You might also like

- Lecture Notes2231 SCMDocument57 pagesLecture Notes2231 SCMhappynandaNo ratings yet

- Chapter 3.1 Mechanics of Futures MarketsDocument17 pagesChapter 3.1 Mechanics of Futures MarketslelouchNo ratings yet

- Building Your Financial Future: A Practical Guide For Young AdultsFrom EverandBuilding Your Financial Future: A Practical Guide For Young AdultsNo ratings yet

- Chapter 4 - Simple InterestDocument18 pagesChapter 4 - Simple InterestKPRobin0% (1)

- Bond and Stock ValuationDocument44 pagesBond and Stock Valuationali khanNo ratings yet

- FM Textbook Solutions Chapter 8 Second EditionDocument11 pagesFM Textbook Solutions Chapter 8 Second EditionlibredescargaNo ratings yet

- Gitmanjoeh 238702 Im08Document23 pagesGitmanjoeh 238702 Im08trevorsum123No ratings yet

- Forecasting of Financial StatementsDocument9 pagesForecasting of Financial StatementssamaanNo ratings yet

- Practice For Chapter 5 SolutionsDocument6 pagesPractice For Chapter 5 SolutionsAndrew WhitfieldNo ratings yet

- Eiteman PPT CH01Document37 pagesEiteman PPT CH01Divya BansalNo ratings yet

- CHAPTER 9 The Cost of CapitalDocument37 pagesCHAPTER 9 The Cost of CapitalAhsanNo ratings yet

- Chapter 06Document47 pagesChapter 06Amylia AmirNo ratings yet

- SMJC 3123 Project Finance QuestionsDocument2 pagesSMJC 3123 Project Finance QuestionsJuandeLaNo ratings yet

- A Case Study On Business Mathematics - Assignment PointDocument2 pagesA Case Study On Business Mathematics - Assignment PointJunior PyareNo ratings yet

- Past Exam Questions - InvestmentDocument14 pagesPast Exam Questions - InvestmentTalia simonNo ratings yet

- This Question Has Been Answered: Find Study ResourcesDocument3 pagesThis Question Has Been Answered: Find Study ResourcesChau NguyenNo ratings yet

- Challenges in Forecasting Exchange Rates by Multinational Corporations Ms 12may2016Document22 pagesChallenges in Forecasting Exchange Rates by Multinational Corporations Ms 12may2016dr Milorad Stamenovic100% (3)

- Chapter 3.2 Futures HedgingDocument19 pagesChapter 3.2 Futures HedginglelouchNo ratings yet

- Madura FMI9e IM Ch14Document15 pagesMadura FMI9e IM Ch14Stanley HoNo ratings yet

- Derivatives Individual AssignmentDocument24 pagesDerivatives Individual AssignmentCarine TeeNo ratings yet

- International & Transnational StrategiesDocument28 pagesInternational & Transnational Strategieskirthika sekar100% (5)

- Pricing Decisions - MCQsDocument26 pagesPricing Decisions - MCQsMaxwell;No ratings yet

- FX Risk Management Transaction Exposure: Slide 1Document55 pagesFX Risk Management Transaction Exposure: Slide 1prakashputtuNo ratings yet

- KLCI Futures Contracts AnalysisDocument63 pagesKLCI Futures Contracts AnalysisSidharth ChoudharyNo ratings yet

- Time Value of MoneyDocument2 pagesTime Value of Moneyanon_672065362No ratings yet

- Venture Capital FinalDocument26 pagesVenture Capital Finalaarzoo dadwalNo ratings yet

- CH 11 HW SolutionsDocument9 pagesCH 11 HW SolutionsAriefka Sari DewiNo ratings yet

- Tutorial 2 AnswersDocument6 pagesTutorial 2 AnswersBee LNo ratings yet

- Business Ethics and MNCDocument21 pagesBusiness Ethics and MNCsanchitshah777100% (1)

