You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Adamson University Managerial Accounting 1 Summary of Ratios (Additional) Ratio Formula RelevanceDocument1 pageAdamson University Managerial Accounting 1 Summary of Ratios (Additional) Ratio Formula Relevancefeitheart_rukaNo ratings yet

- Analysis of Financial Statements: Answers To Selected End-Of-Chapter QuestionsDocument9 pagesAnalysis of Financial Statements: Answers To Selected End-Of-Chapter Questionsfeitheart_rukaNo ratings yet

- Hash SlingingDocument1 pageHash Slingingfeitheart_rukaNo ratings yet

- Tech Eng Pampahirap NG Buhay Version .001Document1 pageTech Eng Pampahirap NG Buhay Version .001feitheart_rukaNo ratings yet

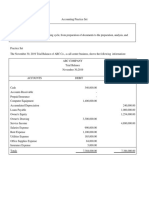

- Project ProposalDocument3 pagesProject Proposalfeitheart_ruka100% (1)

- Grade 9Document2 pagesGrade 9feitheart_rukaNo ratings yet

- Reminders in Preparing Bank Reconciliation StatementDocument2 pagesReminders in Preparing Bank Reconciliation Statementfeitheart_rukaNo ratings yet

- Manga Doki DokiDocument1 pageManga Doki Dokifeitheart_rukaNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Solution Manual Business EntitiesDocument34 pagesSolution Manual Business EntitiesKiranNo ratings yet

- Financial Statements ExercicesDocument7 pagesFinancial Statements Exercicesluliga.loulouNo ratings yet

- Acc-Sample Paper-04Document8 pagesAcc-Sample Paper-04guneet uberoiNo ratings yet

- Intangible AssetsDocument22 pagesIntangible AssetsKaye Choraine Naduma100% (1)

- Working Capital Management: TATA SteelDocument17 pagesWorking Capital Management: TATA SteelSaurabh KhandelwalNo ratings yet

- The Enron Scandal - AssignmentDocument12 pagesThe Enron Scandal - AssignmentArasen அரசன் பழனியாண்டி100% (1)

- I-Great Mega: ArketingDocument12 pagesI-Great Mega: ArketingApakElBuheiriGetbNo ratings yet

- Philippine Bonded Warehouse Services, Inc. Application For Accreditation To CCBW 1415Document3 pagesPhilippine Bonded Warehouse Services, Inc. Application For Accreditation To CCBW 1415Itsfreynk05No ratings yet

- Mutual Fund Industry Decade of Growth 2010 2020 ReportDocument36 pagesMutual Fund Industry Decade of Growth 2010 2020 ReportHarshit SinghNo ratings yet

- Test Bank For Analysis For Financial Management 10th Edition by Higgins PDFDocument18 pagesTest Bank For Analysis For Financial Management 10th Edition by Higgins PDFRandyNo ratings yet

- MCQ-Delta HedgingDocument2 pagesMCQ-Delta HedgingkeshavNo ratings yet

- Ex. 013 Guj Ordinance No.8 of 2020 Dt.21-08-2020 PDFDocument26 pagesEx. 013 Guj Ordinance No.8 of 2020 Dt.21-08-2020 PDFAshish Majithia100% (1)

- Accounting MCQs With AnswersDocument77 pagesAccounting MCQs With AnswersAbhijeet AnandNo ratings yet

- TB12Document9 pagesTB12afrgod20No ratings yet

- ABC CompanyDocument11 pagesABC CompanyA DiolataNo ratings yet

- Institute and Faculty of Actuaries: Subject CT1 - Financial Mathematics Core TechnicalDocument7 pagesInstitute and Faculty of Actuaries: Subject CT1 - Financial Mathematics Core TechnicalfeererereNo ratings yet

- Common Errors in DCF ModelsDocument12 pagesCommon Errors in DCF Modelsrslamba1100% (2)

- Pubali July - 2019 - FinalDocument66 pagesPubali July - 2019 - Finalzannatul zoyaNo ratings yet

- Topic 7 - Forecasting Financial Statements (Updated)Document64 pagesTopic 7 - Forecasting Financial Statements (Updated)Jasmine JacksonNo ratings yet

- October 2020: Canada Core Pick ListDocument3 pagesOctober 2020: Canada Core Pick ListblacksmithMGNo ratings yet

- CHAP - 01 - An Overview of Banking SectorDocument39 pagesCHAP - 01 - An Overview of Banking SectorDieu NguyenNo ratings yet

- Financial Rehabilitation and Insolvency Act - Test BankDocument6 pagesFinancial Rehabilitation and Insolvency Act - Test BankHads LunaNo ratings yet

- Duration and Bonds - 27 Pages of Q & ANSDocument27 pagesDuration and Bonds - 27 Pages of Q & ANSAbdulaziz FaisalNo ratings yet

- Member LedgersDocument205 pagesMember LedgersDhruv ChandwaniNo ratings yet

- Financial Management 2 Assignment 1: Dividend Policy at FPL GroupDocument9 pagesFinancial Management 2 Assignment 1: Dividend Policy at FPL GroupDiv_nNo ratings yet

- Red Herring ProspectusDocument414 pagesRed Herring ProspectusTejesh GoudNo ratings yet

- Deloitte-FAS Corporate Finance BrochureDocument12 pagesDeloitte-FAS Corporate Finance BrochureKen TO100% (1)

- HDFC Balanced Advantage Fund - Apr 22 - 1 PDFDocument2 pagesHDFC Balanced Advantage Fund - Apr 22 - 1 PDFAkash BNo ratings yet

- MakalahDocument8 pagesMakalahAsyam ArkaNo ratings yet

- Business Finance-Module 1Document15 pagesBusiness Finance-Module 1Alex PrioloNo ratings yet