You might also like

- Investment Outlays: Long-Term AssetsDocument12 pagesInvestment Outlays: Long-Term AssetsRimpy SondhNo ratings yet

- Asset Integrity ManagementDocument12 pagesAsset Integrity Managementdaniel leon marinNo ratings yet

- Research Proposal PDFDocument21 pagesResearch Proposal PDFRamraj Ronil SharmaNo ratings yet

- The Effect of Blade Lean on Axial Turbine Stator FlowDocument17 pagesThe Effect of Blade Lean on Axial Turbine Stator FlowAmbrish SinghNo ratings yet

- Ch11 13ed CF Estimation MinicMasterDocument20 pagesCh11 13ed CF Estimation MinicMasterAnoop SlathiaNo ratings yet

- MBA Dissertation TitleDocument5 pagesMBA Dissertation Titleyadgar_870% (1)

- PS AIM Extended BrochureDocument8 pagesPS AIM Extended BrochureSabino LaraNo ratings yet

- Intial Information Report (Financial Analysis)Document13 pagesIntial Information Report (Financial Analysis)NiveditaSnehiNo ratings yet

- Revised CH 5 Material Handling PDFDocument19 pagesRevised CH 5 Material Handling PDFTaha Bzizi100% (1)

- Faculty of Management Tribhuvan University: BBS (4 Year) Project Report WritingDocument54 pagesFaculty of Management Tribhuvan University: BBS (4 Year) Project Report WritingPranesh KatuwalNo ratings yet

- Effect of Inlet Guide Vanes and Sharp Blades On The Performance of A Turbomolecular PumpDocument6 pagesEffect of Inlet Guide Vanes and Sharp Blades On The Performance of A Turbomolecular PumpSuresh ShreeNo ratings yet

- Risk Analysis in Capital BudgetingDocument18 pagesRisk Analysis in Capital BudgetingKushagra RaghavNo ratings yet

- Cash Flow Project Tushar - PDF 0Document42 pagesCash Flow Project Tushar - PDF 0Tushar UpadeNo ratings yet

- Financial Statement Analysis of Everest EmporiumDocument8 pagesFinancial Statement Analysis of Everest EmporiumArthur Richard SumaldeNo ratings yet

- Impact of marginal costing and leverages on cement industriesDocument10 pagesImpact of marginal costing and leverages on cement industriesrakeshkchouhanNo ratings yet

- Portfolio Management Banking SectorDocument133 pagesPortfolio Management Banking SectorNitinAgnihotri100% (1)

- Capital Bud ..Updated FinalDocument36 pagesCapital Bud ..Updated FinalKeyur JoshiNo ratings yet

- MET's Institute Final Project Report on Exploring Tyre Market Potential in Raigad DistrictDocument32 pagesMET's Institute Final Project Report on Exploring Tyre Market Potential in Raigad DistrictgoswamiphotostatNo ratings yet

- COMPARATIVE STUDY On Working Capital Management Between Bhilai Steel Plant & Tisco GroupDocument78 pagesCOMPARATIVE STUDY On Working Capital Management Between Bhilai Steel Plant & Tisco GroupMustafa S TajaniNo ratings yet

- Identification of Potential Investment Opportunities - The CapitalDocument4 pagesIdentification of Potential Investment Opportunities - The CapitalAshley_RulzzzzzzzNo ratings yet

- Notes On Capital BudgetingDocument3 pagesNotes On Capital BudgetingCheshta Suri100% (1)

- Project On Capital Budgeting PPT DataDocument3 pagesProject On Capital Budgeting PPT DataMadhuri GuptaNo ratings yet

- The Marketing Concept - What It Is and What It Is Not - RevisedDocument7 pagesThe Marketing Concept - What It Is and What It Is Not - Revisedmarco_chin846871No ratings yet

- Gls University Faculty of Commerce Sub: Advanced Corporate Account - 2 Objective Questions (17-18) Unit:-Accounts of Banking CompaniesDocument11 pagesGls University Faculty of Commerce Sub: Advanced Corporate Account - 2 Objective Questions (17-18) Unit:-Accounts of Banking Companiessumathi psgcas0% (1)

- Hasdrubal Asset Integrity OverviewDocument20 pagesHasdrubal Asset Integrity OverviewAjmi HmidaNo ratings yet

