You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Money Master The GameDocument48 pagesMoney Master The GameSimon and Schuster72% (18)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Session 2 - Deductions From Gross Income, Part 1Document10 pagesSession 2 - Deductions From Gross Income, Part 1ABBIE GRACE DELA CRUZNo ratings yet

- Extruder Screw Desing Basics PDFDocument54 pagesExtruder Screw Desing Basics PDFAlvaro Fernando Reyes Castañeda100% (6)

- Dynisco Extrusion Handbook C0d23eDocument293 pagesDynisco Extrusion Handbook C0d23eSimas Servutas50% (2)

- Essentials of Human Resource ManagementDocument17 pagesEssentials of Human Resource Managementashbak2006#zikir#scribd#2009No ratings yet

- Environmental Problems and Sustainability Chapter SummaryDocument41 pagesEnvironmental Problems and Sustainability Chapter SummaryTim Weaver75% (4)

- DLL ENTREP Week 9Document6 pagesDLL ENTREP Week 9KATHERINE JOY ZARANo ratings yet

- Tracxn Startup Research Global SaaS India Landscape May 2016 1Document125 pagesTracxn Startup Research Global SaaS India Landscape May 2016 1Shikha GuptaNo ratings yet

- Polymer Additive Reference StandardsDocument36 pagesPolymer Additive Reference StandardsvasucristalNo ratings yet

- 14 Sustainable TourismDocument17 pages14 Sustainable TourismIwan Firman WidiyantoNo ratings yet

- Chapter 11 Partnership FormationDocument10 pagesChapter 11 Partnership FormationJo Faula BelleNo ratings yet

- Polymerscan: Americas Polymer Spot Price AssessmentsDocument28 pagesPolymerscan: Americas Polymer Spot Price AssessmentsmcontrerjNo ratings yet

- Group 3 Presentation - Training Needs AnalysisDocument13 pagesGroup 3 Presentation - Training Needs AnalysisHassaan Bin KhalidNo ratings yet

- Polymerscan: Americas Polymer Spot Price AssessmentsDocument29 pagesPolymerscan: Americas Polymer Spot Price AssessmentsmcontrerjNo ratings yet

- Po 20140924Document29 pagesPo 20140924mcontrerjNo ratings yet

- Aditivo AglomeranteDocument11 pagesAditivo AglomerantemcontrerjNo ratings yet

- ScrewDocument9 pagesScrewmcontrerjNo ratings yet

- Po 20140910Document30 pagesPo 20140910mcontrerjNo ratings yet

- Platts PP 27 May 2015Document11 pagesPlatts PP 27 May 2015mcontrerjNo ratings yet

- Platts Pe 24 June 2015Document12 pagesPlatts Pe 24 June 2015mcontrerjNo ratings yet

- Platts PVC 23 Sept 2015Document10 pagesPlatts PVC 23 Sept 2015mcontrerjNo ratings yet

- Platts Pe 24 June 2015Document12 pagesPlatts Pe 24 June 2015mcontrerjNo ratings yet

- Belgian Punishment Novel Explores WWII Era SocietyDocument5 pagesBelgian Punishment Novel Explores WWII Era SocietymcontrerjNo ratings yet

- Platts PVC 29 July 2015Document10 pagesPlatts PVC 29 July 2015mcontrerjNo ratings yet

- Platts PP 24 June 2015Document11 pagesPlatts PP 24 June 2015mcontrerjNo ratings yet

- Platts PP 26 August 2015Document11 pagesPlatts PP 26 August 2015mcontrerjNo ratings yet

- Platts PVC 26 August 2015Document10 pagesPlatts PVC 26 August 2015mcontrerjNo ratings yet

- Platts PP 29 July 2015Document11 pagesPlatts PP 29 July 2015mcontrerjNo ratings yet

- SAP 120-200 MeshDocument1 pageSAP 120-200 MeshmcontrerjNo ratings yet

- Platts PE 23 Sept 2015Document14 pagesPlatts PE 23 Sept 2015mcontrerjNo ratings yet

