You might also like

- Accounting PrinciplesDocument9 pagesAccounting PrinciplesJodie Ann PajacNo ratings yet

- Introduction to Accounting Principles: 10 Basic ConceptsDocument9 pagesIntroduction to Accounting Principles: 10 Basic ConceptsCaren Que ViniegraNo ratings yet

- Introduction To Accounting PrinciplesDocument3 pagesIntroduction To Accounting PrinciplesZvioule Ma FuentesNo ratings yet

- GAAP Principles SdfsdfsdfsdfsdfwerwerertrtgrffghDocument4 pagesGAAP Principles SdfsdfsdfsdfsdfwerwerertrtgrffghCorolla SedanNo ratings yet

- Introduction To Accounting PrinciplesDocument9 pagesIntroduction To Accounting PrinciplesLyca SorianoNo ratings yet

- Introduction To Accounting Principles ADocument10 pagesIntroduction To Accounting Principles AYuj Cuares CervantesNo ratings yet

- 1 Principle of Acctancy 1819-1Document3 pages1 Principle of Acctancy 1819-1george josephNo ratings yet

- Basic Accounting Principles and GAAP ExplainedDocument4 pagesBasic Accounting Principles and GAAP ExplainedbayrazNo ratings yet

- Introduction to Accounting PrinciplesDocument7 pagesIntroduction to Accounting PrinciplesAnand PrasadNo ratings yet

- Introduction To Accounting PrinciplesDocument4 pagesIntroduction To Accounting PrinciplesJess CaburnayNo ratings yet

- Understanding Accounting Principles and GAAPDocument8 pagesUnderstanding Accounting Principles and GAAPNitish BatraNo ratings yet

- Accouting PrinciplesDocument5 pagesAccouting PrinciplesPriyanka RawoolNo ratings yet

- Introduction To Accounting PrinciplesDocument9 pagesIntroduction To Accounting Principlesanon_632966032No ratings yet

- Financial Accounting Standards Board (FASB) : Introduction To Accounting PrinciplesDocument4 pagesFinancial Accounting Standards Board (FASB) : Introduction To Accounting PrinciplesJasmine TorioNo ratings yet

- Accounting Principles Are Classified Into Two CategoriesDocument4 pagesAccounting Principles Are Classified Into Two CategoriesRanjan Bhagat0% (1)

- Basic Accounting Principle What It Means in Relationship To A Financial StatementDocument3 pagesBasic Accounting Principle What It Means in Relationship To A Financial Statementthareendra1No ratings yet

- RODRIGUEZ, Marion Patricia L. 4LM3Document5 pagesRODRIGUEZ, Marion Patricia L. 4LM3Patricia RodriguezNo ratings yet

- GAAP Accounting Principles ExplainedDocument8 pagesGAAP Accounting Principles ExplainedKrish ChandranNo ratings yet

- Accounting Principles Every Student Should KnowDocument4 pagesAccounting Principles Every Student Should KnowRc M. Santiago IINo ratings yet

- Accounting Principles and Concepts LectureDocument9 pagesAccounting Principles and Concepts LectureMary De JesusNo ratings yet

- Economic Entity Assumption: Ended December 31, 2010Document3 pagesEconomic Entity Assumption: Ended December 31, 2010Rizwan Ahmed ShahbazNo ratings yet

- Introduction To Accounting PrinciplesDocument6 pagesIntroduction To Accounting PrinciplesDanice GanNo ratings yet

- 10 Key Accounting PrinciplesDocument3 pages10 Key Accounting PrinciplesAbdullahNo ratings yet

- Basic Accounting Principles and GuidelinesDocument3 pagesBasic Accounting Principles and GuidelinesJoseph Dalimot SeyerNo ratings yet

- What Is Financial AccountingDocument9 pagesWhat Is Financial Accountingjohn mhrjnNo ratings yet

- Accounting Principle, Concepts & AssumptionsDocument3 pagesAccounting Principle, Concepts & AssumptionsdalanDANICA100% (1)

- Accounting Princple: 1. Economic Entity AssumptionDocument3 pagesAccounting Princple: 1. Economic Entity AssumptionjoeyNo ratings yet

- Definition of 'Accrual Accounting'Document8 pagesDefinition of 'Accrual Accounting'satish_ban91No ratings yet

- Basics Accounting PrinciplesDocument22 pagesBasics Accounting PrincipleshsaherwanNo ratings yet

- Gaap:: The Generally Accepted Accounting Principles (GAAP)Document4 pagesGaap:: The Generally Accepted Accounting Principles (GAAP)Uzair KhanNo ratings yet

