You might also like

- Revenue Circular Amends Real Property Transfer RequirementsDocument1 pageRevenue Circular Amends Real Property Transfer RequirementsReymund BumanglagNo ratings yet

- Revenue Circular on Tax Treatment of Income Payments to Individuals Hired Under Contract of ServiceDocument7 pagesRevenue Circular on Tax Treatment of Income Payments to Individuals Hired Under Contract of ServiceEJ PajaroNo ratings yet

- RMC No. 135-2019Document4 pagesRMC No. 135-2019Jeffrey Dela Rosa BautistaNo ratings yet

- F, A& %-,ffi'lk) : Lli'//'l'lDocument3 pagesF, A& %-,ffi'lk) : Lli'//'l'lMobile LegendsNo ratings yet

- Tax Incentives Transparency Act of 2015 summaryDocument6 pagesTax Incentives Transparency Act of 2015 summaryAnna Leigh AnilloNo ratings yet

- DILG Legal Opinions Development PermitDocument4 pagesDILG Legal Opinions Development PermitattyjeckyNo ratings yet

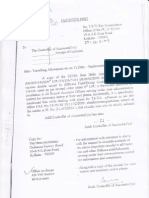

- #.Ciq Of: Revenue The CollectionDocument6 pages#.Ciq Of: Revenue The CollectionCliff DaquioagNo ratings yet

- Construction & Design Services Contractor ListDocument38 pagesConstruction & Design Services Contractor ListSaurabh DwivediNo ratings yet

- Ord01 09Document4 pagesOrd01 09seoversightNo ratings yet

- i.1e, J:J#, - Jri-I: ,?li:,il IilffiDocument5 pagesi.1e, J:J#, - Jri-I: ,?li:,il IilffiadhityaNo ratings yet

- LTFRB Memo # 2014-008Document3 pagesLTFRB Memo # 2014-008PortCallsNo ratings yet

- RMC No. 141-2019 Reiterating The Salient Points Arising From RMC No. 14-16 On The Proper Execution of Waivers PDFDocument2 pagesRMC No. 141-2019 Reiterating The Salient Points Arising From RMC No. 14-16 On The Proper Execution of Waivers PDFKriszan ManiponNo ratings yet

- RMC No. 141-2019 Reiterating The Salient Points Arising From RMC No. 14-16 On The Proper Execution of Waivers PDFDocument2 pagesRMC No. 141-2019 Reiterating The Salient Points Arising From RMC No. 14-16 On The Proper Execution of Waivers PDFKriszan ManiponNo ratings yet

- CAG Circular On MT 05e61ddc6cc64e4 27692120 - 230526 - 110607Document3 pagesCAG Circular On MT 05e61ddc6cc64e4 27692120 - 230526 - 110607Kartik SharmaNo ratings yet

- BIR: RMO No. 26-2016Document5 pagesBIR: RMO No. 26-2016John DavidNo ratings yet

- Certificate Incorporation: TIN OFDocument32 pagesCertificate Incorporation: TIN OFSam Lago100% (1)

- Sample CertificateDocument32 pagesSample CertificateVic AlvarezNo ratings yet

- Update Revenue RecordsDocument6 pagesUpdate Revenue Recordssivagangai kisasNo ratings yet

- Ffi-'#Ff Ffifr Ffirffii I (Y Tu 6 ( R / D," : ' /Anj//T4A-E (Nt/E% & - TR Cs. 'RNDocument7 pagesFfi-'#Ff Ffifr Ffirffii I (Y Tu 6 ( R / D," : ' /Anj//T4A-E (Nt/E% & - TR Cs. 'RNKAMALKISHNo ratings yet

- DILG-Legal - Opinions-201133 - Accountants AdviceDocument4 pagesDILG-Legal - Opinions-201133 - Accountants AdviceJoel Mangubat AmanteNo ratings yet

- Dar Manual On Legal AssistanceDocument12 pagesDar Manual On Legal Assistancehabeas_corpuzNo ratings yet

- India Sudar TaxFile 2005-06Document7 pagesIndia Sudar TaxFile 2005-06India Sudar Educational and Charitable Trust100% (1)

- Doeunpnt Explaiation Afiudavit/Suppieniqnt !uequired DocumentsDocument9 pagesDoeunpnt Explaiation Afiudavit/Suppieniqnt !uequired DocumentsChapter 11 DocketsNo ratings yet

