You might also like

- Excercises On Branch and Home Office Chapter TwoDocument3 pagesExcercises On Branch and Home Office Chapter Twoሔርሞን ይድነቃቸው50% (4)

- Accounting For Branch Operations Beams ch10 PDFDocument33 pagesAccounting For Branch Operations Beams ch10 PDFJeremiah Arief100% (1)

- TBChap 005Document157 pagesTBChap 005John Loserrtr80% (5)

- Advanced Financial Accounting Worksheet Chapter One SolutionsDocument3 pagesAdvanced Financial Accounting Worksheet Chapter One SolutionsJichang Hik100% (3)

- Green Company Is Considering Acquiring The Assets of Gold Company by Assuming Gold's Liabilities and byDocument5 pagesGreen Company Is Considering Acquiring The Assets of Gold Company by Assuming Gold's Liabilities and byሔርሞን ይድነቃቸው67% (3)

- Jawaban BE15 - AKMDocument3 pagesJawaban BE15 - AKMMazz BadruezNo ratings yet

- Abaynesh Abate Advanced Financial AccountingDocument7 pagesAbaynesh Abate Advanced Financial Accountingሔርሞን ይድነቃቸውNo ratings yet

- Ex Ch.15Document2 pagesEx Ch.15kenny 322016048No ratings yet

- Test Bank CH 3Document32 pagesTest Bank CH 3Sharmaine Rivera MiguelNo ratings yet

- Quiz 2 HolyeDocument47 pagesQuiz 2 Holyegoamank100% (5)

- Intercompany Profit Transactions - Inventories: Transactions Within The Affiliated GroupDocument60 pagesIntercompany Profit Transactions - Inventories: Transactions Within The Affiliated GroupPhil MO JoeNo ratings yet

- Chapter 16Document6 pagesChapter 16YasirNo ratings yet

- Natnael Wolde Advanced Financial AccountingDocument7 pagesNatnael Wolde Advanced Financial Accountingሔርሞን ይድነቃቸው100% (1)

- MGT Adv Serv 09.2019Document11 pagesMGT Adv Serv 09.2019Weddie Mae VillarizaNo ratings yet

- Consolidated income reviewDocument7 pagesConsolidated income reviewGinn100% (1)

- Private Not-for-Profit Entities: Accounting Principles and Reporting PracticesDocument44 pagesPrivate Not-for-Profit Entities: Accounting Principles and Reporting PracticesYuvia KeithleyreNo ratings yet

- Problems CH 14Document14 pagesProblems CH 14StephenMcDaniel50% (4)

- Exercise Advanced Accounting SolutionsDocument14 pagesExercise Advanced Accounting SolutionsMiko Victoria Vargas75% (4)

- Solution Manual For Advanced Accounting 11th Edition by Beams 3 PDF FreeDocument14 pagesSolution Manual For Advanced Accounting 11th Edition by Beams 3 PDF Freeluxion bot100% (1)

- Chapter 12Document42 pagesChapter 12Ivo_Nicht100% (4)

- ACCT 3110 CH 7 Homework E 4 8 13 19 20 27Document7 pagesACCT 3110 CH 7 Homework E 4 8 13 19 20 27John Job100% (1)

- MGMT AssignmentDocument79 pagesMGMT AssignmentLuleseged Gebre100% (1)

- On September IDocument37 pagesOn September IYuki Takeno100% (2)

- The Following Questions Might Be Addressed When An Auditor Is Completing An Internal Control QuestionDocument1 pageThe Following Questions Might Be Addressed When An Auditor Is Completing An Internal Control QuestionSomething ChicNo ratings yet

- Chap005-Consolidation of Less-Than-Wholly Owned SubsidiariesDocument71 pagesChap005-Consolidation of Less-Than-Wholly Owned Subsidiaries_casals100% (3)

- Accounting For BranchesDocument53 pagesAccounting For Branchesalemayehu100% (2)

- Advance Financial Accounting (Assignment)Document3 pagesAdvance Financial Accounting (Assignment)asegidNo ratings yet

- DocxDocument21 pagesDocxIzzy BNo ratings yet

- 2010-09-27 104244 AdvancedDocument11 pages2010-09-27 104244 Advancedhetalcar100% (1)

- Chapter 3: Business Combination: Based On IFRS 3Document38 pagesChapter 3: Business Combination: Based On IFRS 3ሔርሞን ይድነቃቸውNo ratings yet

