You might also like

- WARC 100 Summary of Results PDFDocument18 pagesWARC 100 Summary of Results PDFNguyênNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Mindset: If You Like This Summary, Buy The BookDocument16 pagesMindset: If You Like This Summary, Buy The BookRajeev K Nair100% (8)

- Academic Question Paper Test 9Document21 pagesAcademic Question Paper Test 9Berry BlueNo ratings yet

- Ielts Teachers GuideDocument32 pagesIelts Teachers Guidesuccess4everNo ratings yet

- Job CostingDocument10 pagesJob CostingGeejayFerrerPaculdoNo ratings yet

- Chap 004Document42 pagesChap 004NguyênNo ratings yet

- 1298 English ExercisesDocument126 pages1298 English ExercisesNguyênNo ratings yet

- Chap 020Document56 pagesChap 020NguyênNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

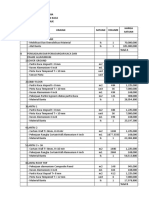

- RENCANA ANGGARAN BIAYA PEMASANGAN KACA PROYEK GEDUNG 21 AVENUEDocument5 pagesRENCANA ANGGARAN BIAYA PEMASANGAN KACA PROYEK GEDUNG 21 AVENUEAswal Al-fakirNo ratings yet

- Credit AppraisalDocument14 pagesCredit AppraisalRishabh Jain0% (1)

- A Project Report On Working Capital Management at Hero Honda PVT LTDDocument73 pagesA Project Report On Working Capital Management at Hero Honda PVT LTDNagireddy Kalluri75% (4)

- Cables Qutation-NationalDocument2 pagesCables Qutation-NationalMuhammad Abubakar QureshiNo ratings yet

- Fish Food SufficiencyDocument30 pagesFish Food SufficiencyDonaldDeLeonNo ratings yet

- Urbanism Si Mobila UrbanaDocument148 pagesUrbanism Si Mobila UrbanaLaura FinkelsteinNo ratings yet

- 170 - Help Points List PDFDocument6 pages170 - Help Points List PDFRaju PuttaswamyNo ratings yet

- Request For Taxpayer Identification Number and CertificationDocument8 pagesRequest For Taxpayer Identification Number and Certificationxintong liuNo ratings yet

- P2WORKDocument2 pagesP2WORKkhefnerNo ratings yet

- Dynamic BalancingDocument2 pagesDynamic BalancingChetan PrajapatiNo ratings yet

- Mental Health Nursing R ShreevaniDocument3 pagesMental Health Nursing R ShreevaniBalwant SinghNo ratings yet

- CH 6 Reverse Logistics PresentationDocument27 pagesCH 6 Reverse Logistics PresentationSiddhesh KolgaonkarNo ratings yet

- Lee Metcalf: The Homestead Act of 1862 National Wildlife RefugeDocument2 pagesLee Metcalf: The Homestead Act of 1862 National Wildlife RefugeChristian ComunityNo ratings yet

- Sectoral Snippets: India Industry InformationDocument18 pagesSectoral Snippets: India Industry Informationpg10shivi_gNo ratings yet

- CVP Considerations in Choosing Between High Fixed or Variable Cost StructuresDocument3 pagesCVP Considerations in Choosing Between High Fixed or Variable Cost StructuresJonna LynneNo ratings yet

- Brannigan Foods: Strategic Marketing PlanningDocument13 pagesBrannigan Foods: Strategic Marketing PlanningNand BhushanNo ratings yet

- User Guide Clearing Messages SWIFT ISO 15022: MT54x Version 1.6 (Release 2008)Document96 pagesUser Guide Clearing Messages SWIFT ISO 15022: MT54x Version 1.6 (Release 2008)Gordana PavlovaNo ratings yet

- DocxDocument2 pagesDocxWalt Chea100% (6)

- Debt Dispute LetterDocument2 pagesDebt Dispute LetterBenson ZhangNo ratings yet

- Travel PDFDocument1 pageTravel PDFtaliajanelleNo ratings yet

- Apparel Industry of Sri LankaDocument4 pagesApparel Industry of Sri LankaRanjan NishanthaNo ratings yet

- Stigler - Theory of Econ RegulationDocument20 pagesStigler - Theory of Econ Regulationheh92No ratings yet

- Industrialisation As A Process of Social Change in IndiaDocument4 pagesIndustrialisation As A Process of Social Change in IndiaBiren PachalNo ratings yet

- Board Resolution of Peace Riders Club Pascam II General Trias ChapterDocument2 pagesBoard Resolution of Peace Riders Club Pascam II General Trias ChapterCM Ronald Bautista100% (2)

- Nooyi Economic Club of Washington 51209Document34 pagesNooyi Economic Club of Washington 51209Prateek UpadhyayNo ratings yet

- TEF 1000 NAMES 2019 TEF Partners 1 .01Document7 pagesTEF 1000 NAMES 2019 TEF Partners 1 .01KAMPAMBA LUKWESANo ratings yet

- Strategic Management Project On Tata SteelDocument18 pagesStrategic Management Project On Tata SteelRonak GosaliaNo ratings yet

- PEST Example Analysis TemplateDocument1 pagePEST Example Analysis TemplateKarim AbdelazeemNo ratings yet

- Analysis of Vehicle Operating Costs (VOC) and Travel Time SavingsDocument10 pagesAnalysis of Vehicle Operating Costs (VOC) and Travel Time Savingsyitno507No ratings yet

- Research On AgingDocument5 pagesResearch On AgingAslam RehmanNo ratings yet