- The International Financial Environment: Multinational Corporation (MNC)Document30 pagesThe International Financial Environment: Multinational Corporation (MNC)FarhanAwaisiNo ratings yet

- FOREX EXERCISE QUESTIONSDocument4 pagesFOREX EXERCISE QUESTIONShoholalahoopNo ratings yet

- KLIBOR Futures Trading StrategiesDocument4 pagesKLIBOR Futures Trading Strategieskristin_kim_13No ratings yet

- Comparative Study Between Ulip & ElssDocument67 pagesComparative Study Between Ulip & ElssN.MUTHUKUMARAN100% (2)

- Introduction To DerivativesDocument7 pagesIntroduction To DerivativesRashwanth TcNo ratings yet

- Working Capital Practice SetDocument12 pagesWorking Capital Practice SetRyan Malanum AbrioNo ratings yet

- EBT Market: Bonds-Types and CharacteristicsDocument25 pagesEBT Market: Bonds-Types and CharacteristicsKristen HicksNo ratings yet

- Cfi1203 Module 2 Interest Rates Determination & StructureDocument8 pagesCfi1203 Module 2 Interest Rates Determination & StructureLeonorahNo ratings yet

- 324 - Foreign Exchange Market-ForEXDocument74 pages324 - Foreign Exchange Market-ForEXTamuna BibiluriNo ratings yet

- Foundations of Finance: An Introduction To The Foundations of Financial Management - The Ties That BindDocument35 pagesFoundations of Finance: An Introduction To The Foundations of Financial Management - The Ties That BindManish MahajanNo ratings yet

- Arithmetic NTH Term (Autosaved)Document28 pagesArithmetic NTH Term (Autosaved)LastCardHolderNo ratings yet

- HUM 2107: Engineering Economics: Fiscal and Monetary PolicyDocument10 pagesHUM 2107: Engineering Economics: Fiscal and Monetary PolicyAshrafi ChistyNo ratings yet

- Chapter 1 DERIVATIVES INTRODUCTION AND OVERVIEWDocument27 pagesChapter 1 DERIVATIVES INTRODUCTION AND OVERVIEWfatenyousmeraNo ratings yet

- Financial Market and Portfolio Management Assignment 2Document6 pagesFinancial Market and Portfolio Management Assignment 2leeroy mekiNo ratings yet

- 1.2 Doc-20180120-Wa0002Document23 pages1.2 Doc-20180120-Wa0002Prachet KulkarniNo ratings yet

- Key Financial System RolesDocument2 pagesKey Financial System RolesLinusChinNo ratings yet

- Topic 4 Central Bank (BNM)Document56 pagesTopic 4 Central Bank (BNM)Ing HongNo ratings yet

- Question Bank SAPMDocument7 pagesQuestion Bank SAPMN Rakesh92% (12)

- Chapter 1Document213 pagesChapter 1Annur SofeaNo ratings yet

- Answer:: ch07: Dealing With Foreign ExchangeDocument10 pagesAnswer:: ch07: Dealing With Foreign ExchangeTong Yuen ShunNo ratings yet

- Calculating Cost of Capital and WACCDocument21 pagesCalculating Cost of Capital and WACCMardi UmarNo ratings yet

- CHAPTER 3 Investment Information and Security TransactionDocument22 pagesCHAPTER 3 Investment Information and Security TransactionTika TimilsinaNo ratings yet

- CH 2 Nature and Purpose of DerivativesDocument0 pagesCH 2 Nature and Purpose of DerivativesumairmbaNo ratings yet

- Financial MarketDocument10 pagesFinancial MarketLinganagouda PatilNo ratings yet

- 426 Chap Suggested AnswersDocument16 pages426 Chap Suggested AnswersMohommed AyazNo ratings yet

- Analyzing Common Stocks: OutlineDocument30 pagesAnalyzing Common Stocks: OutlineHazel Anne MarianoNo ratings yet