- Chapter 16 Chat Exercises Part IIDocument17 pagesChapter 16 Chat Exercises Part IIAnatasyaOktavianiHandriatiTataNo ratings yet

- Acct 108 Accounting For Business Combinations Quiz 4 - Intercompany Sales of AssetsDocument2 pagesAcct 108 Accounting For Business Combinations Quiz 4 - Intercompany Sales of AssetsGround ZeroNo ratings yet

- IFRS 15 - Exercises (Kieso)Document10 pagesIFRS 15 - Exercises (Kieso)Iris Claire GamadNo ratings yet

- Chap 5Document43 pagesChap 5Akm Engida67% (3)

- Brief Exercises CHAPTER 7Document3 pagesBrief Exercises CHAPTER 7Trang LeNo ratings yet

- Beams AdvAcc11 Chapter17Document22 pagesBeams AdvAcc11 Chapter17husnaini dwi wanriNo ratings yet

- CH 6Document6 pagesCH 6Natsu DragneelNo ratings yet

- Afar 2 ExamDocument3 pagesAfar 2 ExamNurul-Fawzia Balindong0% (4)

- Chapter 04 Modern Advanced AccountingDocument31 pagesChapter 04 Modern Advanced AccountingPhoebe Lim81% (21)

- AccntngDocument3 pagesAccntngChristine Dela Rosa CarolinoNo ratings yet

- Review Problems AnswersDocument4 pagesReview Problems AnswersFranchette Yvonne JulianNo ratings yet

- Tugas Akuntansi Keuangan LanjutanDocument8 pagesTugas Akuntansi Keuangan LanjutanMin DaeguNo ratings yet

- Advance Accounting Chapter 15Document3 pagesAdvance Accounting Chapter 15brew167525% (4)

- MC 789Document59 pagesMC 789Minh Nguyễn83% (6)

- Advanced Accounting Testbank QuestionsDocument37 pagesAdvanced Accounting Testbank Questionsxxshoopxx100% (1)

- The Partnership of Frick, Wilson, and Clarke Has Elected To Cease All Operations and Liquidate Its Business PropertyDocument7 pagesThe Partnership of Frick, Wilson, and Clarke Has Elected To Cease All Operations and Liquidate Its Business PropertyKailash KumarNo ratings yet

- ACG4803 - Chapter 5Document108 pagesACG4803 - Chapter 5Minh Nguyễn100% (2)

- FIFO, LIFO, and Average Cost MethodsDocument14 pagesFIFO, LIFO, and Average Cost MethodsMenaz Sadaka100% (1)

- Calculating unrealized intercompany inventory profit adjustmentDocument22 pagesCalculating unrealized intercompany inventory profit adjustmentxxxxxxxxx100% (3)

- DocxDocument5 pagesDocxSylvia Al-a'maNo ratings yet

- As of January 1 2015 Information Related To The DefinedDocument1 pageAs of January 1 2015 Information Related To The DefinedMuhammad ShahidNo ratings yet

- Calculation of net income from shareholders' equity changeDocument4 pagesCalculation of net income from shareholders' equity changePrerna AroraNo ratings yet

- Ex Ch.17Document3 pagesEx Ch.17kenny 322016048No ratings yet

- Mojakoe Ak2 Uts 2018 PDFDocument17 pagesMojakoe Ak2 Uts 2018 PDFRayhandi AlmerifkiNo ratings yet

- Solutions To Exercises Exercise 18-1-15Document50 pagesSolutions To Exercises Exercise 18-1-15Aiziel OrenseNo ratings yet

- Chapter 4Document28 pagesChapter 4Shibly SadikNo ratings yet

- Sequoia Ann 14Document36 pagesSequoia Ann 14CanadianValueNo ratings yet

- Estimates 2019/2020Document624 pagesEstimates 2019/2020Jason victorNo ratings yet

- 03 Course Notes On Statement of Cash Flows-2 PDFDocument4 pages03 Course Notes On Statement of Cash Flows-2 PDFMaxin TanNo ratings yet

- ManAcc 1 - Finals Quiz 1 QuestionsDocument5 pagesManAcc 1 - Finals Quiz 1 QuestionsZihr EllerycNo ratings yet

- Idirect Install Ti On BasicDocument1 pageIdirect Install Ti On BasicEsko KonopiskiNo ratings yet

