You might also like

- 1201 Cash QuestionsDocument12 pages1201 Cash QuestionsAngel Mae YapNo ratings yet

- IA1 - 1st Mock Quiz (With Suggested Answers)Document6 pagesIA1 - 1st Mock Quiz (With Suggested Answers)Rogienel ReyesNo ratings yet

- Ia 1 - Prelim ExamDocument8 pagesIa 1 - Prelim ExamYnah GarciaNo ratings yet

- Problem Solving (With Answers)Document12 pagesProblem Solving (With Answers)sunflower100% (1)

- Assessment Test 2nd Cash&RecDocument6 pagesAssessment Test 2nd Cash&RecMellowNo ratings yet

- 01 - TFAR2301 - Cash and Cash Equivalents - January 16 (With Answers)Document4 pages01 - TFAR2301 - Cash and Cash Equivalents - January 16 (With Answers)Bea GarciaNo ratings yet

- A. TheoryDocument10 pagesA. TheoryROMULO CUBID100% (1)

- Cash and Cash EqDocument18 pagesCash and Cash EqElaine YapNo ratings yet

- Cash and Cash Equivalents, Bank Reconciliation, and Proof of CashDocument8 pagesCash and Cash Equivalents, Bank Reconciliation, and Proof of CashMichaelNo ratings yet

- Pq-Cash and Cash EquivalentsDocument3 pagesPq-Cash and Cash EquivalentsJanella PatriziaNo ratings yet

- Quiz On Audit of CashDocument11 pagesQuiz On Audit of CashY JNo ratings yet

- 1st Long Exam (Summer 2022) WITHOUT ANSWERDocument10 pages1st Long Exam (Summer 2022) WITHOUT ANSWERDaphnie Kitch CatotalNo ratings yet

- Bank Reconciliation and Cash Accounts QuizDocument3 pagesBank Reconciliation and Cash Accounts QuizMarizMatampaleNo ratings yet

- ACCTG102 MidtermQ1.5 Cash Make Up ExamDocument6 pagesACCTG102 MidtermQ1.5 Cash Make Up ExamBarrylou Manayan100% (1)

- Cash and Cash Equivalents ControlsDocument48 pagesCash and Cash Equivalents ControlsLorraine Mae Robrido100% (1)

- Quiz 2 Cash To ARDocument4 pagesQuiz 2 Cash To ARGraziela MercadoNo ratings yet

- Finacc Quiz 1Document8 pagesFinacc Quiz 1Jonas Mondala100% (1)

- Deptals 2Document6 pagesDeptals 2jenylyn acostaNo ratings yet

- APC 4 Reviewer Before FinalsDocument38 pagesAPC 4 Reviewer Before Finalsjeremy groundNo ratings yet

- 03 Quiz On Topic 03 Theories and FAR Problems With Answer KeyDocument4 pages03 Quiz On Topic 03 Theories and FAR Problems With Answer KeyNye NyeNo ratings yet

- FINANCIAL ACCOUNTING 1 CASH AND CASH EQUIVALENTSDocument9 pagesFINANCIAL ACCOUNTING 1 CASH AND CASH EQUIVALENTSPau Santos76% (29)

- (Cash and Cash Equivalents Drills) Acc.106Document18 pages(Cash and Cash Equivalents Drills) Acc.106Boys ShipperNo ratings yet

- Theories - Cash & Cash Equivalents: Identify The Choice That Best Completes The Statement or Answers The QuestionDocument15 pagesTheories - Cash & Cash Equivalents: Identify The Choice That Best Completes The Statement or Answers The QuestionRyan PatitoNo ratings yet

- Cash and Cash Equivalents (Continuation)Document7 pagesCash and Cash Equivalents (Continuation)rufamaegarcia07No ratings yet

- Acctg 100C 01Document6 pagesAcctg 100C 01Jose Magallanes100% (1)

- Q1 SMEsDocument6 pagesQ1 SMEsJennifer RasonabeNo ratings yet

- AP - Audit of CashDocument4 pagesAP - Audit of CashRose CastilloNo ratings yet

- ProbsDocument27 pagesProbsDante Jr. Dela Cruz50% (2)

- TOA 01 CASH AND CASH EQUIVALENTS W SOL PDFDocument5 pagesTOA 01 CASH AND CASH EQUIVALENTS W SOL PDFJerelyn DaneNo ratings yet

- BA 114.1 - Quiz 1 SamplexDocument12 pagesBA 114.1 - Quiz 1 SamplexPamela May NavarreteNo ratings yet