- Lecture 5 PDFDocument90 pagesLecture 5 PDFsyingNo ratings yet

- PGDFMDocument6 pagesPGDFMAvinashNo ratings yet

- Investment Banking Immersion Program SyllabusDocument4 pagesInvestment Banking Immersion Program SyllabussNo ratings yet

- Cloud Summer Presentation Eng v3.1Document20 pagesCloud Summer Presentation Eng v3.1Dino TTNo ratings yet

- Cloud Summer Marketing Plan Eng 3.1Document6 pagesCloud Summer Marketing Plan Eng 3.1Dino TTNo ratings yet

- 8.2o Why Would I Want To Move My Coins Away From An ExchangeDocument1 page8.2o Why Would I Want To Move My Coins Away From An Exchangetrevorsum123No ratings yet

- 8.2f Don't Travel With Your Crypto WalletDocument1 page8.2f Don't Travel With Your Crypto Wallettrevorsum123No ratings yet

- 8.2a Secure USB To Export Your ETHDocument2 pages8.2a Secure USB To Export Your ETHtrevorsum123No ratings yet

- 8.2n What Coins Do The Hard Wallets SupportDocument2 pages8.2n What Coins Do The Hard Wallets Supporttrevorsum123No ratings yet

- Hi, Upgrade Your Account Liftetime - HTTPS://WWW - Wsodownloads.in/ Lifetime Membership Cost Only $25 USD Exclusive VIP Download AreaDocument1 pageHi, Upgrade Your Account Liftetime - HTTPS://WWW - Wsodownloads.in/ Lifetime Membership Cost Only $25 USD Exclusive VIP Download Areatrevorsum123No ratings yet

- Cloud Family PAMM IB PlanDocument4 pagesCloud Family PAMM IB Plantrevorsum123No ratings yet

- AlphaX IntroductionDocument10 pagesAlphaX IntroductionDino TTNo ratings yet

- 8.2h Dilute RiskDocument1 page8.2h Dilute Risktrevorsum123No ratings yet

- 8.2i Another Security ToolDocument1 page8.2i Another Security Tooltrevorsum123No ratings yet

- Must ReadDocument1 pageMust Readtrevorsum123No ratings yet

- 8.2j Where To Get A Bitcoin WalletDocument1 page8.2j Where To Get A Bitcoin Wallettrevorsum123No ratings yet

- 8.2d Update - Ignore ThisDocument1 page8.2d Update - Ignore Thistrevorsum123No ratings yet

- 1.10a 2020 UPDATEDocument1 page1.10a 2020 UPDATEtrevorsum123No ratings yet

- 1.i0b Passive Income - Up To 12% Returns! Better Than Real Estate As No Nightmare TennantsDocument1 page1.i0b Passive Income - Up To 12% Returns! Better Than Real Estate As No Nightmare Tennantstrevorsum123No ratings yet

- Hi, Upgrade Your Account Liftetime - HTTPS://WWW - Wsodownloads.in/ Lifetime Membership Cost Only $25 USD Exclusive VIP Download AreaDocument1 pageHi, Upgrade Your Account Liftetime - HTTPS://WWW - Wsodownloads.in/ Lifetime Membership Cost Only $25 USD Exclusive VIP Download Areatrevorsum123No ratings yet

- 8.2g Where Can I Find Other WalletsDocument1 page8.2g Where Can I Find Other Walletstrevorsum123No ratings yet

- Must ReadDocument1 pageMust Readtrevorsum123No ratings yet

- 1.05 Got QuestionsDocument1 page1.05 Got Questionstrevorsum123No ratings yet

- Must ReadDocument1 pageMust Readtrevorsum123No ratings yet

- Hi, Upgrade Your Account Liftetime - HTTPS://WWW - Wsodownloads.in/ Lifetime Membership Cost Only $25 USD Exclusive VIP Download AreaDocument1 pageHi, Upgrade Your Account Liftetime - HTTPS://WWW - Wsodownloads.in/ Lifetime Membership Cost Only $25 USD Exclusive VIP Download Areatrevorsum123No ratings yet