- RMC No 89-2017Document3 pagesRMC No 89-2017Mark Lord Morales BumagatNo ratings yet

- 10 FLR (I: (L!FR, B+CR QRXRDocument2 pages10 FLR (I: (L!FR, B+CR QRXRRajkumar RajputNo ratings yet

- Report on Proposed Reforms to the System of Way Bills in Andhra PradeshDocument22 pagesReport on Proposed Reforms to the System of Way Bills in Andhra PradeshNitin K. ParekhNo ratings yet

- New Stock Transfer Tax Rate Under TRAIN LawDocument2 pagesNew Stock Transfer Tax Rate Under TRAIN LawRomer LesondatoNo ratings yet

- I. Far-Reaching Implications of The Legal Issue Justify Treatment of Petition For Declaratory Relief As One For MandamusDocument33 pagesI. Far-Reaching Implications of The Legal Issue Justify Treatment of Petition For Declaratory Relief As One For MandamusGuillermo Olivo IIINo ratings yet

- National Transmission Corporation Concession Agreement SummaryDocument80 pagesNational Transmission Corporation Concession Agreement Summaryjerikaye law100% (1)

- The Record-Of-Rights: MutationDocument45 pagesThe Record-Of-Rights: MutationAnonymous lfw4mfCmNo ratings yet

- AP VAT RULES SUMMARYDocument92 pagesAP VAT RULES SUMMARYLe Bharath RoiNo ratings yet

- Government AccountingDocument6 pagesGovernment AccountingroliNo ratings yet

- Procurementof Works StandardTenderDocumentRevisionDocument2 pagesProcurementof Works StandardTenderDocumentRevisionEXECUTIVE ENGINEER RamanagaraNo ratings yet

- SC Rules PR1 Not Liable for Real Property TaxesDocument15 pagesSC Rules PR1 Not Liable for Real Property TaxesJose IbarraNo ratings yet

- RMO No 17-2017Document2 pagesRMO No 17-2017fatmaaleahNo ratings yet

- Rajasthan Victim Compensation Scheme 2011Document6 pagesRajasthan Victim Compensation Scheme 2011Latest Laws TeamNo ratings yet

- Asetts 2Document43 pagesAsetts 2librarypublisherNo ratings yet

- Fiul : "R/'LV, Yl:LllippiDocument4 pagesFiul : "R/'LV, Yl:LllippiLaurenz DalanginNo ratings yet

- Remittance Guidelines 2020 GadgetDocument15 pagesRemittance Guidelines 2020 Gadgetmd mehmoodNo ratings yet

- RMC 75-2018 Prescribes The Mandatory Statutory Requirement and Function of A Letter of AuthorityDocument2 pagesRMC 75-2018 Prescribes The Mandatory Statutory Requirement and Function of A Letter of AuthorityMiming BudoyNo ratings yet

- States: Court " of For AllDocument2 pagesStates: Court " of For AllMau Z MacDayNo ratings yet

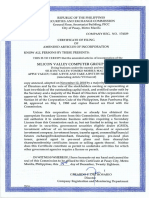

- SEC Amended Articles of Incorporation for Silicon Valley Computer GroupDocument20 pagesSEC Amended Articles of Incorporation for Silicon Valley Computer GroupSir AronNo ratings yet

- DM No. 108, S. 2023. Revised Checklist of Documentary Requirements FormDocument12 pagesDM No. 108, S. 2023. Revised Checklist of Documentary Requirements Formbryan.berinoNo ratings yet

- FOI Manual 2017Document20 pagesFOI Manual 2017Clea LagcoNo ratings yet

- RR No 21-2018Document3 pagesRR No 21-2018Larry Tobias Jr.No ratings yet

- RMC No 24 2015 QA Scanned Copies of Forms 2307 and 2316 PDFDocument4 pagesRMC No 24 2015 QA Scanned Copies of Forms 2307 and 2316 PDFRalph ZelaNo ratings yet

- Standalone Financial Results, Limited Review Report For September 30, 2016 (Result)Document5 pagesStandalone Financial Results, Limited Review Report For September 30, 2016 (Result)Shyam SunderNo ratings yet

- Contract HtechcorpDocument3 pagesContract Htechcorpherkimer.lightNo ratings yet