- Platts PE 26 August 2015Document13 pagesPlatts PE 26 August 2015mcontrerjNo ratings yet

- Platts PE 29 July 2015Document14 pagesPlatts PE 29 July 2015mcontrerjNo ratings yet

- Platts PP 23 Sept 2015Document11 pagesPlatts PP 23 Sept 2015mcontrerjNo ratings yet

- Role of Rheology in ExtrusionDocument25 pagesRole of Rheology in Extrusionmshussein2009No ratings yet

- Role of Rheology in ExtrusionDocument25 pagesRole of Rheology in Extrusionmshussein2009No ratings yet

- NW 15092014 000000 PDFDocument11 pagesNW 15092014 000000 PDFmcontrerjNo ratings yet

- Major Application Areas of BentoniteDocument125 pagesMajor Application Areas of BentoniteApsari Puspita AiniNo ratings yet

- Benefits of Workplace DiversityDocument3 pagesBenefits of Workplace DiversitykathNo ratings yet

- Inclusive Growth and Gandhi's Swaraj ComparedDocument18 pagesInclusive Growth and Gandhi's Swaraj ComparedRubina PradhanNo ratings yet

- CSG International Corporate BrochureDocument18 pagesCSG International Corporate BrochurePrabir MishraNo ratings yet

- National Bank For Agriculture and Rural Development (NABARD)Document58 pagesNational Bank For Agriculture and Rural Development (NABARD)kavita choudharyNo ratings yet

- Mandara Report 2019Document59 pagesMandara Report 2019Tony MumvuriNo ratings yet

- Accounting For Income Taxes: About This Chapter!Document9 pagesAccounting For Income Taxes: About This Chapter!sabithpaulNo ratings yet

- Barangay Annual Gender and Development (Gad) Plan and Budget FY 2021Document8 pagesBarangay Annual Gender and Development (Gad) Plan and Budget FY 2021HELEN CASIANONo ratings yet

- Logistics SsDocument18 pagesLogistics SsCarla Flor LosiñadaNo ratings yet

- JGB v4n1 17Document8 pagesJGB v4n1 17Roel SisonNo ratings yet

- Zero Base BudgetingDocument15 pagesZero Base BudgetingSumitasNo ratings yet

- Anan University case study examines IT infrastructure relationshipsDocument3 pagesAnan University case study examines IT infrastructure relationshipsSam PatriceNo ratings yet

- Level 1: New Century Mathematics (Second Edition) S3 Question Bank 3A Chapter 3 Percentages (II)Document27 pagesLevel 1: New Century Mathematics (Second Edition) S3 Question Bank 3A Chapter 3 Percentages (II)raydio 4No ratings yet

- Shobha DevelopersDocument212 pagesShobha DevelopersJames TownsendNo ratings yet

- Nuss Company ProfileDocument3 pagesNuss Company ProfiletelecomstuffsNo ratings yet

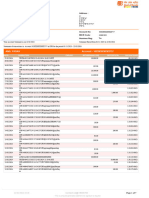

- OpTransactionHistoryUX522 02 2024Document7 pagesOpTransactionHistoryUX522 02 2024Praveen SainiNo ratings yet

- Ust 2014 Bar Q Suggested Answers Civil LawDocument15 pagesUst 2014 Bar Q Suggested Answers Civil LawKevin AmanteNo ratings yet

- DS112 Development Perspectives I Course OverviewDocument68 pagesDS112 Development Perspectives I Course OverviewDanford DanfordNo ratings yet

- Accounting MemeDocument2 pagesAccounting MemeIan Jay DescutidoNo ratings yet

- Appointment Letter: Teamlease Services Limited., Cin No. L74140Ka2000Plc118395Document4 pagesAppointment Letter: Teamlease Services Limited., Cin No. L74140Ka2000Plc118395amrit barmanNo ratings yet

- Understanding Microeconomics FundamentalsDocument3 pagesUnderstanding Microeconomics FundamentalsAnira Rosli0% (1)

- A Quick Guide To The Program DPro PDFDocument32 pagesA Quick Guide To The Program DPro PDFstouraNo ratings yet