- Academic Essay WritingDocument26 pagesAcademic Essay WritingFahad Areeb100% (1)

- 1.03 Welcome To The $100 A Day Investment CourseDocument1 page1.03 Welcome To The $100 A Day Investment Coursetrevorsum123No ratings yet

- The Art of Tehnical AnalisisDocument87 pagesThe Art of Tehnical AnalisisBursa ValutaraNo ratings yet

- Getting Started With Excel: ComprehensiveDocument10 pagesGetting Started With Excel: Comprehensivetrevorsum123No ratings yet

- 1.04 Why Investing in Cryptocurrencies Could Make You A MillionaireDocument1 page1.04 Why Investing in Cryptocurrencies Could Make You A Millionairetrevorsum123No ratings yet

- Excel Training - Level 1Document95 pagesExcel Training - Level 1Cristiano Aparecido da SilvaNo ratings yet

- Policy and Procedures For Regular Procurement Rev - 4 April 2015 - 0 PDFDocument186 pagesPolicy and Procedures For Regular Procurement Rev - 4 April 2015 - 0 PDFtrevorsum123No ratings yet

- 1 Ahmad 2 Ahmad 3 Ahmad 4 Ahmad 5 Ahmad: 8) Fill HandleDocument35 pages1 Ahmad 2 Ahmad 3 Ahmad 4 Ahmad 5 Ahmad: 8) Fill Handletrevorsum123No ratings yet

- Group No-15 - Section-B - Fin1104Document6 pagesGroup No-15 - Section-B - Fin1104Aswath ChandrasekarNo ratings yet

- W 28320Document40 pagesW 28320pralesh gamareNo ratings yet

- 5Year1MillionTradingPlan10 2Document12 pages5Year1MillionTradingPlan10 2Anonymous JE7uJRNo ratings yet

- Keene, Andrew - Ichimoku Cloud, World's Best Technical IndicatorDocument17 pagesKeene, Andrew - Ichimoku Cloud, World's Best Technical IndicatorihaiNo ratings yet

- WRB Analysis Tutorials 011914 v2.5Document65 pagesWRB Analysis Tutorials 011914 v2.5danielNo ratings yet

- Solutions Manual: Introducing Corporate Finance 2eDocument10 pagesSolutions Manual: Introducing Corporate Finance 2ePaul Sau HutaNo ratings yet

- MSCI Vietnam Index (USD)Document3 pagesMSCI Vietnam Index (USD)AlezNgNo ratings yet

- Fim SummaryDocument92 pagesFim Summaryemre kutayNo ratings yet

- Notes - On - The - Thoughtful - Investor Basant - MaheshwariDocument17 pagesNotes - On - The - Thoughtful - Investor Basant - Maheshwarishylesh86100% (2)

- Financial and Technical AnalysisDocument62 pagesFinancial and Technical AnalysisBhupender Singh RawatNo ratings yet

- FM09-CH 03Document14 pagesFM09-CH 03vtiwari2No ratings yet

- David Rosenberg SummaryDocument4 pagesDavid Rosenberg Summaryrichardck61No ratings yet

- CMPT 16103Document289 pagesCMPT 16103Pratheesh KurupNo ratings yet

- 09 Comm 308 Final Exam (Summer 1 2011) SolutionsDocument18 pages09 Comm 308 Final Exam (Summer 1 2011) SolutionsAfafe ElNo ratings yet

- En Gbpjpy 20190520 M PDFDocument2 pagesEn Gbpjpy 20190520 M PDFradiNo ratings yet

- Unit 4 Valuation of Bonds and SharesDocument33 pagesUnit 4 Valuation of Bonds and SharesvinayakbankarNo ratings yet

- Presented By:-Manisha Choubey Akshit Kohli Abhishek MishraDocument19 pagesPresented By:-Manisha Choubey Akshit Kohli Abhishek Mishra9755670992No ratings yet