- ACCOUNTING ENTITY ASSUMPTION explainedDocument8 pagesACCOUNTING ENTITY ASSUMPTION explainedJonalyn abesNo ratings yet

- Accounting Standard-1: Disclosure of Accounting PoliciesDocument8 pagesAccounting Standard-1: Disclosure of Accounting Policieskeshvika singlaNo ratings yet

- GAAPs: Theory base of accountingDocument22 pagesGAAPs: Theory base of accountingDivija MalhotraNo ratings yet

- Eco Unit 4 FullDocument41 pagesEco Unit 4 FullBubbleNo ratings yet

- Accounting Principles, Concepts & Three Golden RulesDocument17 pagesAccounting Principles, Concepts & Three Golden RulesmvinayakamNo ratings yet

- Top 13 accounting principlesDocument7 pagesTop 13 accounting principlesDEVERLYN SAQUIDONo ratings yet

- Advance Accounting TheoryDocument27 pagesAdvance Accounting TheorykailashdhirwaniNo ratings yet

- Chapter 5Document8 pagesChapter 5Janah MirandaNo ratings yet

- Group 2 11-Amber - PPT Lesson 3Document16 pagesGroup 2 11-Amber - PPT Lesson 3kazumaNo ratings yet

- Lesson-2 Generally Accepted Accounting Principles and Accounting StandardsDocument10 pagesLesson-2 Generally Accepted Accounting Principles and Accounting StandardsKarthigeyan Balasubramaniam100% (1)

- Lecture One Role of Accounting in SocietyDocument10 pagesLecture One Role of Accounting in SocietyJagadeep Reddy BhumireddyNo ratings yet

- Who Determines Gaap and What It ReallyDocument4 pagesWho Determines Gaap and What It ReallysajidsfaNo ratings yet

- Quiz Theory AccountingDocument8 pagesQuiz Theory Accountingjucia wantaNo ratings yet

- Ov Ov Ov OvDocument8 pagesOv Ov Ov Ovdeepak_rathod_5No ratings yet

- Inbound 3522308407029868205Document18 pagesInbound 3522308407029868205KupalNo ratings yet

- Acc Assign1Document24 pagesAcc Assign1chandresh_johnsonNo ratings yet

- Fundamentals of Accounting Concepts (39Document54 pagesFundamentals of Accounting Concepts (39Rheen Clarin100% (3)

- Convention of Conservatism: Definition of The 'Going Concern' ConceptDocument14 pagesConvention of Conservatism: Definition of The 'Going Concern' ConceptForam ShahNo ratings yet

- Role of Accounting in SocietyDocument9 pagesRole of Accounting in SocietyAbdul GafoorNo ratings yet

- Accounting Concepts and PrinciplesDocument5 pagesAccounting Concepts and PrinciplesKenneth RamosNo ratings yet

- Acc1 Lesson Week6Document20 pagesAcc1 Lesson Week6KeiNo ratings yet

- Theory Based Accounting - Short Notes - (Aarambh 2.0 2024)Document17 pagesTheory Based Accounting - Short Notes - (Aarambh 2.0 2024)sidhant singhNo ratings yet

- Financial AccountingDocument27 pagesFinancial AccountingShreya KanjariyaNo ratings yet

- Generally Accepted Accounting PrinciplesDocument3 pagesGenerally Accepted Accounting PrinciplesMuhammad Shaukat NaseebNo ratings yet

- Financial Accounting Self NotesDocument10 pagesFinancial Accounting Self NotesShailendra Rajput100% (1)

- Chapter 6 - Accounting Concepts and PrinciplesDocument19 pagesChapter 6 - Accounting Concepts and PrinciplesRyah Louisse E. ParabolesNo ratings yet

- Assignment On Accouting Prin-Assum-RulesDocument4 pagesAssignment On Accouting Prin-Assum-RulesNazimRezaNo ratings yet

- Assignment On GAAP, AccountingDocument7 pagesAssignment On GAAP, AccountingAsma Hameed50% (2)

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Financial Statements: A Simplified Easy Accounting and Business Owner Guide to Understanding and Creating Financial ReportsFrom EverandFinancial Statements: A Simplified Easy Accounting and Business Owner Guide to Understanding and Creating Financial ReportsNo ratings yet

- Dining Room DescriptionDocument8 pagesDining Room DescriptionAamir KhanNo ratings yet

- The Influence of Firm's and Owner's Characteristics On Bank Financing and Trade Credit UseDocument8 pagesThe Influence of Firm's and Owner's Characteristics On Bank Financing and Trade Credit UseAamir KhanNo ratings yet

