You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Exam in Taxation Exam in Taxation: Business Tax (Naga College Foundation) Business Tax (Naga College Foundation)Document29 pagesExam in Taxation Exam in Taxation: Business Tax (Naga College Foundation) Business Tax (Naga College Foundation)jhean dabatosNo ratings yet

- ch10 PDFDocument9 pagesch10 PDFcris lu salemNo ratings yet

- Consolidated Statement of Profit and LossDocument9 pagesConsolidated Statement of Profit and LossHrushikesh DahaleNo ratings yet

- Plant and Intangible Assets: Mcgraw-Hill/IrwinDocument60 pagesPlant and Intangible Assets: Mcgraw-Hill/Irwinazee inmixNo ratings yet

- Consolidated Financial StatementDocument24 pagesConsolidated Financial StatementNguyen Dac Thich100% (1)

- Finance in SAPDocument49 pagesFinance in SAPekta100% (1)

- 15 Accounting ProcedureDocument15 pages15 Accounting ProcedurenorlieNo ratings yet

- Peran Audit Atas Kas Dan Setara Kas Pada PT. Murni Gas Raya SamarindaDocument5 pagesPeran Audit Atas Kas Dan Setara Kas Pada PT. Murni Gas Raya SamarindaAn WismoNo ratings yet

- Accounting 4 Module 1 3Document3 pagesAccounting 4 Module 1 3Micaela EncinasNo ratings yet

- Working Capital ManagementDocument45 pagesWorking Capital ManagementRaghav100% (1)

- Estimation of Project Cash Flows: Centre For Financial Management, BangaloreDocument14 pagesEstimation of Project Cash Flows: Centre For Financial Management, BangaloreNic KnightNo ratings yet

- FMI - Chapter 21 Thrift OperationsDocument34 pagesFMI - Chapter 21 Thrift OperationsChew96No ratings yet

- How Corporations Issue Securities: Eighth EditionDocument15 pagesHow Corporations Issue Securities: Eighth EditionFelix Owusu DarteyNo ratings yet

- Funding The Business TACN 2 HVTCDocument10 pagesFunding The Business TACN 2 HVTCNguyễn Lương Minh ChâuNo ratings yet

- Test PracticeDocument26 pagesTest PracticeStephanie NaamaniNo ratings yet

- Asian Paints Equity ValuationDocument24 pagesAsian Paints Equity ValuationYash DangraNo ratings yet

- Report On Financial Statement of InfosysDocument22 pagesReport On Financial Statement of InfosysSoham Khanna100% (2)

- XYZ Bank Balance Sheet AnalysisDocument4 pagesXYZ Bank Balance Sheet AnalysisMarcusNo ratings yet

- LBO Sensitivity Tables BeforeDocument37 pagesLBO Sensitivity Tables BeforeMamadouB100% (2)

- Calculating days sales outstanding multiple choice itemDocument30 pagesCalculating days sales outstanding multiple choice itemRohit ChellaniNo ratings yet

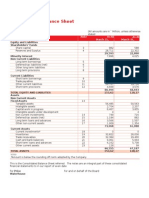

- Balance Sheet Net PP&EDocument13 pagesBalance Sheet Net PP&Esalimanderz813No ratings yet

- Management Accounting Final ExamDocument4 pagesManagement Accounting Final Examacctg2012No ratings yet

- Consolidated Balance Sheet: Annual Report 2013 - 2014Document2 pagesConsolidated Balance Sheet: Annual Report 2013 - 2014mgajenNo ratings yet

- Dust Bee Gone Cleaning Service Corporation 1 1 2Document20 pagesDust Bee Gone Cleaning Service Corporation 1 1 2pangantihonjohnearlNo ratings yet

- Analysis of Financial Statements RatiosDocument9 pagesAnalysis of Financial Statements RatiosViren DeshpandeNo ratings yet

- Long Term Debt Paying Ability Solvency RatiosDocument9 pagesLong Term Debt Paying Ability Solvency RatiosZarish AzharNo ratings yet

- Oct-Nov - 2012 Paper 1Document8 pagesOct-Nov - 2012 Paper 1Israel AyemoNo ratings yet

- Maini - Blueprint - Fi - 100 - Main Document - Ver - 3.0 PDFDocument69 pagesMaini - Blueprint - Fi - 100 - Main Document - Ver - 3.0 PDFBhaskarChakraborty0% (2)

- JPM Trip Com TCOM US 2023-07-30Document16 pagesJPM Trip Com TCOM US 2023-07-30goondu_93No ratings yet

- Report On The Industrial Visit Linc LimitedDocument28 pagesReport On The Industrial Visit Linc LimitedRajdeep Paul100% (1)