You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Caroline Lang: Criminal Justice/Crime Scene Investigator StudentDocument9 pagesCaroline Lang: Criminal Justice/Crime Scene Investigator Studentapi-405159987No ratings yet

- United States v. Theresa Mubang, 4th Cir. (2013)Document3 pagesUnited States v. Theresa Mubang, 4th Cir. (2013)Scribd Government DocsNo ratings yet

- Code of Conduct For Court PersonnelDocument6 pagesCode of Conduct For Court PersonnelJenelyn Bacay LegaspiNo ratings yet

- Heirs of Castillo Vs Lacuata-GabrielDocument2 pagesHeirs of Castillo Vs Lacuata-GabrielJo BudzNo ratings yet

- Sec 3 CompilationDocument6 pagesSec 3 CompilationMatthew WittNo ratings yet

- 2 Sebastian vs. Morales, 445 Phil. 595Document2 pages2 Sebastian vs. Morales, 445 Phil. 595loschudentNo ratings yet

- NYC B14 FEMA - Ted Monette FDR - Draft Interview QuestionsDocument3 pagesNYC B14 FEMA - Ted Monette FDR - Draft Interview Questions9/11 Document ArchiveNo ratings yet

- Certificate of Candidacy SGODocument2 pagesCertificate of Candidacy SGObernardNo ratings yet

- Firearms Protection Act (Review Of)Document63 pagesFirearms Protection Act (Review Of)ArchdukePotterNo ratings yet

- Red Tape Report: Behind The Scenes of The Section 8 Housing ProgramDocument7 pagesRed Tape Report: Behind The Scenes of The Section 8 Housing ProgramBill de BlasioNo ratings yet

- RUBI v. Provincial BoardDocument3 pagesRUBI v. Provincial BoardMaila Fortich RosalNo ratings yet

- Asia Trust Devt Bank v. First Aikka Development, Inc. and Univac Development, IncDocument28 pagesAsia Trust Devt Bank v. First Aikka Development, Inc. and Univac Development, IncSiobhan RobinNo ratings yet

- Amanquiton v. PeopleDocument4 pagesAmanquiton v. PeopleKeel Achernar DinoyNo ratings yet

- The Lex Rei Sitae RulesDocument4 pagesThe Lex Rei Sitae RulesApple WormNo ratings yet

- Press Note For General Election To Karnataka-FinalDocument46 pagesPress Note For General Election To Karnataka-FinalRAKSHITH RNo ratings yet

- Crime and Punishment Around The World Volume 1 Africa and The Middle East PDFDocument468 pagesCrime and Punishment Around The World Volume 1 Africa and The Middle East PDFAnnethedinosaurNo ratings yet

- Ministry of Civil Aviation Security RulesDocument13 pagesMinistry of Civil Aviation Security RulesshombisNo ratings yet

- RISE OF ISIS THREATDocument7 pagesRISE OF ISIS THREATJoyce Manalo100% (3)

- Workings of Debt Recovery TribunalsDocument25 pagesWorkings of Debt Recovery TribunalsSujal ShahNo ratings yet

- SC rules carrier liable for damages in sinking caseDocument1 pageSC rules carrier liable for damages in sinking caseKimberly RamosNo ratings yet

- Impact of Company, Contract, Competition & Data Protection Law on Business (40/40Document3 pagesImpact of Company, Contract, Competition & Data Protection Law on Business (40/40GasluNo ratings yet

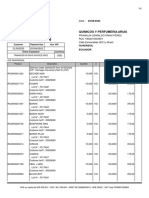

- Factura ComercialDocument6 pagesFactura ComercialKaren MezaNo ratings yet

- Taxation: General PrinciplesDocument34 pagesTaxation: General PrinciplesKeziah A GicainNo ratings yet

- Caridad Ongsiako, Et. Al Vs Emilia Ongsiako, Et. Al (GR. No. 7510, 30 March 1957, 101 Phil 1196-1197)Document1 pageCaridad Ongsiako, Et. Al Vs Emilia Ongsiako, Et. Al (GR. No. 7510, 30 March 1957, 101 Phil 1196-1197)Archibald Jose Tiago ManansalaNo ratings yet

- Sponsor Change: Three Upline Approval FormDocument1 pageSponsor Change: Three Upline Approval FormClaudiamar CristisorNo ratings yet

- Introduction To Philippine Criminal Justice SystemDocument68 pagesIntroduction To Philippine Criminal Justice SystemLouvieBuhayNo ratings yet

- Territorial SeaDocument3 pagesTerritorial SeatonyNo ratings yet

- Dizon V CTA DigestDocument2 pagesDizon V CTA DigestNicholas FoxNo ratings yet

- JG Summit Holdings Vs CA September 24, 2003 PDFDocument2 pagesJG Summit Holdings Vs CA September 24, 2003 PDFErvin Franz Mayor CuevillasNo ratings yet

- Pbcom V CirDocument1 pagePbcom V Cirana ortizNo ratings yet