You might also like

- Eliminating Risks of De-risking for Caribbean's InclusionDocument24 pagesEliminating Risks of De-risking for Caribbean's InclusionJ'Moul A. FrancisNo ratings yet

- De-Risking and Its Impact CCMF Working PaperDocument18 pagesDe-Risking and Its Impact CCMF Working PaperJules BGNo ratings yet

- Credit Risk Management In and Out of the Financial Crisis: New Approaches to Value at Risk and Other ParadigmsFrom EverandCredit Risk Management In and Out of the Financial Crisis: New Approaches to Value at Risk and Other ParadigmsRating: 1 out of 5 stars1/5 (1)

- 33 Compliance and Control PDFDocument14 pages33 Compliance and Control PDFEkta Saraswat VigNo ratings yet

- Portfolio Risk AnalysisDocument30 pagesPortfolio Risk Analysismentor_muhaxheriNo ratings yet

- Credit Risk Chapter SummaryDocument106 pagesCredit Risk Chapter SummaryFarhia NaveedNo ratings yet

- Deleveraging Investing Optimizing Capital StructurDocument42 pagesDeleveraging Investing Optimizing Capital StructurDanaero SethNo ratings yet

- Basel NormsDocument66 pagesBasel NormsShanmathiNo ratings yet

- bcbs292 PDFDocument61 pagesbcbs292 PDFguindaniNo ratings yet

- Credit Management HandbookDocument48 pagesCredit Management HandbookNauman Rashid67% (6)

- Capital Adequacy Mms 2011Document121 pagesCapital Adequacy Mms 2011Aishwary KhandelwalNo ratings yet

- Credit RatingDocument63 pagesCredit Ratingnikhu_shuklaNo ratings yet

- ALCO Structure Responsibilities and Risk ManagementDocument9 pagesALCO Structure Responsibilities and Risk ManagementQamber AliNo ratings yet

- Brismo Analytics Loan Vintage AnalysisDocument2 pagesBrismo Analytics Loan Vintage AnalysisVanderghastNo ratings yet

- Fitch Rating MethodologyDocument16 pagesFitch Rating Methodologyrash2014No ratings yet

- BFM - CH - 9 - Module BDocument14 pagesBFM - CH - 9 - Module BAksNo ratings yet

- Risk PDFDocument44 pagesRisk PDFTathi GuerreroNo ratings yet

- Alternatives in Todays Capital MarketsDocument16 pagesAlternatives in Todays Capital MarketsjoanNo ratings yet

- Guiding PrinciplesDocument39 pagesGuiding PrinciplestiwariajaykNo ratings yet

- Asset Liability Management Under Risk FrameworkDocument9 pagesAsset Liability Management Under Risk FrameworklinnnehNo ratings yet

- Guidelines on Risk Appetite PracticesDocument34 pagesGuidelines on Risk Appetite PracticesPRIME ConsultoresNo ratings yet

- Retail Banking in India (FULL)Document53 pagesRetail Banking in India (FULL)Vinidra WattalNo ratings yet

- Modelin NG Banks' ' Probabil Lity of de EfaultDocument23 pagesModelin NG Banks' ' Probabil Lity of de Efaulthoangminhson0602No ratings yet

- Script - Market Risk - Part 1 PDFDocument154 pagesScript - Market Risk - Part 1 PDFJames AndersonNo ratings yet

- Analysis On Islamic Bank On Rate of Return RiskDocument25 pagesAnalysis On Islamic Bank On Rate of Return RiskNurhidayatul AqmaNo ratings yet

- ALM Project ReportDocument18 pagesALM Project ReportAISHWARYA CHAUHANNo ratings yet

- Risk Management Techniques and ToolsDocument34 pagesRisk Management Techniques and ToolsRiantyasYunelzaNo ratings yet

- PWC Eu Bank Recovery and Resolution Directive Triumph or TragedyDocument8 pagesPWC Eu Bank Recovery and Resolution Directive Triumph or TragedykunalwarwickNo ratings yet

- Procedure of Credit RatingDocument57 pagesProcedure of Credit RatingMilon SultanNo ratings yet

- III.B.6 Credit Risk Capital CalculationDocument28 pagesIII.B.6 Credit Risk Capital CalculationvladimirpopovicNo ratings yet

- Risk Model Presentation For Risk and DDDocument15 pagesRisk Model Presentation For Risk and DDjohn9727100% (1)