- Insights on wealth from The Psychology of MoneyDocument1 pageInsights on wealth from The Psychology of MoneyTanri ArrizasyifaaNo ratings yet

- Business Model CanvasDocument2 pagesBusiness Model CanvasApanama StudioNo ratings yet

- ISEF - 2019 - ISDA IIFM Hedging Standards Ijlal A Alvi IIFMDocument20 pagesISEF - 2019 - ISDA IIFM Hedging Standards Ijlal A Alvi IIFMyunniyustisiaNo ratings yet

- FEA Rules Part 1 ResidentsDocument5 pagesFEA Rules Part 1 Residentssailung88No ratings yet

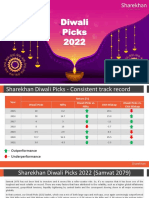

- DiwaliPicks2022 131022Document22 pagesDiwaliPicks2022 131022tranganathanNo ratings yet

- Here's - How - To - Use - Thread - by - Dangstrat - Mar 22, 23 - From - RattibhaDocument16 pagesHere's - How - To - Use - Thread - by - Dangstrat - Mar 22, 23 - From - RattibhaidkwhatiswrongbetaNo ratings yet

- Interview With Michael Hokensen, Asset ManagerDocument5 pagesInterview With Michael Hokensen, Asset ManagerWorldwide finance newsNo ratings yet

- International Finance - Part II International Financial Markets & InstrumentsDocument282 pagesInternational Finance - Part II International Financial Markets & InstrumentsMohit SharmaNo ratings yet

- Ch8 Questions 226Document3 pagesCh8 Questions 226Kye HarveyNo ratings yet

- Mean Reversion Trading Strategies PDFDocument7 pagesMean Reversion Trading Strategies PDFเสกสรรค์ จันทร์สุขปลูกNo ratings yet

- Chapter 1 IntroductionDocument31 pagesChapter 1 IntroductionAnil SharmaNo ratings yet

- Regulatory Framework of Corporate Governance in IndiaDocument10 pagesRegulatory Framework of Corporate Governance in IndiaSavita NeetuNo ratings yet

- Nine Black Robes: Inside the Supreme Court's Drive to the Right and Its Historic ConsequencesFrom EverandNine Black Robes: Inside the Supreme Court's Drive to the Right and Its Historic ConsequencesNo ratings yet

- The Smear: How Shady Political Operatives and Fake News Control What You See, What You Think, and How You VoteFrom EverandThe Smear: How Shady Political Operatives and Fake News Control What You See, What You Think, and How You VoteRating: 4.5 out of 5 stars4.5/5 (16)

- We've Got Issues: How You Can Stand Strong for America's Soul and SanityFrom EverandWe've Got Issues: How You Can Stand Strong for America's Soul and SanityNo ratings yet

- Witch Hunt: The Story of the Greatest Mass Delusion in American Political HistoryFrom EverandWitch Hunt: The Story of the Greatest Mass Delusion in American Political HistoryRating: 4 out of 5 stars4/5 (6)

- Thomas Jefferson: Author of AmericaFrom EverandThomas Jefferson: Author of AmericaRating: 4 out of 5 stars4/5 (107)

- Blood Money: Why the Powerful Turn a Blind Eye While China Kills AmericansFrom EverandBlood Money: Why the Powerful Turn a Blind Eye While China Kills AmericansRating: 4.5 out of 5 stars4.5/5 (10)

- Modern Warriors: Real Stories from Real HeroesFrom EverandModern Warriors: Real Stories from Real HeroesRating: 3.5 out of 5 stars3.5/5 (3)

- The Russia Hoax: The Illicit Scheme to Clear Hillary Clinton and Frame Donald TrumpFrom EverandThe Russia Hoax: The Illicit Scheme to Clear Hillary Clinton and Frame Donald TrumpRating: 4.5 out of 5 stars4.5/5 (11)

- Reading the Constitution: Why I Chose Pragmatism, not TextualismFrom EverandReading the Constitution: Why I Chose Pragmatism, not TextualismNo ratings yet

