You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Key terms in strategic planningDocument17 pagesKey terms in strategic planningDhez BolutanoNo ratings yet

- ICICIDirect SymbolsDocument49 pagesICICIDirect SymbolsKrishnamoorthy SubramaniamNo ratings yet

- Study of Marketing Mix of Maruti Suzuki - BBA Marketing Summer Training Project Report PDFDocument95 pagesStudy of Marketing Mix of Maruti Suzuki - BBA Marketing Summer Training Project Report PDFRj Bîmålkümãr75% (4)

- 73ac4horizontal & Vertical IntegrationDocument5 pages73ac4horizontal & Vertical IntegrationOjasvee KhannaNo ratings yet

- Prop-Wills DigestDocument5 pagesProp-Wills DigestJenica Ti100% (1)

- Georgia v. Tennessee Copper Co. Limits Noxious Fumes Across State LinesDocument13 pagesGeorgia v. Tennessee Copper Co. Limits Noxious Fumes Across State LinesJenica TiNo ratings yet

- Notarial Practice (Rules)Document6 pagesNotarial Practice (Rules)Jenica TiNo ratings yet

- Darvin Crim Pro DiagramDocument1 pageDarvin Crim Pro DiagramJenica TiNo ratings yet

- Transboundary Pollution (NOTES)Document6 pagesTransboundary Pollution (NOTES)Jenica TiNo ratings yet

- Election Law NotesDocument20 pagesElection Law NotesJenica Ti100% (1)

- Corporation Code Refresher pt1Document11 pagesCorporation Code Refresher pt1Jenica TiNo ratings yet

- Chapter One: Preliminary Considerations I. Basic ConceptsDocument5 pagesChapter One: Preliminary Considerations I. Basic ConceptsJenica TiNo ratings yet

- Time Program (For 80 Pax) MarshalsDocument4 pagesTime Program (For 80 Pax) MarshalsJenica TiNo ratings yet

- Project Report GTM PepsiDocument12 pagesProject Report GTM PepsiSudhanshu NangruNo ratings yet

- Function List of Car BrainDocument39 pagesFunction List of Car BrainBogdan PopNo ratings yet

- CIR Vs MarubeniDocument2 pagesCIR Vs MarubeniJocelyn MagbanuaNo ratings yet

- Subic Bay Trading Company ProfileDocument4 pagesSubic Bay Trading Company ProfileNaomi Gimenez BisnarNo ratings yet

- Vks Projects LTDDocument263 pagesVks Projects LTDAswathy NairNo ratings yet

- RRB Exam Previous Year ModelDocument3 pagesRRB Exam Previous Year ModelShijumon XavierNo ratings yet

- Invoice-Apollo - Chennai - ApplicatorDocument1 pageInvoice-Apollo - Chennai - ApplicatorSan SandeepNo ratings yet

- DLFDocument17 pagesDLFAMAL BABUNo ratings yet

- BSN Micro/i Application FormDocument5 pagesBSN Micro/i Application FormVivo Vuvo17% (6)

- 2019A QE Strategic Cost Management FinalDocument5 pages2019A QE Strategic Cost Management FinalJam Crausus100% (1)

- Airbus 40 Years of Innovation - Timeline IllustratedDocument4 pagesAirbus 40 Years of Innovation - Timeline IllustratedOmar BeglerovicNo ratings yet

- Advance Accounting Prelim BSATDocument8 pagesAdvance Accounting Prelim BSATLenie Lyn Pasion TorresNo ratings yet

- Emirate SDDocument11 pagesEmirate SDWan SajaNo ratings yet

- JAK MEMBERS BANK HISTORY AND SERVICESDocument45 pagesJAK MEMBERS BANK HISTORY AND SERVICESHanief AdrianNo ratings yet

- Inversiones de VanguardDocument5 pagesInversiones de VanguardEugenio HerreraNo ratings yet

- Business Directories 2017Document8 pagesBusiness Directories 2017Amjad ShareefNo ratings yet

- Intermediate Accounting I IntroductionDocument6 pagesIntermediate Accounting I IntroductionJoovs JoovhoNo ratings yet

- Orgs ExistDocument15 pagesOrgs ExistFiroz AminNo ratings yet

- Audit Committees ChecklistDocument8 pagesAudit Committees ChecklistTarryn Jacinth NaickerNo ratings yet

- Brand ExtensionDocument28 pagesBrand ExtensionsureshkachhawaNo ratings yet

- MTBC VS JMCDocument4 pagesMTBC VS JMCRichelle CartinNo ratings yet

- 21032019172516Document3 pages21032019172516Azharul IslamNo ratings yet

- Sapsuccessfactors Coursecontent V5Document43 pagesSapsuccessfactors Coursecontent V5deepsajjan0% (1)

- Ias 37Document8 pagesIas 37Szetoo WeishyaNo ratings yet

- Fundamental and Technical Analysis - Technical PaperDocument16 pagesFundamental and Technical Analysis - Technical PaperGauree AravkarNo ratings yet

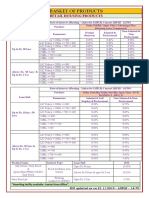

- BASKET OF RETAIL PRODUCTS RATESDocument3 pagesBASKET OF RETAIL PRODUCTS RATESVirendra K VermaNo ratings yet