- Regulatory Directives on Loan ClassificationDocument37 pagesRegulatory Directives on Loan ClassificationNur AlahiNo ratings yet

- Credit Risk Management in Icici BankDocument2 pagesCredit Risk Management in Icici Banknatashafdo50% (2)

- CBM Basel III - Group 7Document16 pagesCBM Basel III - Group 7durgananNo ratings yet

- PWC Client IFRS Update 2016 PDFDocument143 pagesPWC Client IFRS Update 2016 PDFteddy matendawafaNo ratings yet

- Liquidity Presentation 20160518Document22 pagesLiquidity Presentation 20160518cpasl123No ratings yet

- Real Property Evaluations GuideDocument6 pagesReal Property Evaluations GuideIchi MendozaNo ratings yet

- Equity Valuation: B, K & M Chapter 13Document28 pagesEquity Valuation: B, K & M Chapter 13Fatima MosawiNo ratings yet

- Credit ManagementDocument46 pagesCredit ManagementMohammed ShaffanNo ratings yet

- Equity Risk Management PolicyDocument4 pagesEquity Risk Management PolicymkjailaniNo ratings yet

- Senate Hearing, 110TH Congress - Carbon Sequestration TechnologiesDocument95 pagesSenate Hearing, 110TH Congress - Carbon Sequestration TechnologiesScribd Government DocsNo ratings yet

- Prime BrokeringDocument3 pagesPrime BrokeringwesmendenNo ratings yet

- PWC Global Fintech Report 2019Document29 pagesPWC Global Fintech Report 2019Hoàng Châu Trần ĐoànNo ratings yet

- Case Study Operational RiskDocument27 pagesCase Study Operational RiskDikankatla SelahleNo ratings yet

- Bank Risk Management Is Used Mostly in The FinancialDocument9 pagesBank Risk Management Is Used Mostly in The FinancialYash PratapNo ratings yet

- Comparison of Modeling Methods For Loss Given DefaultDocument14 pagesComparison of Modeling Methods For Loss Given DefaultAnnNo ratings yet

- CREDIT RISK MODELLING CURRENT PRACTICES AND APPLICATIONSDocument65 pagesCREDIT RISK MODELLING CURRENT PRACTICES AND APPLICATIONSPriya RanjanNo ratings yet

- Credit Risk S1Document33 pagesCredit Risk S1tanmaymehta24No ratings yet

- Determinants of Credit RatingDocument23 pagesDeterminants of Credit RatingFerlyan Huang 正莲No ratings yet

- Act Cash Management: Managing Cash in A Digital WorldDocument20 pagesAct Cash Management: Managing Cash in A Digital WorldFitiavana Joel AndriantsehenoNo ratings yet

- ICAAP Sample Credit Report TocDocument2 pagesICAAP Sample Credit Report TocJawwad FaridNo ratings yet

- The Bankers Guide To Basel IIDocument59 pagesThe Bankers Guide To Basel IIdominic.soon8900100% (2)

- IFRS 9 Part III Impairment CPD November 2015Document41 pagesIFRS 9 Part III Impairment CPD November 2015Nicolaus CopernicusNo ratings yet

- Moody's Corporate Default and Recovery Rates, 1920-2010. Moody's. February 2011Document66 pagesMoody's Corporate Default and Recovery Rates, 1920-2010. Moody's. February 2011VizziniNo ratings yet

- Evolution of Basel Norms and Their Contribution To The Subprime CrisisDocument7 pagesEvolution of Basel Norms and Their Contribution To The Subprime Crisisstuti dalmiaNo ratings yet

- Standard Operating Procedure (SOP) For eNPSDocument22 pagesStandard Operating Procedure (SOP) For eNPSahan verma100% (1)

- Foundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsFrom EverandFoundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsNo ratings yet

- Quantitative Credit Portfolio Management: Practical Innovations for Measuring and Controlling Liquidity, Spread, and Issuer Concentration RiskFrom EverandQuantitative Credit Portfolio Management: Practical Innovations for Measuring and Controlling Liquidity, Spread, and Issuer Concentration RiskRating: 3.5 out of 5 stars3.5/5 (1)

- Spanish Football Federation Soccer Camps in Madrid, SpainDocument7 pagesSpanish Football Federation Soccer Camps in Madrid, SpainKerine HeronNo ratings yet

- FCB Escola Coaches Seminar-Day 1Document10 pagesFCB Escola Coaches Seminar-Day 1cbales9988% (8)

