You might also like

- Digital BankingDocument32 pagesDigital BankingAnshul VermaNo ratings yet

- The WEALTHTECH Book: The FinTech Handbook for Investors, Entrepreneurs and Finance VisionariesFrom EverandThe WEALTHTECH Book: The FinTech Handbook for Investors, Entrepreneurs and Finance VisionariesNo ratings yet

- Electronic Financial Services: Technology and ManagementFrom EverandElectronic Financial Services: Technology and ManagementRating: 5 out of 5 stars5/5 (1)

- Core Banking System Strategy A Complete Guide - 2020 EditionFrom EverandCore Banking System Strategy A Complete Guide - 2020 EditionNo ratings yet

- Catching the FinTech Wave: How to adopt FinTech and Transform Your Financial Planning BusinessFrom EverandCatching the FinTech Wave: How to adopt FinTech and Transform Your Financial Planning BusinessNo ratings yet

- The Power of Mobile Banking: How to Profit from the Revolution in Retail Financial ServicesFrom EverandThe Power of Mobile Banking: How to Profit from the Revolution in Retail Financial ServicesNo ratings yet

- E-Payment Gateway A Complete Guide - 2019 EditionFrom EverandE-Payment Gateway A Complete Guide - 2019 EditionRating: 1 out of 5 stars1/5 (1)

- Breaking Banks: The Innovators, Rogues, and Strategists Rebooting BankingFrom EverandBreaking Banks: The Innovators, Rogues, and Strategists Rebooting BankingNo ratings yet

- The Digital Banking Revolution: How financial technology companies are rapidly transforming the traditional retail banking industry through disruptive innovation.From EverandThe Digital Banking Revolution: How financial technology companies are rapidly transforming the traditional retail banking industry through disruptive innovation.No ratings yet

- Payment Gateway A Complete Guide - 2020 EditionFrom EverandPayment Gateway A Complete Guide - 2020 EditionRating: 4 out of 5 stars4/5 (2)

- The FINTECH Book: The Financial Technology Handbook for Investors, Entrepreneurs and VisionariesFrom EverandThe FINTECH Book: The Financial Technology Handbook for Investors, Entrepreneurs and VisionariesRating: 4.5 out of 5 stars4.5/5 (6)

- Core Banking Partner GuideDocument19 pagesCore Banking Partner GuideClint JacobNo ratings yet

- Fintech and the Remaking of Financial InstitutionsFrom EverandFintech and the Remaking of Financial InstitutionsRating: 5 out of 5 stars5/5 (1)

- Banking Technology May 2019 PDFDocument25 pagesBanking Technology May 2019 PDFJagannath BNo ratings yet

- Digital Transformation In Banking A Complete Guide - 2020 EditionFrom EverandDigital Transformation In Banking A Complete Guide - 2020 EditionNo ratings yet

- IBM Banking: Core Banking Transformation With System ZDocument16 pagesIBM Banking: Core Banking Transformation With System ZIBMBankingNo ratings yet

- Solution Modern Banking UX Retail FISDocument10 pagesSolution Modern Banking UX Retail FISJamesThoNo ratings yet

- Innovation in Indian Banking SectorDocument16 pagesInnovation in Indian Banking SectorKishor CoolNo ratings yet

- Human Engagement in Digital Banking / Author: Nripendra AcharyaDocument7 pagesHuman Engagement in Digital Banking / Author: Nripendra AcharyaBanking100% (4)

- DigitalTalent3 0Document20 pagesDigitalTalent3 0Sue MarksNo ratings yet

- Digital Banking Playbook Final 1Document21 pagesDigital Banking Playbook Final 1hiteshgoel100% (2)

- Unit-4.4-Payment GatewaysDocument8 pagesUnit-4.4-Payment GatewaysShivam SinghNo ratings yet

- Backbase The ROI of Omni Channel WhitepaperDocument21 pagesBackbase The ROI of Omni Channel Whitepaperpk8barnesNo ratings yet

- The Rise of BaaS (Banking As A Service) WhitepaperDocument7 pagesThe Rise of BaaS (Banking As A Service) WhitepaperBeltan TönükNo ratings yet

- Accenture IT Blueprint For The Everyday BankDocument12 pagesAccenture IT Blueprint For The Everyday BankCristian RoscaNo ratings yet

- Overview of Mobile Payments WhitepaperDocument14 pagesOverview of Mobile Payments WhitepapertderuvoNo ratings yet

- FinTech Lending in Indonesia - PWC ReportDocument34 pagesFinTech Lending in Indonesia - PWC ReportmayurNo ratings yet

- L2 Merchant AcquiringV1.0Document59 pagesL2 Merchant AcquiringV1.0Shweta AgrawalNo ratings yet

- Regulatory Onboarding The Fenergo Way USDocument22 pagesRegulatory Onboarding The Fenergo Way USUtku CetinNo ratings yet

- Innovation in Retail BankingDocument102 pagesInnovation in Retail BankingAlina DamaschinNo ratings yet