- Primary - 1 - Lesson Plan Cube and CuboidDocument5 pagesPrimary - 1 - Lesson Plan Cube and CuboidAamir KhanNo ratings yet

- Integrating TAM and TOE Frameworks and Expanding Their Characteristic Constructs For E-Commerce Adoption by SMEsDocument18 pagesIntegrating TAM and TOE Frameworks and Expanding Their Characteristic Constructs For E-Commerce Adoption by SMEsAamir KhanNo ratings yet

- Koul - A Systematic Review of Technology Adoption Frameworks and Their ApplicationsDocument8 pagesKoul - A Systematic Review of Technology Adoption Frameworks and Their Applicationsafca32No ratings yet

- ''1''faris Nasif AL-Shubiri (2012)Document6 pages''1''faris Nasif AL-Shubiri (2012)Aamir KhanNo ratings yet

- Koul - A Systematic Review of Technology Adoption Frameworks and Their ApplicationsDocument8 pagesKoul - A Systematic Review of Technology Adoption Frameworks and Their Applicationsafca32No ratings yet

- Appearance PDFDocument5 pagesAppearance PDFAamir KhanNo ratings yet

- Financial Wealth, Socioemotional Wealth and Ipo Underpricing in Family Firms: A Two-Stage Gamble ModelDocument60 pagesFinancial Wealth, Socioemotional Wealth and Ipo Underpricing in Family Firms: A Two-Stage Gamble ModelAamir KhanNo ratings yet

- M.phi PHD Thesis FormatDocument37 pagesM.phi PHD Thesis FormatAamir KhanNo ratings yet

- Koul - A Systematic Review of Technology Adoption Frameworks and Their ApplicationsDocument8 pagesKoul - A Systematic Review of Technology Adoption Frameworks and Their Applicationsafca32No ratings yet

- Research Scientist MidlevelDocument2 pagesResearch Scientist MidlevelAamir KhanNo ratings yet

- BNK601BankingLawsPracticesHandoutsLectureno 1to45bywww Virtualians PK PDFDocument297 pagesBNK601BankingLawsPracticesHandoutsLectureno 1to45bywww Virtualians PK PDFMuslima KanwalNo ratings yet

- M.phi PHD Thesis FormatDocument37 pagesM.phi PHD Thesis FormatAamir KhanNo ratings yet

- CSR Research ArticleDocument13 pagesCSR Research ArticleAamir KhanNo ratings yet

- BNK601BankingLawsPracticesHandoutsLectureno 1to45bywww Virtualians PK PDFDocument297 pagesBNK601BankingLawsPracticesHandoutsLectureno 1to45bywww Virtualians PK PDFMuslima KanwalNo ratings yet

- GMDH selective ensemble hybrid model for China energy consumptionDocument28 pagesGMDH selective ensemble hybrid model for China energy consumptionAamir KhanNo ratings yet

- Manzil PDFDocument31 pagesManzil PDFwiqiNo ratings yet

- M.phi PHD Thesis FormatDocument37 pagesM.phi PHD Thesis FormatAamir KhanNo ratings yet

- Application Form AWKUM-NewDocument3 pagesApplication Form AWKUM-NewAamir KhanNo ratings yet

- 500 Solved MCQs of Money BankingDocument230 pages500 Solved MCQs of Money Bankingamir100% (3)

- Financial Statement Analysis: 1 Prepared by Adnan Ali & Amir Ullah Lectures at Qurtuba University, Peshawar CampusDocument5 pagesFinancial Statement Analysis: 1 Prepared by Adnan Ali & Amir Ullah Lectures at Qurtuba University, Peshawar CampusAamir KhanNo ratings yet

- Advt - No - 9-2014Document5 pagesAdvt - No - 9-2014burhan_qureshiNo ratings yet

- Liabilities Duties of Incoming and Outgoing PartnersDocument1 pageLiabilities Duties of Incoming and Outgoing PartnersAamir KhanNo ratings yet

- Present Value Concept ExplainedDocument10 pagesPresent Value Concept ExplainedAamir KhanNo ratings yet

- Autocorrelation by Ijaz 3rd MonthlyDocument14 pagesAutocorrelation by Ijaz 3rd MonthlyAamir KhanNo ratings yet

- Six Steps For Hypothesis TestsDocument1 pageSix Steps For Hypothesis TestsAamir KhanNo ratings yet

- Autocorrelation by Ijaz 3rd MonthlyDocument14 pagesAutocorrelation by Ijaz 3rd MonthlyAamir KhanNo ratings yet