- Oliver Wyman Airline Economic Analysis 2015 2016Document68 pagesOliver Wyman Airline Economic Analysis 2015 2016DharmeshNo ratings yet

- Wps424 Small Open Economy DSGE Model - BrazilDocument40 pagesWps424 Small Open Economy DSGE Model - BrazilKerine HeronNo ratings yet

- Land Chapter 2Document4 pagesLand Chapter 2Kerine HeronNo ratings yet

- Development Economic PolicyDocument1 pageDevelopment Economic PolicyKerine HeronNo ratings yet

- PASS Academy 24 Training SessionsDocument379 pagesPASS Academy 24 Training SessionsKerine Heron100% (1)

- ASPL614 Airline Business PDFDocument41 pagesASPL614 Airline Business PDFmahanumNo ratings yet

- Small Open Economy DSGE Model For PakistanDocument48 pagesSmall Open Economy DSGE Model For PakistanKerine HeronNo ratings yet

- UNDP-Caribbean Human Development Report 2016 PDFDocument248 pagesUNDP-Caribbean Human Development Report 2016 PDFKerine HeronNo ratings yet

- Getting Married in Virginia - Virginia Is For LoversDocument3 pagesGetting Married in Virginia - Virginia Is For LoversKerine HeronNo ratings yet

- Getting Married in Virginia - Virginia Is For LoversDocument3 pagesGetting Married in Virginia - Virginia Is For LoversKerine HeronNo ratings yet

- Ireland Economic Adjustment ProgrammeDocument90 pagesIreland Economic Adjustment ProgrammeKerine HeronNo ratings yet

- Peter Schreiner SystemDocument11 pagesPeter Schreiner SystemKerine HeronNo ratings yet

- SKNTTA Summer Table Tennis Camp 2015Document1 pageSKNTTA Summer Table Tennis Camp 2015Kerine HeronNo ratings yet

- Match Analysis Manchester City Vs Bayern Munich - BayernDocument5 pagesMatch Analysis Manchester City Vs Bayern Munich - BayernKerine HeronNo ratings yet

- League Managers AssociationDocument2 pagesLeague Managers AssociationKerine HeronNo ratings yet

- SKB Salary Scale Budget 2013 Vols 1-2Document23 pagesSKB Salary Scale Budget 2013 Vols 1-2Kerine HeronNo ratings yet

- Youth-Soccer Evaluations Overview and InstructionsDocument8 pagesYouth-Soccer Evaluations Overview and InstructionsKerine HeronNo ratings yet

- ChelseaFC SoccerSchoolDocument2 pagesChelseaFC SoccerSchoolKerine HeronNo ratings yet

- Soccer - Football Management & Scouting CourseDocument5 pagesSoccer - Football Management & Scouting CourseKerine HeronNo ratings yet

- Jeff Bookman Bio Mar2011Document1 pageJeff Bookman Bio Mar2011Kerine HeronNo ratings yet

- UWI Business LawDocument10 pagesUWI Business LawKerine HeronNo ratings yet

- English Premiership - Man City V ArsenalDocument9 pagesEnglish Premiership - Man City V ArsenalKerine HeronNo ratings yet

- When Is Debt Sustainable 2006Document35 pagesWhen Is Debt Sustainable 2006Kerine HeronNo ratings yet

- Analysis of the Trends Shaping Modern Elite FootballDocument40 pagesAnalysis of the Trends Shaping Modern Elite FootballKerine HeronNo ratings yet

- Scouting Report - Man CityDocument25 pagesScouting Report - Man CityKerine HeronNo ratings yet

- Acf Fiorentina Coaching CourseDocument158 pagesAcf Fiorentina Coaching CourseKerine HeronNo ratings yet

- Fsi 2009Document48 pagesFsi 2009Kerine HeronNo ratings yet

- KaphDocument7 pagesKaphFrater MagusNo ratings yet

- Waiver: FEU/A-NSTP-QSF.03 Rev. No.: 00 Effectivity Date: Aug. 10, 2017Document1 pageWaiver: FEU/A-NSTP-QSF.03 Rev. No.: 00 Effectivity Date: Aug. 10, 2017terenceNo ratings yet

- Once in his Orient: Le Corbusier and the intoxication of colourDocument4 pagesOnce in his Orient: Le Corbusier and the intoxication of coloursurajNo ratings yet