- Mobile Payment Business Model Research Report FINALDocument34 pagesMobile Payment Business Model Research Report FINALvia_amiko0% (1)

- Emerging Technologies Disrupting The Financial Sector PDFDocument56 pagesEmerging Technologies Disrupting The Financial Sector PDFvaragg24No ratings yet

- RBI Payment Gateway Guidelines in IndiaDocument14 pagesRBI Payment Gateway Guidelines in IndiaDeepak SinghNo ratings yet

- Credit Digitization For Credit Management Presentation 23jul19Document21 pagesCredit Digitization For Credit Management Presentation 23jul19Chidozie Farsight100% (1)

- Ezbob SME Digital Lending Product DescriptionDocument34 pagesEzbob SME Digital Lending Product DescriptionMinhminh NguyenNo ratings yet

- What Is Open Banking GuideDocument18 pagesWhat Is Open Banking GuideMiguelAngelHernandezNo ratings yet

- Going Digital - The Banking Transformation Road MapDocument13 pagesGoing Digital - The Banking Transformation Road MapHardikSinghvi100% (2)

- A Case For A Single Loan Origination System For Core Banking ProductsDocument5 pagesA Case For A Single Loan Origination System For Core Banking ProductsCognizant100% (1)

- Fintech Landscape OverviewDocument1 pageFintech Landscape OverviewJason NikolaouNo ratings yet

- 4 A Guide To Payment Gateways PDFDocument3 pages4 A Guide To Payment Gateways PDFMishel Carrion lopezNo ratings yet

- Core BankingDocument37 pagesCore Bankingnwani25No ratings yet

- Payments 101Document37 pagesPayments 101David Leeman100% (1)

- Quotes of LifeDocument88 pagesQuotes of LifeMicah Smith100% (1)

- MKT PowerDocument1 pageMKT PowerMicah SmithNo ratings yet

- HPCL Procurement Manual NewDocument446 pagesHPCL Procurement Manual NewMicah SmithNo ratings yet

- NAT Sample Paper - 2 Year 2021 - Paper PDFDocument8 pagesNAT Sample Paper - 2 Year 2021 - Paper PDFDhruv GuptaNo ratings yet

- MKT AnalysisDocument2 pagesMKT AnalysisMicah SmithNo ratings yet

- fx-570 - 991ES - PLUS - EN ManualDocument46 pagesfx-570 - 991ES - PLUS - EN ManualJack Skb SmithNo ratings yet

- Arbitration Laws in India PDFDocument58 pagesArbitration Laws in India PDFdsnm777No ratings yet

- India's Goods and Service TaxDocument9 pagesIndia's Goods and Service TaxMicah SmithNo ratings yet

- 1) PF Portability: Every Time You Join A New Company, You Were Given A New PFDocument2 pages1) PF Portability: Every Time You Join A New Company, You Were Given A New PFMicah SmithNo ratings yet

- Inspiring Leadership Through Effective CommunicationDocument11 pagesInspiring Leadership Through Effective CommunicationMicah SmithNo ratings yet

- Presentation - Business Etiquette and ProtocolDocument45 pagesPresentation - Business Etiquette and ProtocolMicah SmithNo ratings yet

- Fms Corporate Restructuring 2013 WinterDocument2 pagesFms Corporate Restructuring 2013 WinterMicah SmithNo ratings yet

- Reasoning Book - Banking ShortcutsDocument126 pagesReasoning Book - Banking ShortcutsMicah Smith0% (1)

- FMCG PropertiesDocument4 pagesFMCG PropertiesMicah SmithNo ratings yet

- EffectivenessDocument9 pagesEffectivenessMicah SmithNo ratings yet

- Compendium of Vigilance GuidelinesDocument165 pagesCompendium of Vigilance GuidelinesMicah SmithNo ratings yet

- To Whom It May ConcernDocument1 pageTo Whom It May ConcernMicah SmithNo ratings yet

- 1) PF Portability: Every Time You Join A New Company, You Were Given A New PFDocument2 pages1) PF Portability: Every Time You Join A New Company, You Were Given A New PFMicah SmithNo ratings yet

- EffectivenessDocument9 pagesEffectivenessMicah SmithNo ratings yet

- Products Portfolio: The Following Are The Dimensions For Both MS Conduit and GL ConduitDocument2 pagesProducts Portfolio: The Following Are The Dimensions For Both MS Conduit and GL ConduitMicah SmithNo ratings yet

- Market PropertiesDocument3 pagesMarket PropertiesMicah SmithNo ratings yet

- Open Mkt.Document1 pageOpen Mkt.Micah SmithNo ratings yet

- FMCG MarketDocument3 pagesFMCG MarketMicah SmithNo ratings yet

- Mobile Phones SelectionDocument5 pagesMobile Phones SelectionMicah SmithNo ratings yet