- RR No. 8 2016Document4 pagesRR No. 8 2016Jay Mark ReponteNo ratings yet

- SAMPLE of AmedmentsDocument22 pagesSAMPLE of AmedmentsMae De GuzmanNo ratings yet

- Vitthal Mandir Audit ReportDocument4 pagesVitthal Mandir Audit ReportHindu Janajagruti SamitiNo ratings yet

- 5gBJECT:: Regulations BIR ofDocument6 pages5gBJECT:: Regulations BIR ofErica CaliuagNo ratings yet

- Krntoor Va) T Dte Prokureur-Generaal: Attorney:G L (Itwatersrands e Plaaslike Afd Eiling Vitwatersrand Local Office ofDocument2 pagesKrntoor Va) T Dte Prokureur-Generaal: Attorney:G L (Itwatersrands e Plaaslike Afd Eiling Vitwatersrand Local Office ofPitchfork NewsNo ratings yet

- RMC No 42-2019Document3 pagesRMC No 42-2019Aj PacaldoNo ratings yet

- RMC No 19-2018Document2 pagesRMC No 19-2018Paul GeorgeNo ratings yet

- Prescribing Policies for Accounting of Offsetting TransactionsDocument6 pagesPrescribing Policies for Accounting of Offsetting TransactionssandraNo ratings yet

- Immovable and Movable Property 1Document12 pagesImmovable and Movable Property 1Jaminder BibraNo ratings yet

- In Of: Subject To of of Any TheDocument3 pagesIn Of: Subject To of of Any TheBok CoolNo ratings yet

- Where Is The $70 Million Dollars That's Missing From DeKalb County Watershed Department?Document12 pagesWhere Is The $70 Million Dollars That's Missing From DeKalb County Watershed Department?Viola DavisNo ratings yet

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- Philippine Stock Exchange: Head, Disclosure DepartmentDocument15 pagesPhilippine Stock Exchange: Head, Disclosure DepartmentKarl Anthony Rigoroso MargateNo ratings yet

- Disclosure No. 851 2020 List of Stockholders As of March 17 2020Document245 pagesDisclosure No. 851 2020 List of Stockholders As of March 17 2020Karl Anthony Rigoroso MargateNo ratings yet

- Of Public: Notice HearingDocument2 pagesOf Public: Notice HearingKarl Anthony Rigoroso MargateNo ratings yet

- ADMU PRIVACY POLICY For Students, Admission Applicants and Alumni (April 2018)Document4 pagesADMU PRIVACY POLICY For Students, Admission Applicants and Alumni (April 2018)Karl Anthony Rigoroso MargateNo ratings yet

- Checklist For Infrastructure 2017Document2 pagesChecklist For Infrastructure 2017Marciano Apilado100% (1)

- Health Privacy CodeDocument46 pagesHealth Privacy CodePhilip TomzNo ratings yet

- TIMTADocument6 pagesTIMTAKarl Anthony Rigoroso MargateNo ratings yet

- BAC-NSCC GeoTech RFPDocument24 pagesBAC-NSCC GeoTech RFPKarl Anthony Rigoroso MargateNo ratings yet

- 1 PDFDocument50 pages1 PDFBenjie Modelo ManilaNo ratings yet

- PDF PDFDocument700 pagesPDF PDFRin ChesterNo ratings yet

- 2118 EA GuidelinesDocument1 page2118 EA GuidelinesMark RamirezNo ratings yet

- Ersonal ATA Heet: JBC Form No. 1Document7 pagesErsonal ATA Heet: JBC Form No. 1Karl Anthony Rigoroso MargateNo ratings yet

- Rules of CourtDocument233 pagesRules of CourtKarl Anthony Rigoroso MargateNo ratings yet

- Pos 11172014Document2 pagesPos 11172014Karl Anthony Rigoroso MargateNo ratings yet

- RR No. 6-2019 - IRR Estate Tax AmnestyDocument5 pagesRR No. 6-2019 - IRR Estate Tax AmnestyAlexander Julio ValeraNo ratings yet

- Ra 6541Document77 pagesRa 6541b_nicebNo ratings yet

- NLRC RulesDocument19 pagesNLRC RulesKarl Anthony Rigoroso MargateNo ratings yet