- Blood Culture & Sensitivity (2011734)Document11 pagesBlood Culture & Sensitivity (2011734)Najib AimanNo ratings yet

- Climbing KnotsDocument40 pagesClimbing KnotsIvan Vitez100% (11)

- Ck-Nac FsDocument2 pagesCk-Nac Fsadamalay wardiwiraNo ratings yet

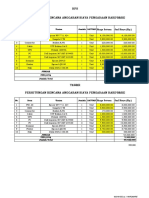

- HPS Perhitungan Rencana Anggaran Biaya Pengadaan Hardware: No. Item Uraian Jumlah SATUANDocument2 pagesHPS Perhitungan Rencana Anggaran Biaya Pengadaan Hardware: No. Item Uraian Jumlah SATUANYanto AstriNo ratings yet

- Shilajit The Panacea For CancerDocument48 pagesShilajit The Panacea For Cancerliving63100% (1)

- Farm Policy Options ChecklistDocument2 pagesFarm Policy Options ChecklistJoEllyn AndersonNo ratings yet

- Week 5 WHLP Nov. 2 6 2020 DISSDocument5 pagesWeek 5 WHLP Nov. 2 6 2020 DISSDaniel BandibasNo ratings yet

- MT 1 Combined Top 200Document3 pagesMT 1 Combined Top 200ShohanNo ratings yet

- AC & Crew Lists 881st 5-18-11Document43 pagesAC & Crew Lists 881st 5-18-11ywbh100% (2)

- Final Literature CircleDocument10 pagesFinal Literature Circleapi-280793165No ratings yet

- Is The Question Too Broad or Too Narrow?Document3 pagesIs The Question Too Broad or Too Narrow?teo100% (1)

- Temperature Rise HV MotorDocument11 pagesTemperature Rise HV Motorashwani2101No ratings yet

- Court Reviews Liability of Staffing Agency for Damages Caused by Employee StrikeDocument5 pagesCourt Reviews Liability of Staffing Agency for Damages Caused by Employee StrikeDenzhu MarcuNo ratings yet

- El Rol Del Fonoaudiólogo Como Agente de Cambio Social (Segundo Borrador)Document11 pagesEl Rol Del Fonoaudiólogo Como Agente de Cambio Social (Segundo Borrador)Jorge Nicolás Silva Flores100% (1)

- Class 9 Maths Olympiad Achievers Previous Years Papers With SolutionsDocument7 pagesClass 9 Maths Olympiad Achievers Previous Years Papers With Solutionskj100% (2)

- Absolute Advantage and Comparative AdvantageDocument11 pagesAbsolute Advantage and Comparative AdvantageLouie ManaoNo ratings yet

- Successfull Weight Loss: Beginner'S Guide ToDocument12 pagesSuccessfull Weight Loss: Beginner'S Guide ToDenise V. FongNo ratings yet

- Accounting What The Numbers Mean 11th Edition Marshall Solutions Manual 1Document36 pagesAccounting What The Numbers Mean 11th Edition Marshall Solutions Manual 1amandawilkinsijckmdtxez100% (23)

- E2415 PDFDocument4 pagesE2415 PDFdannychacon27No ratings yet

- International BankingDocument3 pagesInternational BankingSharina Mhyca SamonteNo ratings yet

- APP Eciation: Joven Deloma Btte - Fms B1 Sir. Decederio GaganteDocument5 pagesAPP Eciation: Joven Deloma Btte - Fms B1 Sir. Decederio GaganteJanjan ToscanoNo ratings yet

- DepEd K to 12 Awards PolicyDocument29 pagesDepEd K to 12 Awards PolicyAstraea Knight100% (1)

- SEIPIDocument20 pagesSEIPIdexterbautistadecember161985No ratings yet

- Eco Orphanage: Model of Sustainability: 15 536 Words (Not Including Bibliography)Document78 pagesEco Orphanage: Model of Sustainability: 15 536 Words (Not Including Bibliography)Princess ManiquizNo ratings yet

- BAFINAR - Midterm Draft (R) PDFDocument11 pagesBAFINAR - Midterm Draft (R) PDFHazel Iris Caguingin100% (1)

- Christian Mission and Conversion. Glimpses About Conversion, Constitution, Right To ReligionDocument8 pagesChristian Mission and Conversion. Glimpses About Conversion, Constitution, Right To ReligionSudheer Siripurapu100% (1)