheNo ratings yet

- The Human Resources Management and Payroll CycleDocument17 pagesThe Human Resources Management and Payroll CycleHabtamu Hailemariam AsfawNo ratings yet

- The Basic Objectives of Corporate Governance AreDocument1 pageThe Basic Objectives of Corporate Governance AreRCA for Non-Academics Dianne0% (1)

- Auditing Chapter 1Document7 pagesAuditing Chapter 1Sigei LeonardNo ratings yet

- Internal Control System of The Philippine GovernmentDocument40 pagesInternal Control System of The Philippine GovernmentFRANZ MARTIN CALLANONo ratings yet

- Business PolicyDocument7 pagesBusiness PolicySuzette EstiponaNo ratings yet

- Assosai Guideline of Fraud and CorruptionDocument26 pagesAssosai Guideline of Fraud and CorruptionSandyCorpNo ratings yet

- The Role of SAI in Combating CorruptionDocument21 pagesThe Role of SAI in Combating CorruptionAdem SylejmaniNo ratings yet

- Combating Corruption in Asia and the PacificDocument8 pagesCombating Corruption in Asia and the PacificsanjayndutNo ratings yet

- Audit Reports Style GuideDocument27 pagesAudit Reports Style GuideSandyCorpNo ratings yet

- Assosai Guideline of Fraud and CorruptionDocument26 pagesAssosai Guideline of Fraud and CorruptionSandyCorpNo ratings yet

- Copenhagen Climate Change AgreementDocument13 pagesCopenhagen Climate Change AgreementSandyCorpNo ratings yet

- Title SheetDocument2 pagesTitle SheetSandyCorpNo ratings yet

- Atir Query 1 LadDocument3 pagesAtir Query 1 LadSandyCorpNo ratings yet

- Draft Inspection Report on Accounts of HeadmistressDocument6 pagesDraft Inspection Report on Accounts of HeadmistressSandyCorpNo ratings yet

- Draft Ir S&WC May 2014Document15 pagesDraft Ir S&WC May 2014SandyCorpNo ratings yet

- Review NoteDocument2 pagesReview NoteSandyCorpNo ratings yet

- Draft Ir MSSWB 2014Document16 pagesDraft Ir MSSWB 2014SandyCorpNo ratings yet

- Sl. No. Name & Designation Duties Allotted POS Issued (POS No.) Reference of para in DIR SignatureDocument3 pagesSl. No. Name & Designation Duties Allotted POS Issued (POS No.) Reference of para in DIR SignatureSandyCorpNo ratings yet

- POS Travelling Allowance of Rs 5Document3 pagesPOS Travelling Allowance of Rs 5SandyCorpNo ratings yet

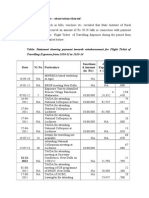

- Travelling Expenses From 2010-11 To 2013-14Document2 pagesTravelling Expenses From 2010-11 To 2013-14SandyCorpNo ratings yet

- CR PCDocument169 pagesCR PCSaurabh GaurNo ratings yet

- POS As Per General Financial RulesDocument1 pagePOS As Per General Financial RulesSandyCorpNo ratings yet

- Travelling Expenses From 2010-11 To 2013-14Document5 pagesTravelling Expenses From 2010-11 To 2013-14SandyCorpNo ratings yet

- Sriram G S ADDITIONAL TOPICS IN MOD HIST PDFDocument20 pagesSriram G S ADDITIONAL TOPICS IN MOD HIST PDFAnkur PandeyNo ratings yet

- Aizawl Municipal CouncilDocument5 pagesAizawl Municipal CouncilSandyCorpNo ratings yet

- Office of The Sinlung Hill Development CouncilDocument1 pageOffice of The Sinlung Hill Development CouncilSandyCorpNo ratings yet

- SR Sielent Fedures of Indian Society, Diversity of India Paper IiDocument22 pagesSR Sielent Fedures of Indian Society, Diversity of India Paper IipremathoammaNo ratings yet

- IR of NITDocument9 pagesIR of NITSandyCorpNo ratings yet

- Analytic Geometry Formulas PDFDocument4 pagesAnalytic Geometry Formulas PDFKaranbir RandhawaNo ratings yet

- Trigonometry Formulas PDFDocument2 pagesTrigonometry Formulas PDFsasi15augNo ratings yet

- Mod HistDocument3 pagesMod HistSandyCorpNo ratings yet

- People vs. Mariano, 71 SCRA 604: Months, or A Fine of More Than Two HundredDocument1 pagePeople vs. Mariano, 71 SCRA 604: Months, or A Fine of More Than Two HundredRussellNo ratings yet

- 2019 (GR No 229862, People of The Philippines V ZZZ) PDFDocument12 pages2019 (GR No 229862, People of The Philippines V ZZZ) PDFFrance SanchezNo ratings yet

- Fraud-Based Reconveyance Prescribes in 10 YearsDocument6 pagesFraud-Based Reconveyance Prescribes in 10 YearsElephantNo ratings yet

