You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

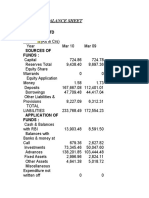

- Balance Sheet: JK Cement LTDDocument3 pagesBalance Sheet: JK Cement LTDHimanshu SharmaNo ratings yet

- Understanding How Demand and Supply Interact to Reach EquilibriumDocument10 pagesUnderstanding How Demand and Supply Interact to Reach EquilibriumSamruddhi DoshettyNo ratings yet

- DRS Business Case - Barnet CouncilDocument161 pagesDRS Business Case - Barnet CouncilMisterMustardNo ratings yet

- Engro's Annual Report 2008Document189 pagesEngro's Annual Report 2008shahidamin1100% (2)

- RIBA Benchmarking 2019 Summary PDFDocument6 pagesRIBA Benchmarking 2019 Summary PDFAlanNo ratings yet

- Shared Services Best PracticesDocument40 pagesShared Services Best PracticesWilliam DANo ratings yet

- Unit 1: IATA Accreditation Requirements: Learning Objectives Key Learning PointsDocument1 pageUnit 1: IATA Accreditation Requirements: Learning Objectives Key Learning PointsSitakanta AcharyaNo ratings yet

- Financial Management Assignment QuestionsDocument3 pagesFinancial Management Assignment QuestionsBabu Ty75% (8)

- 5Document2 pages5ABDUL WAHABNo ratings yet

- AE23 - Strategic Cost Management Ch 6Document18 pagesAE23 - Strategic Cost Management Ch 6Ayana Janica100% (3)

- Analyzing variable costs to estimate profit contribution of a charity eventDocument4 pagesAnalyzing variable costs to estimate profit contribution of a charity eventambermuNo ratings yet

- Donor's Tax A) Basic Principles, Concept and DefinitionDocument4 pagesDonor's Tax A) Basic Principles, Concept and DefinitionAnonymous YNTVcDNo ratings yet

- HkfrspeDocument340 pagesHkfrspeTommy KoNo ratings yet

- City BankDocument328 pagesCity BankKhandaker Amir EntezamNo ratings yet

- p1 Quiz With TheoryDocument16 pagesp1 Quiz With TheoryRica RegorisNo ratings yet

- The Fallacies of Patent Hold Up TheoryDocument56 pagesThe Fallacies of Patent Hold Up TheoryTrevor SoamesNo ratings yet

- IAS 16 by FFQADocument9 pagesIAS 16 by FFQAMohammad Faizan Farooq Qadri Attari0% (1)

- Trust AccountingDocument13 pagesTrust AccountingPriyalaxmi Uma100% (4)

- Financial ManagementDocument238 pagesFinancial ManagementJherzy Henry Elijorde FloresNo ratings yet

- ACC722 Tutorial IIDocument4 pagesACC722 Tutorial IIJohn Tom50% (2)

- Indian Aviation Industry - Indigo AirlinesDocument13 pagesIndian Aviation Industry - Indigo AirlinesArjun Pratap SinghNo ratings yet

- BDocument4 pagesBsakuraNo ratings yet

- Sample Chart of Accounts Feature of Retail Advantage Pos Software, Point of Sale Software, Pos Software, POS System, Retail Management SoftwareDocument3 pagesSample Chart of Accounts Feature of Retail Advantage Pos Software, Point of Sale Software, Pos Software, POS System, Retail Management SoftwareRichardSetiawan0% (1)

- Find Study Resources: Answered Step-By-StepDocument4 pagesFind Study Resources: Answered Step-By-StepJohn Carlos DoringoNo ratings yet

- Nicanor Comptech Service Year End WorksheetDocument5 pagesNicanor Comptech Service Year End WorksheetAshlee DegumbisNo ratings yet

- Top Oil and Gas CompaniesDocument19 pagesTop Oil and Gas CompaniesDenis IoniţăNo ratings yet

- Branch Accounting Examination BankDocument71 pagesBranch Accounting Examination BankNicole TaylorNo ratings yet

- RMCBDocument36 pagesRMCBSharvil Vikram SinghNo ratings yet

- TNK BP RussiaDocument16 pagesTNK BP RussiapheeyonaNo ratings yet

- 2003 RLC Business CalcDocument9 pages2003 RLC Business Calcbob smithNo ratings yet