- 1) PF Portability: Every Time You Join A New Company, You Were Given A New PFDocument2 pages1) PF Portability: Every Time You Join A New Company, You Were Given A New PFMicah SmithNo ratings yet

- Comp Circ Ul Cte 2013Document112 pagesComp Circ Ul Cte 2013Micah SmithNo ratings yet

- Analysis of Domestic ProductsDocument2 pagesAnalysis of Domestic ProductsMicah SmithNo ratings yet

- Evolution of Online Consumer Services IndustryDocument26 pagesEvolution of Online Consumer Services IndustryMicah SmithNo ratings yet

- Financ Il ApplicationDocument27 pagesFinanc Il ApplicationMicah SmithNo ratings yet

- Regulations On E-CigretteDocument4 pagesRegulations On E-CigretteMicah SmithNo ratings yet

- IATA TaxDocument1,510 pagesIATA TaxMiguelRevera100% (1)

- UCT Handbook 12 2019 StudentFees PDFDocument132 pagesUCT Handbook 12 2019 StudentFees PDFNjabulo DlaminiNo ratings yet

- Banccassurance Project For Banking & InsuranceDocument32 pagesBanccassurance Project For Banking & Insuranceramprabu88No ratings yet

- Term Project: Credit Card BusinessDocument17 pagesTerm Project: Credit Card BusinessOnur YılmazNo ratings yet

- Hyd LodgeDocument5 pagesHyd LodgeRammohanreddy RajidiNo ratings yet

- Business Sale Agreement TemplateDocument2 pagesBusiness Sale Agreement TemplatecmdelrioNo ratings yet

- Charles Reed BishopDocument4 pagesCharles Reed BishopLinas KondratasNo ratings yet

- Gloria Institute of Science and Technology Gloria, Oriental MindoroDocument4 pagesGloria Institute of Science and Technology Gloria, Oriental MindoroGist Gloria TesdaNo ratings yet

- How To Deposit Your SLP From Ronin To BinanceDocument8 pagesHow To Deposit Your SLP From Ronin To BinanceGaeyden Meira MosadaNo ratings yet

- Should We Use Cash or Credit Card When TravellingDocument2 pagesShould We Use Cash or Credit Card When TravellingNana SupriatnaNo ratings yet

- Assessment of Working Capital Requirements Form Ii: Operating StatementDocument12 pagesAssessment of Working Capital Requirements Form Ii: Operating StatementMD.SAFIKUL MONDALNo ratings yet

- Payment System ReportDocument21 pagesPayment System ReportChristian Grey ChantiacoNo ratings yet

- VISADocument74 pagesVISAዝምታ ተሻለNo ratings yet

- Final SynthesisDocument6 pagesFinal Synthesisapi-256072244No ratings yet

- Bank Advice: Name UIDDocument8 pagesBank Advice: Name UIDS1626No ratings yet

- Interest A Bane For SocietyDocument4 pagesInterest A Bane For SocietyMohd Zubair AhmadNo ratings yet

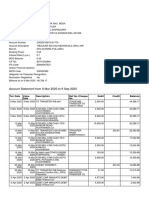

- Bank Statement09-2020Document6 pagesBank Statement09-2020Tnt SolutionsNo ratings yet

- Karthikeyan G - Updated ResumeDocument7 pagesKarthikeyan G - Updated ResumeKarthikeyan GangadharanNo ratings yet

- KYC Guide (1) - 2Document65 pagesKYC Guide (1) - 2SikeNo ratings yet

- Damon K. Roberts Plea AgreementDocument2 pagesDamon K. Roberts Plea AgreementWashington ExaminerNo ratings yet

- Mca 21 Case StudyDocument7 pagesMca 21 Case StudySapna SharmaNo ratings yet

- Journalizing in Periodic Inventory (Exercises)Document15 pagesJournalizing in Periodic Inventory (Exercises)Joselyn AmonNo ratings yet

- QA SIPACKS in Business Finance Q3 W1 7Document91 pagesQA SIPACKS in Business Finance Q3 W1 7Roan DiracoNo ratings yet

- Walter BagehotDocument4 pagesWalter BagehotdantevantesNo ratings yet

- Board of Inland Revenue v. HaddockDocument2 pagesBoard of Inland Revenue v. HaddockJ. JimenezNo ratings yet

- s90 Users Guide 1 00 01Document250 pagess90 Users Guide 1 00 01Wijaksana DewaNo ratings yet

- 2A COMMUNICATIVE Are You A Saver or A Spender?Document1 page2A COMMUNICATIVE Are You A Saver or A Spender?B McNo ratings yet

- Pioneering Portfolio ManagementDocument6 pagesPioneering Portfolio ManagementGeorge KyriakoulisNo ratings yet

- Human Resources Director in Los Angeles CA Resume Trudy WestDocument2 pagesHuman Resources Director in Los Angeles CA Resume Trudy WestTrudyWestNo ratings yet

- Citi BankDocument12 pagesCiti BankAsad MazharNo ratings yet