- 32 at MVD Charged in Fake Id Case (2004)Document4 pages32 at MVD Charged in Fake Id Case (2004)Roy WardenNo ratings yet

- Oblicon ReviewerDocument13 pagesOblicon ReviewerGeraldine Mae DamoslogNo ratings yet

- Strict Liability Offences - A Worrying Trend - Tax JournalDocument7 pagesStrict Liability Offences - A Worrying Trend - Tax JournalHenryNo ratings yet

- Complete Compliance KYC 2020Document25 pagesComplete Compliance KYC 2020amir bayatNo ratings yet

- Amidon IndictmentDocument2 pagesAmidon Indictmentldoranps100% (1)

- Commercial CasesDocument332 pagesCommercial CasesYam LicNo ratings yet

- Strong vs. Repide - Special Facts DoctrineDocument31 pagesStrong vs. Repide - Special Facts DoctrineMikee Clamor100% (1)

- Ljdddddddduddi Icjddddddddd: J (J (J (I.) L J I 1 L) Jljdi L L J (L J ( (DDocument1 pageLjdddddddduddi Icjddddddddd: J (J (J (I.) L J I 1 L) Jljdi L L J (L J ( (Ddusty kilgoreNo ratings yet

- Albano June29 EstateDonorsVAT AnswerKeyDocument5 pagesAlbano June29 EstateDonorsVAT AnswerKeySteven OrtizNo ratings yet

- Corporate Governance Practice at NHPC LTD, Jaypee Associates & United KingdomDocument20 pagesCorporate Governance Practice at NHPC LTD, Jaypee Associates & United KingdomsangramdeyNo ratings yet

- Ilagan Vs CADocument2 pagesIlagan Vs CAKacel CastroNo ratings yet

- CIR v. Ayala HotelsDocument20 pagesCIR v. Ayala HotelsnoonalawNo ratings yet

- Cyber Claims Analysis ReportDocument19 pagesCyber Claims Analysis ReportDaniela Guzman ArizaNo ratings yet

- Financial Crime Digest September 2021.Document105 pagesFinancial Crime Digest September 2021.Alexandra ElenaNo ratings yet

- Labor Ruling Affirms Conviction for Large Scale Illegal RecruitmentDocument2 pagesLabor Ruling Affirms Conviction for Large Scale Illegal RecruitmentEvielyn MateoNo ratings yet

- California Manufacturing Company Inc vs. Advanced System Technology IncDocument3 pagesCalifornia Manufacturing Company Inc vs. Advanced System Technology IncCarlota Nicolas VillaromanNo ratings yet

- BP Blg. 22 penalizes bouncing checksDocument64 pagesBP Blg. 22 penalizes bouncing checksMae NiagaraNo ratings yet

- CIR Vs The Estate of TodaDocument3 pagesCIR Vs The Estate of TodaLDNo ratings yet

- PEOPLE OF THE PHILIPPINES, Plaintiff-Appellee, v. ARMANDO RODAS1 and JOSE RODAS, SR., Accused-Appellants. G.R. NO. 175881: August 28, 2007Document13 pagesPEOPLE OF THE PHILIPPINES, Plaintiff-Appellee, v. ARMANDO RODAS1 and JOSE RODAS, SR., Accused-Appellants. G.R. NO. 175881: August 28, 2007Kaye Kiikai OnahonNo ratings yet

- T Chuma Research Project-McommDocument72 pagesT Chuma Research Project-McommIsaac ChinodaNo ratings yet

- Claw Ch3 Formation of A CompanyDocument20 pagesClaw Ch3 Formation of A CompanyNeha RohillaNo ratings yet

- Fraud Detection in Insurance Applications Using Predictive ModelingDocument16 pagesFraud Detection in Insurance Applications Using Predictive ModelingADEDEJI MICHEALNo ratings yet

- 73 People v. TemporadaDocument62 pages73 People v. TemporadaCarlota Nicolas VillaromanNo ratings yet

- United States v. Pasquale Panza, Seymour Ringle, Charles Fruscione, Gregory Cappello, Gregory Boutelle, Christopher Merlino, 750 F.2d 1141, 2d Cir. (1984)Document16 pagesUnited States v. Pasquale Panza, Seymour Ringle, Charles Fruscione, Gregory Cappello, Gregory Boutelle, Christopher Merlino, 750 F.2d 1141, 2d Cir. (1984)Scribd Government DocsNo ratings yet

- 04 Piercing DoctrineDocument37 pages04 Piercing DoctrinezahreenamolinaNo ratings yet

- CaliforniaDocument4 pagesCaliforniastanleyNo ratings yet

- Indian Institute of Banking & Finance: Certificate Examination in Prevention of Cyber Crimes and Fraud ManagementDocument6 pagesIndian Institute of Banking & Finance: Certificate Examination in Prevention of Cyber Crimes and Fraud ManagementAnkit Singh TomarNo ratings yet