- Calculating IRR Through Fake Payback Period MethodDocument9 pagesCalculating IRR Through Fake Payback Period Methodakshit_vij0% (1)

- Capital Budgeting Techniques PDFDocument57 pagesCapital Budgeting Techniques PDFraj100% (1)

- Cost of CapitalDocument55 pagesCost of CapitalSaritasaruNo ratings yet

- BEHAVIOURAL FINANCE PPT PDFDocument27 pagesBEHAVIOURAL FINANCE PPT PDFLibin GeevargheseNo ratings yet

- Mba 201Document2 pagesMba 201Nitish Kumar100% (2)

- BlackbookDocument3 pagesBlackbookrajat dayamNo ratings yet

- Sustainable Energy Handbook ModuleDocument14 pagesSustainable Energy Handbook ModuleforuzzNo ratings yet

- ENGRO FERTILIZERS - Aiman JamilDocument25 pagesENGRO FERTILIZERS - Aiman JamilRosenna99No ratings yet

- Financial Management Overview and Key ConceptsDocument16 pagesFinancial Management Overview and Key ConceptsKAUSHIKNo ratings yet

- Airline Financial Analysis Project - ACC40810 - 17200991Document23 pagesAirline Financial Analysis Project - ACC40810 - 17200991dnhn1992No ratings yet

- Synopsis Working CapitalDocument27 pagesSynopsis Working CapitalManish DwivediNo ratings yet

- Continuous ProbDocument10 pagesContinuous Probtushar jainNo ratings yet

- Risk CalculationDocument33 pagesRisk CalculationAbhishek RaiNo ratings yet

- Banks' Behavior Study Finds Profit DriversDocument16 pagesBanks' Behavior Study Finds Profit DriversAbdelghani RemramNo ratings yet

- Aim PDFDocument6 pagesAim PDFSlim Ben SlimaneNo ratings yet

- P4 Chapter 04 Risk Adjusted WACC and Adjusted Present Value PDFDocument45 pagesP4 Chapter 04 Risk Adjusted WACC and Adjusted Present Value PDFasim tariqNo ratings yet

- New Invt MGT KesoramDocument69 pagesNew Invt MGT Kesoramtulasinad123No ratings yet

- PPM 542 - Shimelis Tessema - GSR-2453-13Document4 pagesPPM 542 - Shimelis Tessema - GSR-2453-13Shimelis TesemaNo ratings yet

- Security Analysis & Portfolio Management Lec 1Document55 pagesSecurity Analysis & Portfolio Management Lec 1Anonymous utSFl8No ratings yet

- ConclusionDocument3 pagesConclusionAsadvirkNo ratings yet

- BIT Pilani Financial Management Comprehensive Exam QuestionsDocument2 pagesBIT Pilani Financial Management Comprehensive Exam QuestionsMohana KrishnaNo ratings yet

- Lesson 5 Tax Planning With Reference To Capital StructureDocument37 pagesLesson 5 Tax Planning With Reference To Capital StructurekelvinNo ratings yet

- Training On RCM at Jakarta by Marcus EvansDocument4 pagesTraining On RCM at Jakarta by Marcus EvansJigarDhabaliaNo ratings yet

- Financial Management MCQs on Capital Budgeting, Risk AnalysisDocument17 pagesFinancial Management MCQs on Capital Budgeting, Risk Analysis19101977No ratings yet

- Allowable and Disallowable Expenses PDFDocument1 pageAllowable and Disallowable Expenses PDFAnna MwitaNo ratings yet

- CCA Current Cost Accounting Theory 2021Document4 pagesCCA Current Cost Accounting Theory 2021PradeepNo ratings yet

- Risk ManagementDocument35 pagesRisk Managementfafese7300No ratings yet

- Spreadsheet Analysis of Demand and Supply for Sunbest Orange JuiceDocument2 pagesSpreadsheet Analysis of Demand and Supply for Sunbest Orange JuicekarobikushalNo ratings yet

- Mba ProjectDocument71 pagesMba ProjectSahana SindyaNo ratings yet

- Study of Expenses in Different Branches of Hindustan Times at Western UP RegionDocument73 pagesStudy of Expenses in Different Branches of Hindustan Times at Western UP RegionGuman Singh0% (1)