- ACCTG102 MidtermQ1 CashDocument13 pagesACCTG102 MidtermQ1 CashRose Marie93% (15)

- Audit of Cash and Cash Equivalents: Problem No. 20Document6 pagesAudit of Cash and Cash Equivalents: Problem No. 20Robel MurilloNo ratings yet

- AEFAR 3 PRELIMS PrintDocument7 pagesAEFAR 3 PRELIMS Print버니 모지코No ratings yet

- Let Check AACC124 PDFDocument13 pagesLet Check AACC124 PDFFatima Medriza DuranNo ratings yet

- Mock Departmental Part 1Document7 pagesMock Departmental Part 1Mikee RizonNo ratings yet

- Ta-1004q1 Cash and Cash EquivalentsDocument3 pagesTa-1004q1 Cash and Cash Equivalentsleonardo alis100% (1)

- p2 Quiz Acc 103Document4 pagesp2 Quiz Acc 103Ariane Grace Hiteroza Margajay100% (1)

- Reviewer - Cash & Cash EquivalentsDocument5 pagesReviewer - Cash & Cash EquivalentsMaria Kathreena Andrea Adeva100% (1)

- Quiz 1Document11 pagesQuiz 1Sam VeraNo ratings yet

- Cash & Cash Equivalents Accounting GuideDocument5 pagesCash & Cash Equivalents Accounting Guidejane dillanNo ratings yet

- Simulates Midterm Exam. IntAcc1 PDFDocument11 pagesSimulates Midterm Exam. IntAcc1 PDFA NuelaNo ratings yet

- 112 Practice Material: Cash, Cash Equivalents, Bank Reconciliation Petty CashDocument7 pages112 Practice Material: Cash, Cash Equivalents, Bank Reconciliation Petty CashKairo ZeviusNo ratings yet

- Financial Accounting Exam ReviewDocument15 pagesFinancial Accounting Exam ReviewChjxksjsgskNo ratings yet

- Cash and Cash Equivalents ExamDocument7 pagesCash and Cash Equivalents ExamRudydanvinz BernardoNo ratings yet

- 19283198237Document11 pages19283198237xjammerNo ratings yet

- E-Handout On Audit of Cash and Cash EquivalentsDocument12 pagesE-Handout On Audit of Cash and Cash EquivalentsAsnifah AlinorNo ratings yet

- Ap-1402 CashDocument22 pagesAp-1402 Cashjulie anne mae mendozaNo ratings yet

- Theory of Accounts Cash and Cash EquivalentsDocument9 pagesTheory of Accounts Cash and Cash Equivalentsida_takahashi43% (14)

- F 51124304Document3 pagesF 51124304hanamay_07No ratings yet

- Chapter 10Document35 pagesChapter 10Joanna GarciaNo ratings yet

- TOA - 01-CASH AND CASH EQUIVALENTS W - SOLDocument5 pagesTOA - 01-CASH AND CASH EQUIVALENTS W - SOLPachi100% (1)

- Long Quiz 1 Acc 205Document6 pagesLong Quiz 1 Acc 205Philip LarozaNo ratings yet

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Rating: 5 out of 5 stars5/5 (1)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- Financial and Accounting Guide for Not-for-Profit OrganizationsFrom EverandFinancial and Accounting Guide for Not-for-Profit OrganizationsNo ratings yet

- Job DescriptionDocument21 pagesJob DescriptionRonnie PahilagaoNo ratings yet

- Mission StatementDocument1 pageMission StatementRonnie PahilagaoNo ratings yet

- Company Name and LogoDocument2 pagesCompany Name and LogoRonnie PahilagaoNo ratings yet

- Business MachinesDocument9 pagesBusiness MachinesRonnie PahilagaoNo ratings yet

- Application LetterDocument2 pagesApplication LetterRonnie Pahilagao100% (2)

- Application LetterDocument2 pagesApplication LetterRonnie PahilagaoNo ratings yet

- Code of ConductDocument1 pageCode of ConductRonnie PahilagaoNo ratings yet

- Accounting Systems Designed For Publiq Coffee and BeerDocument207 pagesAccounting Systems Designed For Publiq Coffee and BeerRonnie PahilagaoNo ratings yet

- Business Forms and DocumentsDocument36 pagesBusiness Forms and DocumentsRonnie PahilagaoNo ratings yet

- It 3 AssignmentDocument4 pagesIt 3 AssignmentRonnie PahilagaoNo ratings yet

- International Auditing OverviewDocument36 pagesInternational Auditing OverviewAnuradha AcharyaNo ratings yet

