You might also like

- NMG RykeGeerdHamerDocument23 pagesNMG RykeGeerdHamerljzapata100% (12)

- Resurse Online de MatematicaDocument3 pagesResurse Online de MatematicaFlaviub23No ratings yet

- William Walker Atkinson - Thought VibrationDocument161 pagesWilliam Walker Atkinson - Thought VibrationHomers SimpsonNo ratings yet

- As A Man Thinketh: by James AllenDocument22 pagesAs A Man Thinketh: by James AllenFlaviub23No ratings yet

- The Importance of Increased Emotional Intelligence (9 Pages)Document9 pagesThe Importance of Increased Emotional Intelligence (9 Pages)api-3696230100% (1)

- Discover the world's public domain books onlineDocument103 pagesDiscover the world's public domain books onlineNagarajanNo ratings yet

- Solar Plexus or Abdominal Brain by Theron Dumont PDFDocument75 pagesSolar Plexus or Abdominal Brain by Theron Dumont PDFzianna124765No ratings yet

- Eternal CareerDocument88 pagesEternal CareerFlaviub23No ratings yet

- Powerof WillDocument228 pagesPowerof WillNicholas GuribieNo ratings yet

- Mastery of SelfDocument72 pagesMastery of SelfeddymassaNo ratings yet

- Game of LifeDocument51 pagesGame of LifeFlaviub23No ratings yet

- Time ManagementDocument52 pagesTime ManagementKen LindenNo ratings yet

- A Special GiftDocument106 pagesA Special GiftFlaviub23No ratings yet

- Sae EbookDocument264 pagesSae EbookFlaviub23No ratings yet

- Knowing KnowledgeDocument176 pagesKnowing Knowledgestarmania831No ratings yet

- The Grieving Parents HandbookDocument26 pagesThe Grieving Parents HandbookFlaviub23100% (2)

- Binaural BeatsDocument32 pagesBinaural BeatsFlaviub23No ratings yet

- Road Signs 1Document11 pagesRoad Signs 1Flaviub23No ratings yet

- The LoveDocument305 pagesThe LoveFlaviub23No ratings yet

- A Life On FireDocument116 pagesA Life On Fireweb_queen100% (7)

- 3 Keys To FortuneDocument21 pages3 Keys To Fortunehuong512No ratings yet

- No Time For KarmaDocument166 pagesNo Time For KarmansziszoNo ratings yet

- WTGH SampleChapterDocument12 pagesWTGH SampleChapterFlaviub23No ratings yet

- Thegreatawakening Ebook PDFDocument89 pagesThegreatawakening Ebook PDFanny1990No ratings yet

- Wisdom of RamadahnDocument95 pagesWisdom of RamadahnFlaviub23No ratings yet

- Stepping Into Spiritual Oneness PDFDocument460 pagesStepping Into Spiritual Oneness PDFTaulant HoxhaNo ratings yet

- Truth About Astral Experience IDocument20 pagesTruth About Astral Experience IFlaviub230% (1)

- Sathya Sai BabaDocument15 pagesSathya Sai BabaFlaviub23No ratings yet

- Story of IWSDocument81 pagesStory of IWSFlaviub23No ratings yet

- Remembrance Karen WrightDocument52 pagesRemembrance Karen WrightFlaviub23No ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Journal Entries & Correction of ErrorsDocument33 pagesJournal Entries & Correction of ErrorsSteven RaintungNo ratings yet

- Summer Internship Project Karvy....Document61 pagesSummer Internship Project Karvy....Preet Josan100% (2)

- Banking sector challenges in Bangladesh: people, products, regulationsDocument2 pagesBanking sector challenges in Bangladesh: people, products, regulationsSajib DevNo ratings yet

- WWW TSPSC Gov inDocument22 pagesWWW TSPSC Gov inrameshNo ratings yet

- HDFC ChallanDocument1 pageHDFC ChallanJayant Modi100% (1)

- Response To First Comments On DCTV Show Last NightTwitter3.20.19Document39 pagesResponse To First Comments On DCTV Show Last NightTwitter3.20.19karen hudesNo ratings yet

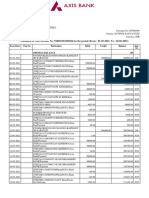

- Account STMTDocument3 pagesAccount STMTDhanush KumarNo ratings yet

- Payment, Clearing and Settlements Systems in The Euro AreaDocument78 pagesPayment, Clearing and Settlements Systems in The Euro AreaasalihovicNo ratings yet

- Banking Regulation Act Objectives and Salient FeaturesDocument35 pagesBanking Regulation Act Objectives and Salient FeaturesM A MUBEEN 172919831047No ratings yet

- 16 e Chapter 10Document29 pages16 e Chapter 10Yuki MiharuNo ratings yet

- Draft Format of Board ResolutionDocument2 pagesDraft Format of Board ResolutionzamasuaepNo ratings yet

- Organizational Study of The Perla Service Co-operative BankDocument37 pagesOrganizational Study of The Perla Service Co-operative BankFathima LibaNo ratings yet

- Sample Chapter5Document5 pagesSample Chapter5zoltan2014No ratings yet

- Current Account - Online Current Account Opening at HDFC Bank PDFDocument2 pagesCurrent Account - Online Current Account Opening at HDFC Bank PDFVishnu Shankar MishraNo ratings yet

- IMF Training Catalog 2013Document56 pagesIMF Training Catalog 2013Armand Dagbegnon TossouNo ratings yet

- BSP PresentationDocument27 pagesBSP PresentationMika AlimurongNo ratings yet

- 297Document1 page297Prem ChanderNo ratings yet

- Board Resolution Credit PolicyDocument2 pagesBoard Resolution Credit PolicyJayson Silot CabelloNo ratings yet

- Ibs Ipoh Main, Jsis 1 30/09/22Document3 pagesIbs Ipoh Main, Jsis 1 30/09/22JGL MOTORNo ratings yet

- Holder in Due Course DefinitionDocument3 pagesHolder in Due Course DefinitionTRISTARUSA100% (4)

- Postilion Diagram ElementsDocument12 pagesPostilion Diagram Elementsnzobya50% (2)

- HalifaxBOS 2001Document121 pagesHalifaxBOS 2001Mohamad RamdanNo ratings yet

- Mobile BankingDocument17 pagesMobile Bankingankitaneema87% (15)

- Case Digest Credit TransactionsDocument11 pagesCase Digest Credit TransactionsChristineNo ratings yet

- Substantive Tests of Transactions and Balances: Learning ObjectivesDocument61 pagesSubstantive Tests of Transactions and Balances: Learning ObjectivesMatarintis A Zulqarnain IINo ratings yet

- Pre Closing Trial BalanceDocument1 pagePre Closing Trial BalanceEli PerezNo ratings yet

- Educratsweb E-Magazine - Bimonthly E-Magazine - Issue No. 03 Jan2020Document170 pagesEducratsweb E-Magazine - Bimonthly E-Magazine - Issue No. 03 Jan2020GunjanNo ratings yet

- Hist Panel EURIBOR Jul 2010Document12 pagesHist Panel EURIBOR Jul 2010JaphyNo ratings yet

- Advanced Finance, Banking and Insurance SamenvattingDocument50 pagesAdvanced Finance, Banking and Insurance SamenvattingLisa TielemanNo ratings yet

- Recalled Questions - Promotion Test For Scale II To IIIDocument8 pagesRecalled Questions - Promotion Test For Scale II To IIIcandeva2007No ratings yet