- 2 4 Term Credit EvaluationDocument23 pages2 4 Term Credit EvaluationRagini VermaNo ratings yet

- Capital Budgeting TutorialDocument26 pagesCapital Budgeting Tutorialf20221182No ratings yet

- Unit-2 Investment AppraisalDocument47 pagesUnit-2 Investment AppraisalPrà ShâñtNo ratings yet

- Incremental Analysis for Engineering Project DecisionsDocument25 pagesIncremental Analysis for Engineering Project DecisionsDejene HailuNo ratings yet

- Incremental AnalysisDocument25 pagesIncremental AnalysisAngel MallariNo ratings yet

- Geometry Basics Submitted 9/27Document2 pagesGeometry Basics Submitted 9/27Bijoy SalahuddinNo ratings yet

- Topic: Geometry: (Date of Submission: 27/9/2020)Document2 pagesTopic: Geometry: (Date of Submission: 27/9/2020)Bijoy SalahuddinNo ratings yet

- Accounting For PropertyDocument6 pagesAccounting For PropertyBijoy SalahuddinNo ratings yet

- Breakeven AnalysisDocument1 pageBreakeven AnalysisBijoy SalahuddinNo ratings yet

- 1 Economic, Political and Legal SystemsDocument10 pages1 Economic, Political and Legal SystemsBijoy SalahuddinNo ratings yet

- Mole ChemistryDocument2 pagesMole ChemistryBijoy SalahuddinNo ratings yet

- Recording DepreciationDocument1 pageRecording DepreciationBijoy SalahuddinNo ratings yet

- Group Company WorkingDocument4 pagesGroup Company WorkingBijoy SalahuddinNo ratings yet

- SuriaDocument2 pagesSuriaBijoy SalahuddinNo ratings yet

- OT f6 Example 2Document2 pagesOT f6 Example 2Bijoy SalahuddinNo ratings yet

- Solve Each of The Following Triangles and Give Your Answers Correct To 1 Decimal PlaceDocument1 pageSolve Each of The Following Triangles and Give Your Answers Correct To 1 Decimal PlaceBijoy SalahuddinNo ratings yet

- Audit Practice Manual For ICABDocument223 pagesAudit Practice Manual For ICABhridimamalik80% (5)

- Trading LossDocument1 pageTrading LossBijoy SalahuddinNo ratings yet

- Depreciation O Level NotesDocument5 pagesDepreciation O Level NotesBijoy SalahuddinNo ratings yet

- Recording DepreciationDocument1 pageRecording DepreciationBijoy SalahuddinNo ratings yet

- Bassanio Page 49Document1 pageBassanio Page 49Bijoy SalahuddinNo ratings yet

- Prologue:: Textiles Garments Ready-Made GarmentsDocument1 pagePrologue:: Textiles Garments Ready-Made GarmentsBijoy SalahuddinNo ratings yet

- ACCA F5 Course NotesDocument273 pagesACCA F5 Course NotesLinkon Peter50% (2)

- 3MDocument14 pages3MBijoy SalahuddinNo ratings yet

- Transfer Pricing August 2014 IssueDocument4 pagesTransfer Pricing August 2014 IssueBijoy SalahuddinNo ratings yet

- How To Prevent Failure of Financial InstitutionsDocument55 pagesHow To Prevent Failure of Financial InstitutionsBijoy SalahuddinNo ratings yet

- Meena Bazar tops in reducing absenteeism and turnoverDocument23 pagesMeena Bazar tops in reducing absenteeism and turnoverBijoy Salahuddin100% (2)

- Presentation 1Document9 pagesPresentation 1Bijoy SalahuddinNo ratings yet

- 2title PageDocument1 page2title PageBijoy SalahuddinNo ratings yet

- Capital StructureDocument58 pagesCapital Structuretabi_thegr8No ratings yet

- Marketing Research ProcessDocument2 pagesMarketing Research ProcessBijoy SalahuddinNo ratings yet

- Marketing ResearchDocument4 pagesMarketing ResearchBijoy SalahuddinNo ratings yet

- Marketing Research ProcessDocument4 pagesMarketing Research ProcessBijoy SalahuddinNo ratings yet