- Bail Bond Guide PhilippinesDocument100 pagesBail Bond Guide PhilippinesSakuraCardCaptor60% (5)

- W16 ADMS 4562 Assignment 2Document6 pagesW16 ADMS 4562 Assignment 2vyaskush100% (1)

- Table 1 - Tax Table 01Document182 pagesTable 1 - Tax Table 01wellawalalasithNo ratings yet

- Employee Pay StubDocument2 pagesEmployee Pay StubTasnim jamil100% (1)

- Solution Aassignments CH 13Document2 pagesSolution Aassignments CH 13RuturajPatilNo ratings yet

- QUOTEDocument1 pageQUOTESagar ButaniNo ratings yet

- Generate LESCO electricity billDocument2 pagesGenerate LESCO electricity billusmanNo ratings yet

- Crew time card tracking hoursDocument1 pageCrew time card tracking hoursValeria GonzálezNo ratings yet

- Greek Debt Crisis: How It StartedDocument3 pagesGreek Debt Crisis: How It StartedHidden TalentzNo ratings yet

- Income Tax Payment Challan: PSID #: 41614961Document1 pageIncome Tax Payment Challan: PSID #: 41614961Zubair KhanNo ratings yet

- Tax Invoice and Tax Credit NoteDocument24 pagesTax Invoice and Tax Credit NoteMichu ParadNo ratings yet

- State Tax Return NC-F14Document2 pagesState Tax Return NC-F14aklank_218105No ratings yet

- Group Assignment - April 23Document16 pagesGroup Assignment - April 23DIVA RTHININo ratings yet

- Taxmann - Budget Highlights 2022-2023Document42 pagesTaxmann - Budget Highlights 2022-2023Jinang JainNo ratings yet

- Panaji, 11th January, 2018 (Pausa 21, 1939) : Government of GoaDocument28 pagesPanaji, 11th January, 2018 (Pausa 21, 1939) : Government of Goaks1962No ratings yet

- 2307 TemplateDocument4 pages2307 TemplateMarianneRoseBrusolaNo ratings yet

- FNSTPB412 AE Sk2of4 Appx FrasersElectricalEmployeeDataDocument34 pagesFNSTPB412 AE Sk2of4 Appx FrasersElectricalEmployeeDataChoo Li ZiNo ratings yet

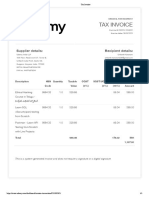

- Udhemy CourcesDocument1 pageUdhemy CourcesRam Sri100% (1)

- Gross Estate Tax QuizzerDocument6 pagesGross Estate Tax QuizzerLloyd Sonica100% (1)

- Amaron Battery Change InvoiceDocument2 pagesAmaron Battery Change InvoiceShivam MishraNo ratings yet

- BIR Ruling 27-02Document2 pagesBIR Ruling 27-02erikagcv100% (1)

- Teaching PowerPoint Slides - Chapter 13Document20 pagesTeaching PowerPoint Slides - Chapter 13Seo ChangBinNo ratings yet

- CIR V General FoodsDocument2 pagesCIR V General FoodsNelsonPolinarLaurdenNo ratings yet

- Bahasa Inggris PPHDocument9 pagesBahasa Inggris PPHRiska UsmawardaniNo ratings yet

- Quotation For Scrap & E Waste-Orica1Document2 pagesQuotation For Scrap & E Waste-Orica1Rakesh Singh100% (3)

- 2020 Income Tax Organizer: 211 Crescent DriveDocument2 pages2020 Income Tax Organizer: 211 Crescent DriveLeslie HutchinsonNo ratings yet

- 7th NFC Award 2010Document4 pages7th NFC Award 2010humayun313No ratings yet

- FM Specialization 2nd Year Book ListDocument3 pagesFM Specialization 2nd Year Book Listloveprashant82No ratings yet

- PRD Requirements Checklist For Non Trade Supplier Accreditation 2011 1Document1 pagePRD Requirements Checklist For Non Trade Supplier Accreditation 2011 1LouAnn Templo Cabrera100% (1)

- 2 5 296 180Document4 pages2 5 296 180Mayur PatilNo ratings yet

- Computation of Total Income Income From Salary (Chapter IV A) 260000Document1 pageComputation of Total Income Income From Salary (Chapter IV A) 260000jassi7nishadNo ratings yet