- Ejercicios de Presente Simple y Presente Continuo PDFDocument2 pagesEjercicios de Presente Simple y Presente Continuo PDFAlfonso DíezNo ratings yet

- Electrical Safety Devices at Home: Science 8Document5 pagesElectrical Safety Devices at Home: Science 8John Mark PrestozaNo ratings yet

- PE Goals, Fitness Benefits & Philippine Folk DancesDocument64 pagesPE Goals, Fitness Benefits & Philippine Folk DancesMichael Dela Cruz RiveraNo ratings yet

- Self Assessment For Observed LessonDocument2 pagesSelf Assessment For Observed Lessonapi-241168263No ratings yet

- TH 400 Automatic Transmission: General Towing The VehicleDocument42 pagesTH 400 Automatic Transmission: General Towing The VehicleFernando Bas100% (1)

- Girma TelilaDocument107 pagesGirma TelilaTedla BekeleNo ratings yet

- How to knit top down sleeves flat (less than 40 charsDocument3 pagesHow to knit top down sleeves flat (less than 40 charsRadu AnghelNo ratings yet

- Tony PavesDocument1 pageTony PavesTanvir Hasan RakinNo ratings yet

- Hospital Waste Management ArticleDocument5 pagesHospital Waste Management ArticleFarrukh AzizNo ratings yet

- Report Accompanying With EstimateDocument2 pagesReport Accompanying With EstimateparameswarikumarNo ratings yet

- Plant Inspector CV.Document7 pagesPlant Inspector CV.Khalilahmad KhatriNo ratings yet

- LL.M.203 Unit 5. Summary of RTE Act.2009Document7 pagesLL.M.203 Unit 5. Summary of RTE Act.2009mukendermeena10sNo ratings yet

- Information and Knowledge Management in LibrariesDocument3 pagesInformation and Knowledge Management in LibrariesTahur AhmedNo ratings yet

- Formatted - Sample Text g6Document1 pageFormatted - Sample Text g6Annjen MuliNo ratings yet

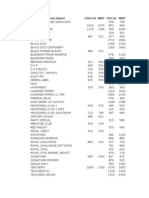

- Price ListDocument28 pagesPrice Listhomerahul9070No ratings yet

- Newsletter 20 - January 2008Document12 pagesNewsletter 20 - January 2008Alexander Mendoza100% (1)

- Mid Term Date Sheet - pq0NsApDocument2 pagesMid Term Date Sheet - pq0NsApSahil HansNo ratings yet

- Soal Bahasa Inggris Kelas 7 Chapter 1Document3 pagesSoal Bahasa Inggris Kelas 7 Chapter 1AcizziaChocca57% (7)

- Brief Industrial Profile of Haveri District, Karnataka StateDocument13 pagesBrief Industrial Profile of Haveri District, Karnataka StateShyam J VyasNo ratings yet

- Commonly Used AbbreviationsDocument5 pagesCommonly Used AbbreviationsUzziel Galinea TolosaNo ratings yet

- Makkah Train Network ProjectDocument3 pagesMakkah Train Network ProjectSTP DesignNo ratings yet

- MilestoneDocument36 pagesMilestoneRiza ZaharaNo ratings yet

- Advanced Financial Reporting EthicsDocument4 pagesAdvanced Financial Reporting Ethicswaresh36No ratings yet

- IPS Academy compares HUL and ITC LtdDocument14 pagesIPS Academy compares HUL and ITC LtdFaizanNo ratings yet

- SUD-Oisterwijk Omschrijvingen - enDocument3 pagesSUD-Oisterwijk Omschrijvingen - enJose CarbajalNo ratings yet

- S.M. Stirling & Jerry Pournelle - Falkenberg 1 - Falkenberg's Legion EDocument156 pagesS.M. Stirling & Jerry Pournelle - Falkenberg 1 - Falkenberg's Legion ENaomi TressNo ratings yet

- Dale Spender - Living by The Pen - Early British Women Writers (1992, Teachers College Press) - Libgen - LiDocument276 pagesDale Spender - Living by The Pen - Early British Women Writers (1992, Teachers College Press) - Libgen - LiGime VilchezNo ratings yet

- Bayan Ul QuranDocument18 pagesBayan Ul QuransahibafNo ratings yet

- Ilovepdf MergedDocument33 pagesIlovepdf MergedRajesh Bhat - Estimation Dept. KBP CivilNo ratings yet