- Game Change: Obama and the Clintons, McCain and Palin, and the Race of a LifetimeFrom EverandGame Change: Obama and the Clintons, McCain and Palin, and the Race of a LifetimeRating: 4 out of 5 stars4/5 (572)

- The Courage to Be Free: Florida's Blueprint for America's RevivalFrom EverandThe Courage to Be Free: Florida's Blueprint for America's RevivalNo ratings yet

- The Red and the Blue: The 1990s and the Birth of Political TribalismFrom EverandThe Red and the Blue: The 1990s and the Birth of Political TribalismRating: 4 out of 5 stars4/5 (29)

- Stonewalled: My Fight for Truth Against the Forces of Obstruction, Intimidation, and Harassment in Obama's WashingtonFrom EverandStonewalled: My Fight for Truth Against the Forces of Obstruction, Intimidation, and Harassment in Obama's WashingtonRating: 4.5 out of 5 stars4.5/5 (21)

- The Quiet Man: The Indispensable Presidency of George H.W. BushFrom EverandThe Quiet Man: The Indispensable Presidency of George H.W. BushRating: 4 out of 5 stars4/5 (1)

- The Great Gasbag: An A–Z Study Guide to Surviving Trump WorldFrom EverandThe Great Gasbag: An A–Z Study Guide to Surviving Trump WorldRating: 3.5 out of 5 stars3.5/5 (9)

- Hatemonger: Stephen Miller, Donald Trump, and the White Nationalist AgendaFrom EverandHatemonger: Stephen Miller, Donald Trump, and the White Nationalist AgendaRating: 4 out of 5 stars4/5 (5)

- Commander In Chief: FDR's Battle with Churchill, 1943From EverandCommander In Chief: FDR's Battle with Churchill, 1943Rating: 4 out of 5 stars4/5 (16)

- An Ordinary Man: The Surprising Life and Historic Presidency of Gerald R. FordFrom EverandAn Ordinary Man: The Surprising Life and Historic Presidency of Gerald R. FordRating: 4 out of 5 stars4/5 (5)

- Trumpocracy: The Corruption of the American RepublicFrom EverandTrumpocracy: The Corruption of the American RepublicRating: 4 out of 5 stars4/5 (68)

- Power Grab: The Liberal Scheme to Undermine Trump, the GOP, and Our RepublicFrom EverandPower Grab: The Liberal Scheme to Undermine Trump, the GOP, and Our RepublicNo ratings yet

- The Magnificent Medills: The McCormick-Patterson Dynasty: America's Royal Family of Journalism During a Century of Turbulent SplendorFrom EverandThe Magnificent Medills: The McCormick-Patterson Dynasty: America's Royal Family of Journalism During a Century of Turbulent SplendorNo ratings yet

- The Deep State: How an Army of Bureaucrats Protected Barack Obama and Is Working to Destroy the Trump AgendaFrom EverandThe Deep State: How an Army of Bureaucrats Protected Barack Obama and Is Working to Destroy the Trump AgendaRating: 4.5 out of 5 stars4.5/5 (4)

- Confidence Men: Wall Street, Washington, and the Education of a PresidentFrom EverandConfidence Men: Wall Street, Washington, and the Education of a PresidentRating: 3.5 out of 5 stars3.5/5 (52)

- The Last Republicans: Inside the Extraordinary Relationship Between George H.W. Bush and George W. BushFrom EverandThe Last Republicans: Inside the Extraordinary Relationship Between George H.W. Bush and George W. BushRating: 4 out of 5 stars4/5 (6)

- Camelot's Court: Inside the Kennedy White HouseFrom EverandCamelot's Court: Inside the Kennedy White HouseRating: 4 out of 5 stars4/5 (17)

- Profiles in Ignorance: How America's Politicians Got Dumb and DumberFrom EverandProfiles in Ignorance: How America's Politicians Got Dumb and DumberRating: 4.5 out of 5 stars4.5/5 (80)