- Debt PolicyDocument51 pagesDebt PolicyBijoy SalahuddinNo ratings yet

- Pecking Order TheoryDocument2 pagesPecking Order TheoryBijoy SalahuddinNo ratings yet

- SPV1Document37 pagesSPV1ritu_gnimsNo ratings yet

- Auto Trend ForecasterDocument15 pagesAuto Trend ForecasterherbakNo ratings yet

- Global CorrelationsDocument47 pagesGlobal CorrelationspkanakaNo ratings yet

- Capital Budgeting Techniques ComparisonDocument27 pagesCapital Budgeting Techniques ComparisonSumit KumarNo ratings yet

- Financial Performance Analysis of Kotak Mahindra BankDocument60 pagesFinancial Performance Analysis of Kotak Mahindra Bankvaibhav pachputeNo ratings yet

- Corporate ScorecardDocument36 pagesCorporate Scorecardgkohli79No ratings yet

- CCI - Technical AnalysisDocument20 pagesCCI - Technical AnalysisqzcNo ratings yet

- Shareholders EquityDocument30 pagesShareholders EquityEmmanuelNo ratings yet

- 6359476Document30 pages6359476marianaNo ratings yet

- Etoro FeesDocument6 pagesEtoro FeesAlfa BetaNo ratings yet

- Case 13Document12 pagesCase 13Superb AdnanNo ratings yet

- Jiranna Healthcare AnalysisDocument8 pagesJiranna Healthcare AnalysisEllen MarkNo ratings yet

- Balance Sheet OverviewDocument8 pagesBalance Sheet OverviewRavi Chaurasia100% (1)

- Fund Factsheet For June 2023Document140 pagesFund Factsheet For June 2023ranjithgujjenti123No ratings yet

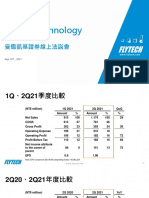

- Flytech TechnologyDocument7 pagesFlytech TechnologyLouis ChenNo ratings yet

- Redemption of Shares NotesDocument14 pagesRedemption of Shares Notesms.AhmedNo ratings yet

- Final-Term Quiz Mankeu Roki Fajri 119108077Document4 pagesFinal-Term Quiz Mankeu Roki Fajri 119108077kota lainNo ratings yet

- Wharton Business Foundations Intro To FiDocument4 pagesWharton Business Foundations Intro To FiasdfghjNo ratings yet

- Book 1 - Foundations of Risk Management PDFDocument19 pagesBook 1 - Foundations of Risk Management PDFmohamed0% (1)

- BBMF 2093 Corporate Finance: Characteristic Line (SML) Slope of The Line To Be 1.67Document6 pagesBBMF 2093 Corporate Finance: Characteristic Line (SML) Slope of The Line To Be 1.67WONG ZI QINGNo ratings yet

- 2022-2023 INTACC3 PAS 1 HandoutsDocument9 pages2022-2023 INTACC3 PAS 1 HandoutsJefferson AlingasaNo ratings yet

- 5 Internal ReconstructionDocument31 pages5 Internal ReconstructionHariom PatidarNo ratings yet

- Decision Usefulness Approach to Financial ReportingDocument24 pagesDecision Usefulness Approach to Financial ReportingAmeliaNo ratings yet

- Investor Protection Rights in IndiaDocument9 pagesInvestor Protection Rights in IndiaGaurav SharmaNo ratings yet

- Calculation of DataDocument3 pagesCalculation of Datafahad fareedNo ratings yet

- Kenmare Architects LTD Kal Was Incorporated and Commenced Operations OnDocument1 pageKenmare Architects LTD Kal Was Incorporated and Commenced Operations OnMiroslav GegoskiNo ratings yet

- Goto Uob 02 Jan 2024 240116 124127Document5 pagesGoto Uob 02 Jan 2024 240116 124127marcellusdarrenNo ratings yet

- Caceres Semilla Case StudyDocument6 pagesCaceres Semilla Case StudyJoyce Anne RenacidoNo ratings yet

- Natural Gas October 2021 Contract OnwardsDocument2 pagesNatural Gas October 2021 Contract Onwardskaran3393No ratings yet

- Equity Research PPT Dhawal Shah-1Document16 pagesEquity Research PPT Dhawal Shah-1Dhaval ShahNo ratings yet