- International Auditing OverviewDocument36 pagesInternational Auditing OverviewAnuradha AcharyaNo ratings yet

- Hi HelloDocument1 pageHi HelloRonnie PahilagaoNo ratings yet

- Hi HelloDocument1 pageHi HelloRonnie PahilagaoNo ratings yet

- The Parts of A CheckDocument2 pagesThe Parts of A Checkjamaica dingleNo ratings yet

- Certified Dental AssistantDocument22 pagesCertified Dental AssistantRoxana Larisa CiobotaruNo ratings yet

- Notification Fema 14 (R)Document5 pagesNotification Fema 14 (R)Jagadeesan PurushothamanNo ratings yet

- Audit Cash Equivalents Receivables NotesDocument11 pagesAudit Cash Equivalents Receivables NotesEdemson NavalesNo ratings yet

- Petty Cash SolutionsDocument20 pagesPetty Cash SolutionsHassleBustNo ratings yet

- STOCK AUDIT PROCEDURES AND IRREGULARITIESDocument4 pagesSTOCK AUDIT PROCEDURES AND IRREGULARITIESCma Suman Kumar VermaNo ratings yet

- WORKS AUDIT MANUAL INSPECTION GUIDEDocument123 pagesWORKS AUDIT MANUAL INSPECTION GUIDEmuhammad yasirNo ratings yet

- Deseret First Credit Union Statement.Document6 pagesDeseret First Credit Union Statement.cathy clarkNo ratings yet

- En 05 10073Document8 pagesEn 05 10073OneNationNo ratings yet

- FMMA Vol 1 8th EditionDocument117 pagesFMMA Vol 1 8th EditionMurtaza HashimNo ratings yet

- Abridged Version of ProspectusDocument12 pagesAbridged Version of ProspectusAbbasi Hira100% (1)

- Direct Deposit FormDocument3 pagesDirect Deposit FormSreenivas RaoNo ratings yet

- Philippine Banking Laws SummaryDocument41 pagesPhilippine Banking Laws SummaryNeil GloriaNo ratings yet

- Eadvice-2019 06 23 00 19 27 PDFDocument2 pagesEadvice-2019 06 23 00 19 27 PDFsuwNo ratings yet

- PTR Form of North Delhi Municipal Corporation For 2014-15Document5 pagesPTR Form of North Delhi Municipal Corporation For 2014-15rasiya49No ratings yet

- Axis Gold ETF KIM Application FormDocument6 pagesAxis Gold ETF KIM Application Formrkdgr87880No ratings yet

- Internship ReportDocument60 pagesInternship Reportraahul7100% (3)

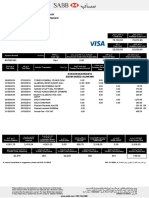

- SABB Platinum Visa Credit Card StatementDocument2 pagesSABB Platinum Visa Credit Card Statementsabah alsannaa100% (1)

- Technical-Vocational LivelihoodDocument16 pagesTechnical-Vocational LivelihoodAda S. RicañaNo ratings yet

- Two Column Cash BookDocument24 pagesTwo Column Cash BookDarshans dadNo ratings yet

- Sample General Ledger With Trial BalanceDocument10 pagesSample General Ledger With Trial BalanceIriz Beleno0% (1)

- Dispute form for unauthorized Google Ads chargeDocument2 pagesDispute form for unauthorized Google Ads chargeRaviteja DhammishettyNo ratings yet

- Ebilling SDKDocument414 pagesEbilling SDKWilfred MbithiNo ratings yet

- HDFC Competition Analysis-CharuDocument97 pagesHDFC Competition Analysis-Charudheeraj_kush100% (1)

- PC 16 - MCQ - Rahi - CPWA - Appendix - AnsDocument4 pagesPC 16 - MCQ - Rahi - CPWA - Appendix - AnsVirendra Ramteke100% (1)

- Chapter 3 Ethiopian Govt AcctingDocument19 pagesChapter 3 Ethiopian Govt AcctingwubeNo ratings yet

- Summary (Banking) VitalijaSDocument2 pagesSummary (Banking) VitalijaSv sNo ratings yet

- Albenson Enterprises Corp. v. CA (G.R. No. 88694 January 11, 1993)Document12 pagesAlbenson Enterprises Corp. v. CA (G.R. No. 88694 January 11, 1993)Hershey Delos Santos100% (1)

- Amir 12Document3 pagesAmir 12Dani KhanNo ratings yet

- How To Read Your RCN BillDocument1 pageHow To Read Your RCN BillMiguel ÁngelNo ratings yet