- HBL Final ReportDocument31 pagesHBL Final ReportAamir KhanNo ratings yet

- Financial Accounting Exam QuestionsDocument9 pagesFinancial Accounting Exam QuestionsdayahNo ratings yet

- PartnershipDocument9 pagesPartnershipGrace A. ManaloNo ratings yet

- Budget in HousekeepingDocument15 pagesBudget in Housekeepingtanmay jain100% (1)

- CVP Bba 2020Document58 pagesCVP Bba 2020Loreen Maya0% (1)

- B75C0 - FA - Course PackDocument123 pagesB75C0 - FA - Course PackHemant MULRAJ Merchant,No ratings yet

- Computerised Accounting SystemDocument196 pagesComputerised Accounting SystemSaiqua Parveen100% (2)

- Liquor 20 ReportDocument77 pagesLiquor 20 ReportinforumdocsNo ratings yet

- Week 2 Quiz Answers - Explanations PDFDocument6 pagesWeek 2 Quiz Answers - Explanations PDFanar82% (11)

- JurisDocument32 pagesJurisEdz ZVNo ratings yet

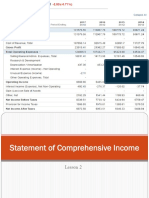

- Lesson 2 Statement of Comprehensive IncomeDocument23 pagesLesson 2 Statement of Comprehensive IncomePaulette Sarno80% (5)

- Income Statement Based Off Khan Academy (Also For Accounting)Document2 pagesIncome Statement Based Off Khan Academy (Also For Accounting)Sachi LoreigneNo ratings yet

- Review and Evaluate/examine Financial Management Processes: Submission DetailsDocument10 pagesReview and Evaluate/examine Financial Management Processes: Submission DetailsRichard HS Kim100% (1)

- Financial Analysis & Inventory Management in WIMCODocument65 pagesFinancial Analysis & Inventory Management in WIMCOMayankNo ratings yet

- 4417 - Hiep Nam Le - SITXFIN004Document12 pages4417 - Hiep Nam Le - SITXFIN004jsoin0% (1)

- CCASBBAR13Document57 pagesCCASBBAR13Wall HackNo ratings yet

- DTP Full NotesDocument114 pagesDTP Full NotesCHAITHRANo ratings yet

- As10 SolutionDocument17 pagesAs10 SolutionAman RayNo ratings yet

- Chap014 Financial and Managerial Accountting WilliamsDocument57 pagesChap014 Financial and Managerial Accountting WilliamsOther Side100% (1)

- Chapter 4. Understanding The Cash Flow Statement Item AmountDocument4 pagesChapter 4. Understanding The Cash Flow Statement Item AmountThu PhạmNo ratings yet

- ACYAVA1 Comprehensive Examination Quiz Instructions: Started: Jun 4 at 13:00Document37 pagesACYAVA1 Comprehensive Examination Quiz Instructions: Started: Jun 4 at 13:00Joel Kennedy BalanayNo ratings yet

- Cost AccountingDocument53 pagesCost Accountingpritika mishraNo ratings yet

- Compliances: Overview of Year End Under Companies Act, 2013Document89 pagesCompliances: Overview of Year End Under Companies Act, 2013Vijay MelwaniNo ratings yet

- WF 761 FMLDocument296 pagesWF 761 FMLhellboysatyaNo ratings yet

- Naming and Filing Audit Evidence GuideDocument8 pagesNaming and Filing Audit Evidence GuideGellie De VeraNo ratings yet

- Bản sao của Câu hỏi trắc nghiệm (bản đánh sẵn đáp án)Document30 pagesBản sao của Câu hỏi trắc nghiệm (bản đánh sẵn đáp án)HẬU TRẦN TOÀN XUÂNNo ratings yet

- Rising Chick 120 Heads Broiler Production: Irish Mae JovitaDocument28 pagesRising Chick 120 Heads Broiler Production: Irish Mae JovitaIrish Mae JovitaNo ratings yet

- Accounting 12 Chapter 8Document30 pagesAccounting 12 Chapter 8cecilia capiliNo ratings yet

- NEELA POORNIMA 2013080 Report - NeelaPoornima EsakkiDocument51 pagesNEELA POORNIMA 2013080 Report - NeelaPoornima EsakkiSherlyn SNo ratings yet

- Advanced Accounting - 2015 (Chapter 17) Multiple Choice Solution (Part I)Document1 pageAdvanced Accounting - 2015 (Chapter 17) Multiple Choice Solution (Part I)John Carlos DoringoNo ratings yet

- Jayakody Hardware Stores Trial Balance and Financial StatementsDocument4 pagesJayakody Hardware Stores Trial Balance and Financial StatementsmonteNo ratings yet